The S&P 500 In Weeks 3 And 4 Of November 2016

We're catching up with two weeks worth of action in the S&P 500, so let's start with what stood out during Week 3 of November 2016.

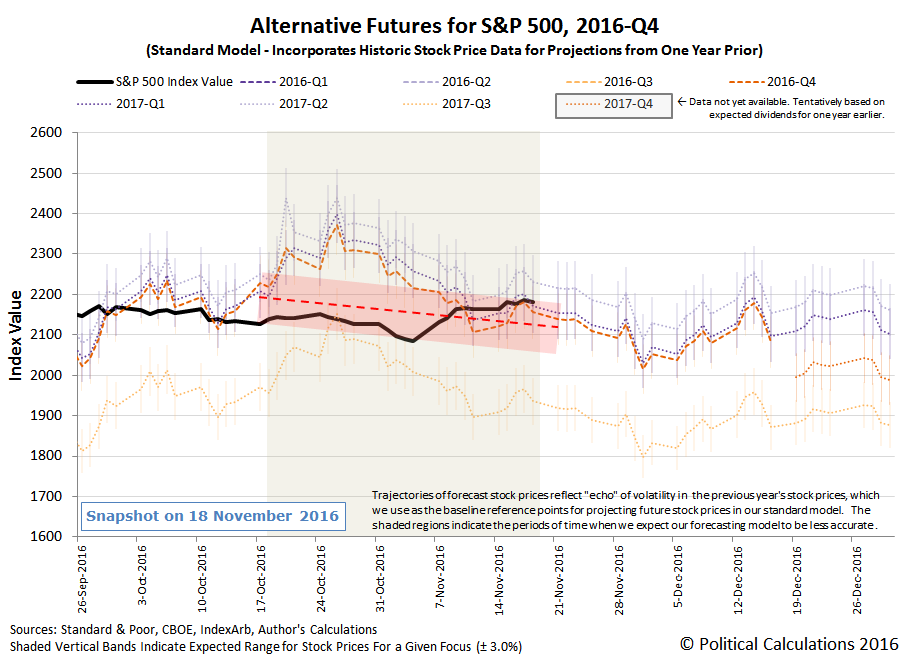

First and foremost, our prediction from five weeks ago appears to have held throughout nearly every trading day of the last five weeks, with the S&P 500 actual values consistently falling within 3% of the red-dotted line that we sketched on top of our standard forecasting model to anticipate its future trajectory at that time, as almost indicated by the hand-drawn red-shaded region (since we drew it slightly narrower than intended).

In the chart above, our hand drawn forecast applies only to the period where our standard model would be affected by the echo effect from past volatility (indicated as the brown-shaded region), which is an artifact of our model's use of historic stock prices from 1 month, 12 months and 13 months earlier in its projections of future stock prices. To work around the echo effect, we literally connected the dots corresponding to the trajectory associated with 2016-Q4 on both sides of the period we identified over five weeks ago where we anticipated that our model's projections would be less accurate than usual.

Back then, we assumed that investors would keep their forward-looking focus fixed on the very near term future defined by the expectations associated with the current quarter of 2016-Q4, which we predicted would be the case as investors would be greatly influenced by their concerns over the Fed's plans to hike short term interest rates, where that concern would largely trump (pun intended) any noise introduced by the U.S. national elections.

Speaking of which, the outcome of the elections contributed quite a lot of noise, where the actual trajectory of the S&P 500 swung from the low end of our forecast range to the high end. That said, coming out of Week 3 of November 2016, it would appear that investors remained focused on 2016-Q4 in setting current day stock prices.

Here are the headlines that we identified as being relevant to the stock market in Week 3 of November 2016:

Monday, 14 November 2016

- Too early to tell impact of Trump policies: Fed's Kaplan

- Wall Street ends flat as financials' rise offsets tech drop

Tuesday, 15 November 2016

- Fed won't be easily swayed from December rate hike: Rosengren

- Washington stimulus would bring more rate hikes: Fed's Rosengren

- This story provides a pretty good example of why changes in fiscal policy (changes in government spending or taxation) often fail to deliver intended results, which happens because central banks use monetary policy to offset the effects of fiscal policy.

