It’s enough to make you close up shop and seek out a new career if you’re a portfolio or hedge fund manager. I say that tongue and cheek of course, but next week will prove to be quite interesting if you have been reading the headlines and/or listening to what the major media outlets have been cultivating If we take these events mentioned in order, the greatest consideration would likely produce a good deal of volatility in the markets next week. Leading up to the aforementioned market events, volatility had already been rising and before peaking out at roughly 16.25 recently.

What had been sparking higher levels of volatility/fear, as represented by the VIX, had been the unusual dive in the 10yr. U.S. Treasury yield. This may have been the markets way of addressing the mentioned events in advance. Despite the FOMC’s decision to raise rates, the 10yr has done little more than find lower yields.

Such an outcome hadn’t been expected by many economists, as the normal trend of long-dated treasury yields during a period of rising Prime rates has been to rise in accordance with the Prime rate. The chart above recognizes the almost absolute correlation between the 10yr Treasury yield and the VIX over a 2-week period for which yields fell from 2.37%-2.28% and as the VIX rose from 13-16. The correlation finally detached last week as the VIX dropped a bit, even as rates continued their path lower with the 10yr yield dipping below 2.20 percent.

Golden Capital Portfolio invests in VIX-leveraged ETF/ETNs and as the Chief Investment Officer and Market Strategist, I’m always on the hunt for VIX correlations; I almost have to be as these instruments bear little efficacy with regards to technical analysis. Inverse VIX-leveraged ETPs such as ProShares Ultra VIX Short-Term Futures ETF (UVXY), VelocityShares Daily 2x VIX Short-Term ETN (TVIX), iPath S&P 500 VIX Short-Term Futures ETN (VXX) and the like have an intrinsic or designed decay. The level of the ETP is based on the value of the VIX short-term futures contracts (“VIX futures contracts”) that comprise the ETP. While there is a relationship between the performance of the ETP and future levels of the VIX, the performance is not directly linked to the performance of the VIX, to the realized volatility of the S&P 500 or to the options that underlie the calculation of the VIX. When trading or investing in these instruments, it is important to understand this concept before doing so. Keeping in mind that these instruments have been active in the marketplace for less than a decade, and are extremely unique in their construct, much of their trading patterns and usage by investors/traders is still developing an understanding for practical analysis and usage. In other words, what we have come to understand thus far, may find a new or elevated understanding in the future.

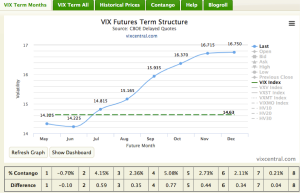

Moreover, even some of the more commonly used terminology for understanding the variables that affect the likes of these instruments can be called into question for usage. Two such terms that are widely used and recently exhibited with regards to VIX-Leveraged instruments is contango and backwardation. Look, I don’t really desire to get into the whole “backwardation” definition discussion here, so let’s just say I’ll go along with the text book definition offered by Investopedia… even as I find it illogical and lacking a correlation to the root word “backward”. “Backwardation occurs when the futures price of a commodity is lower than its market price today. Backwardation does not happen very frequently, and when it does, it usually doesn’t last long.”

That’s the definition of backwardation as offered by Investopedia, Webster’s Dictionary and even coined in the ProShares S-1 of these instruments. Within that same regard, backwardation is the opposite of contango, again, as offered by Investopedia.

“When the market for these contracts is such that the prices are higher in the nearer months than in the more distant months, the sale during the course of the “rolling process” of the more nearby futures contract would take place at a price that is higher than the price of the more distant futures contract. This pattern of higher futures prices for shorter expiration futures contracts is referred to as “backwardation.”

If you are new to these VIX-leveraged instruments and reading the above reference points regarding contango and backwardation for the first time, you probably shouldn’t be investing or trading these instruments just yet. For the sake of simplicity, however, contango is a key variable that acts like an anchor around the neck of any of these VIX-leveraged instruments of which UVXY is my instrument of choice. Contango doesn’t force UVXY or its peers to fall in price, but rather it suppresses the upward movement in price, even as buying pressure increases on VIX future contracts. It’s one of the reasons those who choose to utilize these instruments as so-called “hedges” against their long positions, the hedge is found not to perform as expected.

As recognized in the chart above, contango is understood in both positive and negative terms. Negative contango is referred to as a state of “backwardation”. The term used makes little sense when carefully considered, but I digress. What may be more important for the average investor/trader to understand about backwardation is that the ETPs under this circumstance has considerably less drag on the share price when in a state of backwardation.

