Top Analysts Look For Growth In Yahoo! Inc’s Quarterly Report

Yahoo! Inc (NASDAQ: YHOO) will report first quarter 2015 earnings today after market close. Analysts will be looking for Yahoo’s progress in mobile, video, native, and social (MVNS). Furthermore, analysts are anticipating an update on the Alibaba (NYSE: BABA) spin-off.

Analysts estimate that Yahoo will post non-GAAP earnings per share of $0.018, down from $0.38 year-over-year and down from $0.30 sequentially. Analysts estimate quarterly revenue of $1.06 billion, down from $1.13 billion year-over-year and down from $1.25 billion sequentially.

Yahoo has been carried by Alibaba since the Chinese e-commerce company released a record-breaking IPO in September. Now, Yahoo will be spinning off what stake it has left in Alibaba into an independent investment company called SpinCo. Analysts hope this move will allow Yahoo to focus on growing its core business while giving value back to shareholders.

Analysts also hope that Yahoo will be able to expand its MVNS. Yahoo purchased BrightRoll in December, a platform that automates video advertisements and streamlines the process of planning a video campaign. Analysts are looking to this acquisition to boost display revenue in the quarterly report.

In December, Yahoo replaced Google as Firefox’s default search engine in the U.S., helping Yahoo cut into Google’s overwhelming market share. Furthermore, Yahoo’s president and CEO, Marissa Mayers, negotiated Yahoo’s search alliance with Microsoft in order to give Yahoo more autonomy to control searches.

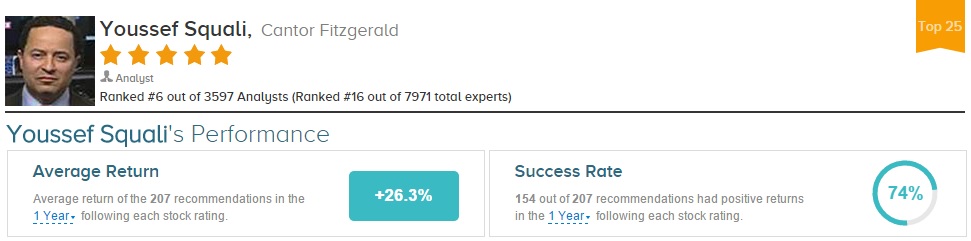

Yesterday, analyst Youssef Squali of Cantor Fitzgerald reiterated a Buy rating on Yahoo with a $60 price target. Squali commented that Yahoo has made “significant progress in company culture, product improvement, [and] user engagement in the last two years.” However, Squali continued, Yahoo has been “sorely lacking” in meaningful “monetization and revenue growth.” Although Yahoo’s MVNS has “strong traction,” this growth has been “more than offset” by PC revenue decreases. Squali is anticipating flat year-over-year revenue growth in today’s report. Looking forward, the analyst notes that Yahoo management needs to “grow core Yahoo! again, with a clear path that gets it closer to industry rates” in order for the stock to succeed after the Alibaba stake spin-off.

Youssef Squali has rated Yahoo 25 times since April 2009, earning a 68% success rate recommending the stock with a +13.7% average return per YHOO recommendation. Overall, Squali has a 74% success rate recommending stocks with a +26.3% average return per rating.

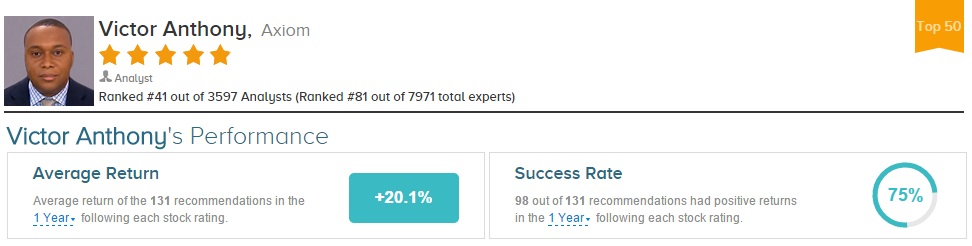

Separately, analyst Victor Anthony of Axiom Capital also reiterated a Buy rating on Yahoo yesterday, but slightly lowered his price target from $52 to $51 due to Alibaba’s price decline. Like Squali, Anthony sees improved investments in MVNS but thinks this is “unlikely to show overall Core improvement.” However, Anthony is bullish on the stock due to the “tax-free spin-off of the Alibaba shares, a potential monetization of Yahoo Japan further down the road, efforts to improve the Core business, and the continued equity shrink.” Anthony lists 11 questions he would address to Yahoo CEO Marissa Mayer, ranging from Yahoo’s relationship with different search engines to a timeline for monetizing Yahoo! Japan.

Victor Anthony has rated Yahoo 13 times since April 2013, earning a 77% success rate recommending the stock with a +17.7% average return per YHOO rating. Overall, Anthony has a 75% overall success rate recommending stocks with a +20.1% average return per rating.

On average, the top analyst consensus for Yahoo on TipRanks is Moderate Buy.

Disclosure: To see more visit TipRanks today.

more