Morning Call For Wednesday, Nov. 16

OVERNIGHT MARKETS AND NEWS

Dec E-mini S&Ps (ESZ16 -0.34%) are down -0.23% as they retreat from a new contract high posted in overnight trade and European stocks are down -0.44% after weaker oil prices and interest rate concerns pressured equities. Dec WTI crude oil (CLZ16 -1.24%)is down -1.57% after the API late yesterday reported that U.S. crude stockpiles rose +3.65 million bbl last week. The chances of a Fed rate hike at the Dec FOMC meeting increased after St. Louis Fed President Bullard (voter) said that December would be a "reasonable time" to raise interest rates. Asian stocks settled mixed: Japan +1.10%, Hong Kong -0.19%, China -0.06%, Taiwan +0.35%, Australia +0.03%, Singapore -0.13%, South Korea +0.45%, India -0.02%. The Chinese yuan tumbled to a 7-3/4 year low against the dollar on concern over President-elect Trump's trade policies, while Japan's Nikkei Stock Index climbed to a 9-1/2 month high as exporter stocks rallied when USD/JPY rose to a 5-1/2 month high, which boosts the earnings prospects of exporters.

The dollar index (DXY00 +0.27%) is up +0.23% at an 11-1/2 month high on the prospects for a Fed rate hike at next month's FOMC meeting. EUR/USD (^EURUSD) is down -0.28% at an 11-1/2 month low. USD/JPY (^USDJPY) is up +0.49% at a 5-1/2 month high.

Dec 10-year T-note prices (ZNZ16 -0.28%) are down -11 ticks on hawkish comments from St. Louis Fed President Bullard.

St. Louis Fed President Bullard (voter) said that December would be a "reasonable time" to raise interest rates and that you would have to see a surprise to stop a December rate hike.