I won’t suggest that negative contango allows for the erroneous and illogical use of the term “backwardation”. Or did I do just that very thing; suggest it in total. From a physics and physiological stance, take a look at your feet for a moment. What direction are they facing? Are they designed to face this way and if so does that design dictate a functional term understood to be “moving forward”. Essentially, our bodies were designed to move forward. Evolved, maybe some of you are more comfortable with that notion, evolved to move forward. Now take that principle or example I just offered and apply it to contango or the understood negative contango/backwardation. What’s the intrinsic design of contango? Correct there isn’t one. Contango or backwardation is actually a variable affected by a transmission mechanism, the interest in VIX Futures that ultimately converge on Spot VIX when expiration for these contracts comes to be. There is no real design and it is left to chance how contango will be affected by the transmission process, more commonly known as the “rolling process”. That’s a lot to take in I’m sure and especially for newcomers to the terminology. Remember though that these terms haven’t come into mass usage since the inception of VIX-leveraged trading instruments came into focus and actionable trading. But let’s get back to the term backwardation and why it makes little sense to refer to it using this term.

When we walk backward it is with the understanding that we weren’t designed to do so and I think we can all agree there is an intended design with regards to the way/direction we walk. We are working against the intended design of our human anatomy by walking backward. That’s what the underlying VIX-leveraged ETF/ETNs do when they go backward in share price; they work against the design and due to what I call inverted contango. Inverted contango is negative contango if I were to utilize a more correlated reference to the numerical system which proposes negative and positive integers and not directional terminology associated with the human body’s approximation or positioning to an object. I guess what I’m trying to say is where there is design, as there is with our feet, there is backwardation. Where there is an absence of design there is inversion. And where you have the numerical system you have negative and positive integers at least.

Words become redefined and refined all the time. Even Webster’s Dictionary is forced to redefine words almost every year for the betterment of terminology and definition in use. But again, I said I don’t really desire to get into the whole “backwardation” thing and yet I did. But that’s ok, I don’t make a lot of friends with the way this mind works and quite humbly, maybe my perspective and considerations are in error.

Over the last couple of weeks and since my VIX-leveraged instrument of choice, UVXY, hit a new all-time trading low, the share price slipped into backwardation. As the share price is designed to decay in price over time, it actually rose by roughly 45% from a low $15.16 price to a peak trading price of $21.75 intraday on April 13, 2017. I had been craving some backwardation in the share price since covering a significant portion of Golden Capital Portfolio’s UVXY position at $15.85, as recently noted in the article titled UVXY: Market Uncertainty And Telling The Untold Future.

“Since authoring this article, I had reduced that position in shares of UVXY to roughly 15.2% of invested capital. With the Golden Capital Portfolio up nearly 50% year-to-date in a rather robust equity market that exhibits low levels of volatility, the portfolio’s alignment has been optimal or optimized to express great profit potential. And that is from whence I came into the year and found myself on March 17th, as Mr. Baldwin might say. As such and as recognized by my tweet above, I covered another significant portion (30,000 shares) of the portfolio’s short position in UVXY at $15.85 a share. This activity brought the Golden Capital Portfolio to a weighted UVXY short holding of roughly 11% with the recent reduction.”

I strongly urge investors and traders to read the totality of this article, as it quickly became one of my most viewed article on TalkMarkets.com. But back to my previous point regarding the spike in UVXY’s trading price. It was as the share price rose in the last two weeks that I have been able to recapture short positions in UVXY above and beyond the $18.50 level. It is often the case that during a share price rally in UVXY I will layer short positions and trade some of them for quick profits while pushing portions of the position into the core position. That core, short UVXY position in Golden Capital Portfolio has now risen to roughly 18.5% of the portfolio holdings and nearing its 20% holding benchmark. I consider covering significant portions of the core position previously at $15.85 and recapturing the positions short at or above $18.50 to be strong portfolio management.

Ok, so let’s get onto some of the more pressing matters for VIX-leveraged traders/investors in the coming week. And yes, I realize it’s not ok to start a sentence with “Ok”. Okay? First up we have a pretty tense weekend as the French election takes hold of global markets. The most desirable outcome for this French vote would be if the centrist candidates, former Economy Minister Emmanuel Macron or mainstream conservative Francois Fillon, takes more than 50 percent of the vote. Unfortunately, the early polls don’t bode well for such a result. The worst outcome, in terms of global equity markets, would be if the extreme right Marine Le Pen and far-left candidate Jean-Luc Melenchon capture the majority of the vote. This would possibly lead to global equity markets tumbling. Such a reaction may have already been foreshadowed by the falling 10yr U.S. Treasury yield as previously discussed, not to mention the bump in gold prices. Markets tend to predict or at least anticipate the future with the actions of today. CNBC’s Patti Domm offers the following commentary in her summation of the French election with the following:

“Citigroup analysts expect Macron to ultimately win, with a 35 percent probability, and they say he would go into the race with a good margin against all other candidates in the second round. Fillon would be second most likely, with a 30 percent probability, and Le Pen's odds are about 25 percent. The analysts see a small 10 percent probability for Melenchon.