- Oil prices jump 3 percent on hopes of OPEC output cut

- Wall Street rises, lifted by technology and energy stocks

Wednesday, 16 November 2016

- Only a surprise will halt December Fed rate hike: Bullard

- A surprising observation: Market reaction to Trump more muted than expected: Fed's Bullard

- Setting future expectations: Fed's Bullard says low interest era not expected to end

- Dow, S&P drop as financials' rally ebbs, tech boosts Nasdaq

Thursday, 17 November 2016

- Fed's Harker says he supports an interest rate hike

- U.S. needs higher rates; banks need more capital: FDIC's Hoenig

- Oil falls as stronger dollar outweighs OPEC deal optimism

- U.S. dollar, stocks climb as Yellen signals rate hike coming

- Wall street stocks lifted by data, earnings Yellen remarks

Friday, 18 November 2016

- Fed's Bullard leaning toward supporting December rate hike

- Post-election markets not concerning for Fed policy plan: Dudley

- Wall Street slips, led by healthcare decline

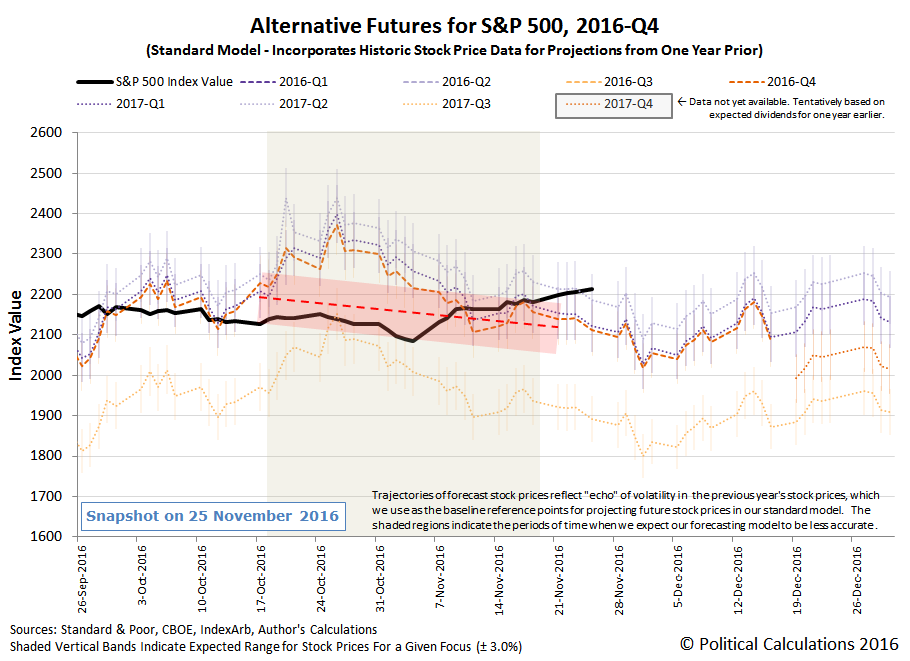

Now, let's move into Week 4 of November 2016, where something more interesting happened in a Thanksgiving holiday-shortened week.

For investors focusing on the future, the big news of the week was the shift in how far forward investors were looking, which changed from 2016-Q4 to 2017-Q2 during the course of the week.

As for what caused that shift, here are the news items for which we took special note of during Week 4 of November 2016.

Monday, 21 November 2016

- Oil rally propels Wall Street to record

- Dollar's rise won't blind Fed to its goals, Fischer says

- Major indexes hit records as post-election rally goes on

Tuesday, 22 November 2016

- Oil prices end near flat on uncertain outcome from OPEC meeting

- Wall Street extends record streak, Dow breaks 19,000 for first time

Wednesday, 23 November 2016

- Oil prices edge down on doubts about OPEC-led cuts

- Fed policymakers confident of need for rate hikes on eve of Trump win

- This is the biggest news of the week. Following the release of the Fed's 2 November 2016 FOMC statement, this news all but locked in the probability of a December 2016 hike in short term interest rates at 100%, which freed investors to look beyond the current quarter of 2016-Q4 and the Fed's December meeting to look at the more distant future. Based on what we've observed, investors have shifted their focus to 2017-Q2, which accounts for the continuing rise in the S&P 500 off its pre-election lows during the past week. In addition to confirming that change in our chart above, that shift in how far forward investors shifted their attention was surprisingly captured in at least one contemporary news source: Get Ready for Higher Interest Rates, Fed Minutes Say, where June 2017 (the month ending 2017-Q2) would coincide with current expectations of the timing of the Fed's next short term rate hike after December 2016.

- Dow, S&P close at records; U.S. yields, dollar at multi-year highs

Friday, 25 November 2016

- Oil falls $2 a barrel on OPEC cut uncertainty ahead of meeting

- Wall Street finishes at record highs consumer staples, techs gain

Elsewhere, Barry Ritholtz divided the economic and market news into its positives and negatives for both Week 3 and Week 4of November 2016.

Looking forward over the next couple of weeks, in the absence of more fundamental events to change expectations or new noise events, we think that the S&P 500 will continue running to the high side of our forecast range for 2017-Q2, which shows the effects of a small echo from late 2015. That said, pay attention to the difference in where stock prices can be expected to go if investors focus on either 2017-Q2 or 2017-Q3. Unless the expectations for the change in the growth rate of future dividends for 2017-Q3 improves significantly, any news that would reasonably delay the expected timing of the Fed's next rate hike out of 2017-Q2 would likely coincide with a significant downward change in U.S. stock prices.

Disclosure: None.