U.S. STOCK PREVIEW

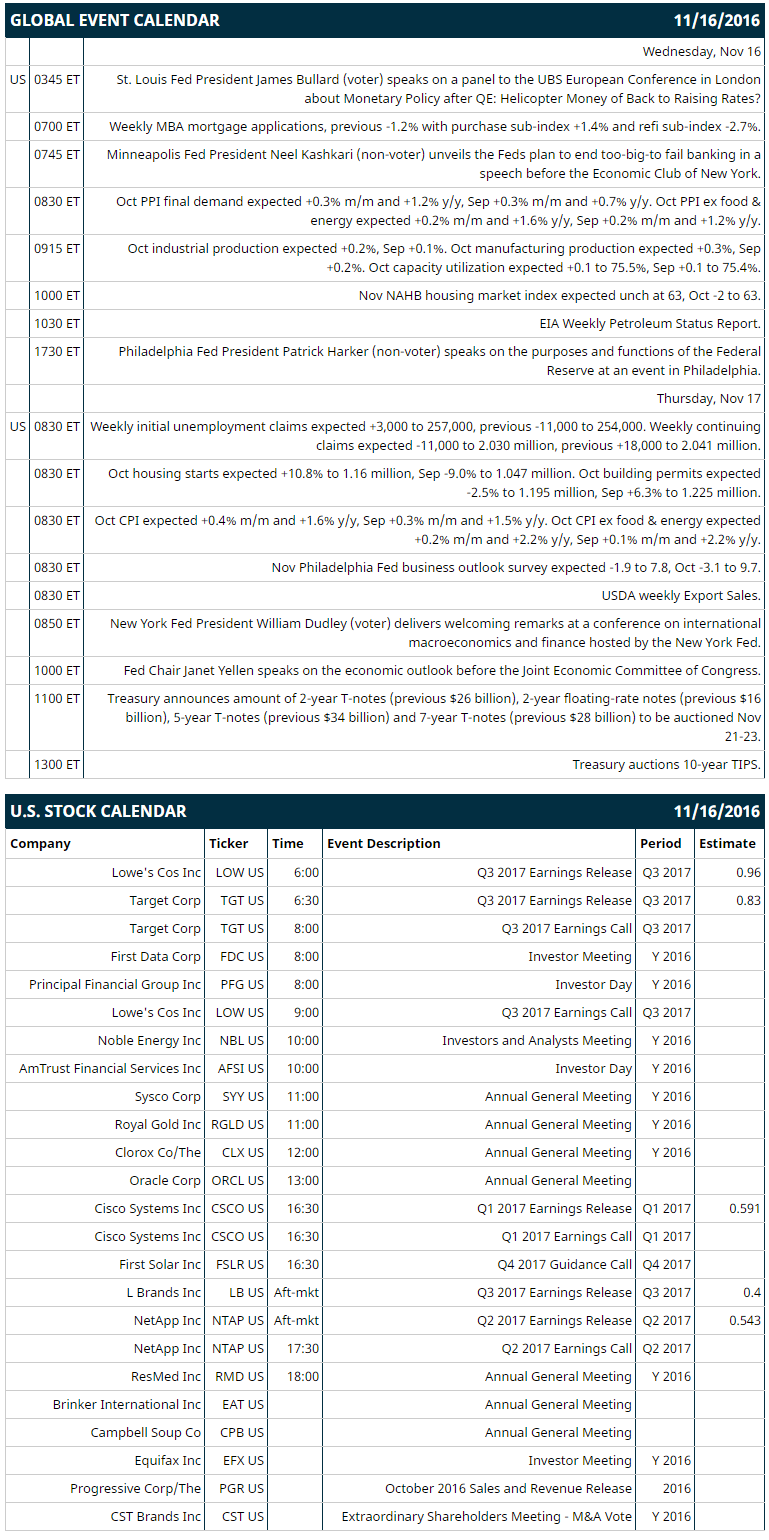

Key U.S. news today includes: (1) St. Louis Fed President James Bullard (voter) speaks on a panel to the UBS European Conference in London about “Monetary Policy after QE: Helicopter Money of Back to Raising Rates?," (2) weekly MBA mortgage applications (previous -1.2% with purchase sub-index +1.4% and refi sub-index -2.7%), (3) Minneapolis Fed President Neel Kashkari (non-voter) unveils the Fed’s plan to end too-big-to fail banking in a speech before the Economic Club of New York, (4) Oct PPI final demand (expected +0.3% m/m and +1.2% y/y, Sep +0.3% m/m and +0.7% y/y) and Oct PPI ex food & energy (expected +0.2% m/m and +1.6% y/y, Sep +0.2% m/m and +1.2% y/y), (5) Oct industrial production (expected +0.2%, Sep +0.1%) (6) Nov NAHB housing market index (expected unch at 63, Oct -2 to 63), (7) Philadelphia Fed President Patrick Harker (non-voter) speaks on the purposes and functions of the Federal Reserve at an event in Philadelphia, and (8) EIA Weekly Petroleum Status Report.

S&P 500 earnings reports today include: Target (consensus $0.83), Lowe's (0.96), Cisco Systems (0.59), L Brands (0.40), NetApp (0.54).

U.S. IPO's scheduled to price today: none.

Equity conferences this week include: UBS Global Technology Conference on Mon-Wed, Bank of America Merrill Lynch Banking & Financial Services Conference on Tue-Wed, Stifel, Nicolaus & Co Health Care Conference on Tue-Wed, Morgan Stanley Global Consumer & Retail Conference on Tue-Thu, Barclays Select Series Conference on Wed, Goldman Sachs Metals and Mining Conference on Wed, William Blair Financial Technology and Services Summit on Wed, Bank of America Merrill Lynch Global Energy Conference on Wed-Thu, Jefferies London Health Care Conference on Wed-Thu, Canaccord Genuity Medical Technology and Diagnostics Forum on Thu, Vertical Research Partners Global Materials Conference on Thu, UBS Industrials and Transportation Conference on Thum, Morgan Stanley European Technology, Media & Telecom Conference on Fri.

OVERNIGHT U.S. STOCK MOVERS

Lowe's (LOW -1.37%) fell over 5% in pre-market trading after it reported Q3 adjusted EPS of 88 cents, weaker than consensus of 96 cents, and then cut its full-year EPS view to $3.52 from an August 17 view of $4.06.

Sysco (SYY +0.02%) was downgraded to 'Neutral' from 'Outperform' at Credit Suisse.

Target (TGT -1.01%) jumped nearly 6% in pre-market trading after it reported Q3 adjusted EPS of $1.04, well above consensus of 83 cents, and then raised guidance on fiscal 2017 adjusted EPS to $5.10-$5.30 from an August 17 view of $4.80-$5.20.

