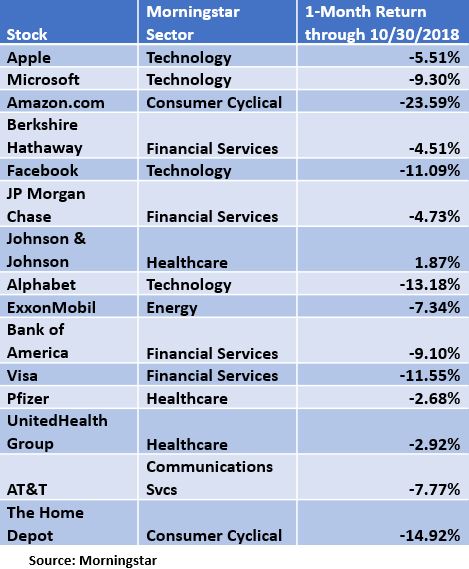

The S&P 500 Index dropped 6.84%, including dividends in a showing that was a rude awakening for investors who had, once again, become complacent. The beginning of this year was marked by a surge in January following a year in which the index didn’t drop for a single month. But after February and March wiped out January’s gains, rattled investors relaxed once again. Now that everyone’s on high alert again, it’s a decent time to see which stocks and sectors held up for the month. Keep in mind that our numbers are 1-month returns through October 30th, according to Morningstar, and stocks rallied on the 31st.

First, as we look at the top positions of the S&P 500 Index, it’s striking how many companies are technology or financial services companies, according to Morningstar’s classification. It seems like that’s what our economy consists of now – wealthy people checking their investment accounts on iPhones and less-than-wealthy people doing other things on cheaper phones.

In any case, the month wasn’t kind to FAANG stocks. Although Apple held up with a -5.5% showing through Oct. 30th, Amazon dropped more than 20%. Facebook dropped more than 10% and Alphabet more than 13%. Although not a top-15 index position, Netflix dropped more than 20% for the month through Oct. 30th.

The clear winners were healthcare stocks. Johnson & Johnson gained nearly 2%, making it the only top-15 constituent to post a positive return. Another pharmaceutical firm, Pfizer, and health insurance giant, UnitedHealth Group (UNH), managed to keep their losses to less than 3% each.

Financial services had a mixed showing. Berkshire Hathaway dropped less than 5%, as did JP Morgan Chase. But Bank of America shed 9%, and Visa dropped nearly 12%.

Defensive Sectors And Healthcare Shine

Since we can’t get a good cross-section of sectors by looking at the top-15 constituents of the index, let’s move to the sectors themselves as represented by ETFs. Here the returns will be on a 1-month basis through Oct 30th. It turns out the defensive sectors that pay dividends held up.The SPDR Utilities Select Sector SPDR ETF (XLU) posted a 1.98% 1-month gain. Similarly, the iShares Cohen & Steers REIT ETF (ICF) dropped 1.47%. The Consumer Staples Select Sector SPDR ETF (XLP) posted a 2% 1-month gain, while the iShares. U.S. Financials ETF (IYF) lost around 5%. The iShares U.S. Healthcare ETF (IYH) lost a little more than 7%.

The more negative sectors were consumer discretionary, industrials, energy, and materials. Consumer Discretionary Select Sector SPDR ETF posted an 11.24% 1-month loss. The iShares U.S. Industrials ETF dropped nearly 11%, while the iShares U.S. Energy ETF dropped around 12% for the month. The Materials Select SPDR ETF dropped around 9%.

Bonds Didn’t Rally

On the bond side, short-term U.S. Treasuries did fine, but didn’t experience the rally that sometimes goes with a plunging stock market. The iShares Short Treasury ETF (SHV) gained 0.16% for the 1-month period through Oct. 30th. Treasuries with longer duration struggled, however. The iShares 10-20 year Treasury Bond ETF (TLH) lost around 1% for the 1-month period.

Intermediate investment grade corporates also struggled. The iShares Investment grade Corporate Bond ETF (LQD) dropped around 1.8% for the 1-month period. High yield or junk bonds didn’t do worse, however, with the iShares High Yield Corporate Bond ETF (HYG) also dropping 1.8%.

Municipals held up fine too, but, like Treasuries, didn’t rally either. The iShares Short Maturity Municipal Bond ETF (MEAR) gained 0.03%, while the iShares National Muni Bond ETF (MUB), with an average maturity of more than 6 years, dropped 0.39%.

The worst performing bonds were emerging markets dollar-denominated government bonds. The J.P. Morgan USD Emerging Markets Bond ETF (EMB) lost 2.52% for the 1-month period. By contrast, the iShares J.P. Morgan EM Local Currency Bond ETF (LEMB) gained 0.51% for the 1-month period. The discrepancy of the returns in these two funds shows the effects of the U.S. dollar which continued to strengthen. When emerging markets countries have to pay debt in dollars, it hurts them when the U.S. dollar rises against other currencies.

One is tempted to say that the absence of a Treasury rally might mean a new normal for interest rates. But a still-flat yield curve makes it difficult to be certain of that outcome.

Comments

Log in or sign up to join the conversation.