"That gives a 65 percent likelihood of a risk-on, pro-EU final outcome and 35 percent probability for a risk-off, anti-EU outcome. A market-benign outcome still seems most likely but there is a meaningful risk that something more worrying happens," the Citi analysts wrote.

But Bank of America Merrill Lynch believes a victory by Fillon in the first round would not be a positive for markets, since he could potentially lose to one of the extremist candidates in the second round.

"There are more negative than neutral or positive scenarios," said Mark Cabana, head of U.S. short rate strategy at BofA.

Regardless of the outcome, it seems as though investors/traders would have been wise to have ample cash on hands to trade the post-election environment. For those who have followed my trading history over the years, you will likely recall my Brexit trading plans and my post-Brexit trading strategy as outlined in the articles below:

- UVXY Strategy For Brexit

- UVXY: The Post Brexit And End Of Quarter Market Environment Trading Opportunity

As everyone was clamoring and fretting over the Brexit vote by going long VIX/volatility, I stood pat with my tried and true strategy of maintaining a healthy amount of cash to short VIX-leveraged instruments and/or volatility should it spike. How’d I do? “Aint I a stinker”? (Bugs Bunny famous quote)

My strategy hasn’t changed from the Brexit event and for the sake of the upcoming French vote. I tend to lean on the Efficient Market Hypothesis with regards to maximizing the potential ROI from any risk on or risk off event. If everyone one is buying VIX/volatility, be where they aren’t. In truth, Monday morning global equities and futures could look ugly, benign or defiant of fear altogether; we simply won’t know until we know. But always be prepared for the worst and delighted by the best outcomes. So what’s next? I’m glad you asked.

There’s a good deal of mixed-messaging coming from the media presently and with regards to a possible Trump Administration Tax Reform proposal to come as early as Wednesday. In traditional Donald Trump fashion, he offered his sentiment with a tweet stating quite clearly that a Tax Reform and Tax Reduction proposal would be announced Wednesday. On Friday, Bloomberg cited a senior administration official as saying the new tax plan was unlikely to include a border-adjusted tax backed by House Speaker Paul Ryan, which has divided Republicans. That could be really good news for the retail and consumer goods sector stocks. Of course, we’ll have to see what exactly is in the Tax Reform and Reduction proposal.

With macro risks that include the possibility of a U.S. Government shutdown next week, earnings season kicks into high gear as well. The lineup of earnings reports accounts for around 40% of the benchmark index's value, or more than $7.7 trillion, and includes big names like Alphabet Inc (GOOGL), Amazon.com Inc (AMZN), and Exxon Mobil Corp (XOM).

“The first three months of the year now appear set to mark the strongest quarterly earnings growth in more than five years. In the last week alone, expected S&P 500 first-quarter earnings per share growth rose to 11.2 percent from 10.4 percent, a more than 7 percent jump, according to Thomson Reuters data.”

Thursday marks a day of high interest for the Golden Capital Portfolio as I recently added shares of Starbucks (SBUX) to the portfolio at $56.70 a share and the company will report its quarterly results. Additionally, other key investments in the portfolio will be reporting that same day such as Microsoft (MSFT) and Intel Corp (INTC). Recently I had reduced exposure to these two investments as the gains since 2013 warranted profit taking as well as risk management. We’ll see what this reporting cycle bears out for these investments and if an opportunity to reload is presented in any of the names.

Final Thought

The key takeaway here and as exampled within this narrative is that macro-headlines have proven to dominate market movements for very brief periods of time. Ultimately, earnings drive market performance long-term and while it may be difficult to consider long-term performance given near-term risk factors, the greater returns on capital come from long-term consideration interlaced with risk management.

The Golden Capital Portfolio has been managed since 2012 to take full advantage of certain VIX-leveraged instruments, UVXY and VXX mainly. The ideal outcome regarding the start of the trading week would be a benign French vote that exhibits a mild global equity reaction. Such a reaction may express little volatility and aid in the decaying of UVXY and VXX share prices. Then again it may not, as for a singular trading day anything is probable. Harkening back to what I previously stated, however, the long-term outcome for these ETFs is not left to chance, as they will decay in price per design. But if Monday morning should not express a decay in share price due to an unfavorable French vote, I will be attempting to capture the full 20% core UVXY holdings in Golden Capital Portfolio and in the $20 range. If you desire to know exactly when I position a trade execution I often disseminate them through my real-time Twitter feed.

Comments

Log in or sign up to join the conversation.