Lululemon Athletica (LULU -1.76%) lost over 1% in pre-market trading after it was downgraded to 'Neutral' from 'Buy' at Credit Suisse Group AG.

OSI Systems (OSIS -1.88%) was rated a new 'Buy' at Drexel Hamilton LLC with a 12-month target price of $90.

ViaSat (VSAT +0.25%) slid over 2% in after-hours trading after it proposed a 6.5 million offering of common stock.

Agilient Technologies (A +0.15%) gained almost 2% in after-hours trading after it reported Q4 adjusted continuing operations EPS of 59 cents, above consensus of 52 cents.

CACI International (CACI -3.00%) was rated a new 'Buy' at Drexel Hamilton LLC with a 12-month target price of $140.

Flexion Therapeutics (FLXN -3.24%) dropped nearly 8% in after-hours trading after it proposed an offering of stock, with no amount given.

MACOM Technology Solutions Holdings (MTSI +1.74%) fell over 3% in after-hours trading after it reported Q4 adjusted EPS of 54 cents, below consensus of 56 cents.

La-Z-Boy (LZB -0.76%) climbed 5% in after-hours trading after it purchased the UK and Ireland licenses from Furnico and said it bought 9 La-Z-Boy furniture galleries in Pennsylvania and both deals should add $41 million in incremental sales volume.

Aclaris Therapeutics (ACRS +4.04%) gained over 2% in after-hours trading after it is said it met all endpoints in a Phase 3 study of its A-101 40% Topical Solution for seborrheic keratosis.

Invitae (NVTA -1.04%) dropped 6% in after-hours trading after it proposed a $40 million offering of common stock.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ16 -0.34%) this morning are down -5.00 points (-0.23%). Tuesday's closes: S&P 500 +0.75%, Dow Jones +0.29%, Nasdaq +1.33%. The S&P 500 on Tuesday closed higher on positive economic data with the (1) +0.8% increase in U.S. Oct retail sales and +0.8% increase in Oct retail sales ex-autos, stronger than expectations of +0.6% and +0.5% ex-autos, and (2) the +8.3 point jump in the U.S. Nov Empire manufacturing index to a 5-month high of 1.5, stronger than expectations of +4.3 to -2.5. Stocks were also boosted by a rally in energy producer stocks after the price of crude oil surged +5.61% on optimism that OPEC may reach an oil production cut agreement.

Dec 10-year T-notes (ZNZ16 -0.28%) this morning are down -11 ticks. Tuesday's closes: TYZ6 -7.50, FVZ6 -4.75. Dec 10-year T-notes on Tuesday closed lower on the stronger-than-expected U.S. Oct retail sales report, which boosts the chances of a Fed rate hike next month. T-notes were also undercut by reduced safe-haven demand with the rally in stocks.

The dollar index (DXY00 +0.27%) this morning is up +0.23 (+0.23%) at a fresh 11-1/2 month high. EUR/USD (^EURUSD) is down -0.0030 (-0.28%) at an 11-1/2 month low. USD/JPY (^USDJPY) is up +0.54 (+0.49%) at a 5-1/2 month high. Tuesday's closes: Dollar index +0.120 (+0.12%), EUR/USD -0.0015 (-0.14%), USD/JPY +0.78 (+0.72%). The dollar index on Tuesday climbed to a fresh 11-1/4 month high and closed higher. The dollar index was boosted by the stronger-than-expected U.S. Oct retail sales report, which bolsters the outlook for the Fed to raise interest rates. There was also reduced safe-haven demand for the yen as gains in the equity market spurred a rally in USD/JPY to a 5-1/4 month high.

Dec crude oil prices (CLZ16 -1.24%) are down -72 cents (-1.57%) and Dec gasoline (RBZ16 +0.10%) is -0.0021 (-0.16%). Tuesday's closes: Dec crude +2.43 (+5.61%), Dec gasoline +0.0570 (+4.46%). Dec crude oil and gasoline on Tuesday closed sharply higher as Qatar, Algeria and Venezuela work to secure a deal between Saudi Arabia, Iran and Iraq on how to share crude output cuts. Crude oil prices were also boosted by renewed attacks on Nigerian oil installations by rebels, which may curb oil supplies from Nigeria, Africa's biggest crude producer.

Disclosure: None.