Technically Speaking: Tis But A Flesh Wound

In this past weekend’s missive, I discussed the recent market sell-off:

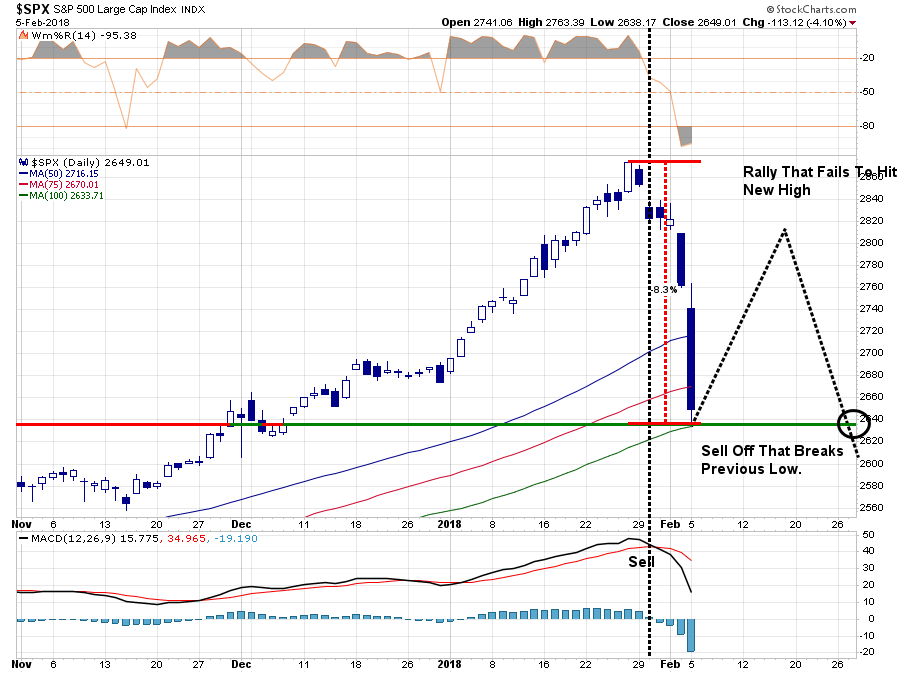

“Well, this past week, the market tripped ‘over its own feet’ after prices had created a massive extension above the 50-dma as shown below. As I have previously warned, since that extension was so large, a correction just back to the moving average at this point will require nearly a -6% decline.”

Chart updated through Monday

(Click on image to enlarge)

“I have also repeatedly written over the last year:

‘The problem is that it has been so long since investors have even seen a 2-3% correction, a correction of 5%, or more, will ‘feel’ much worse than it actually is which will lead to ’emotionally driven’ mistakes.’

The question now, of course, is do you “buy the dip” or ‘run for the hills?’

Don’t do either one, yet.

Yes, corrections do not ‘feel’ good. But they are part of a ‘healthy’ market cycle. In more normal, healthy, bullish trends corrections should be used as buying opportunities to increase exposure to equity risk in portfolios.”

Yesterday morning, the markets began the day deeply in the red, but by mid-morning were flirting with positive territory before sliding lower again. By the end of the day, the Dow had posted its largest one-day point loss in history.

Not surprisingly, by the end of it all, bonds were up sharply, as anticipated, as investors sought safety from the sell-off.

While the market found support at the 100-dma, an attempt to bounce is still anticipated from the short-term “oversold” conditions that have now developed during the “bloodletting.”

“At the moment, this is the expected correction we have been discussing over the last several weeks. It is also something we had planned for by reducing overweight positions and adding a short-hedge to portfolios.”

(Click on image to enlarge)

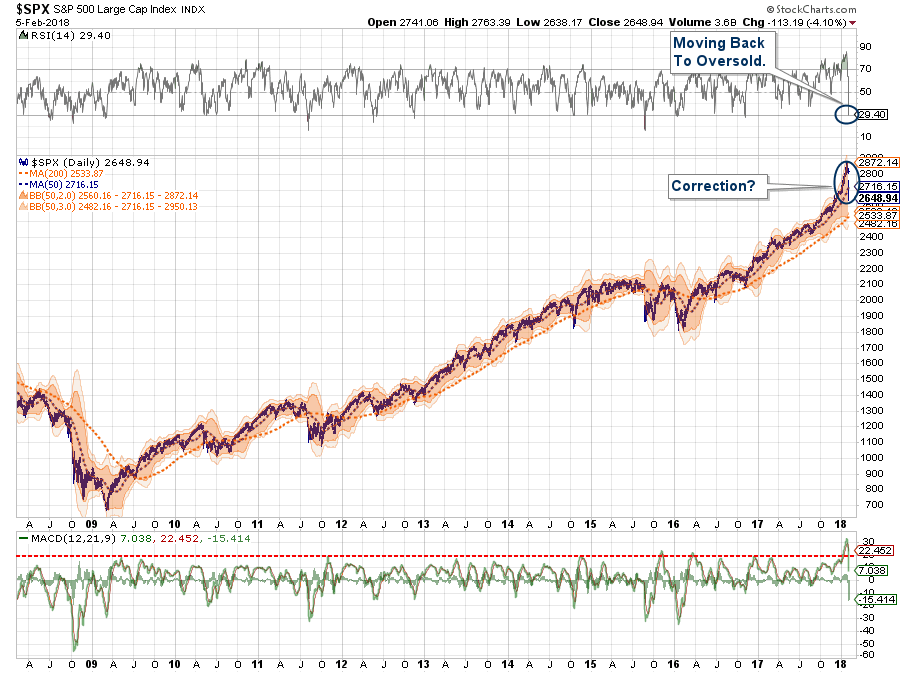

With yesterday’s sell-off, the markets are on a short-term sell signal which continues to apply downward pressure. However, the with the market now oversold on a VERY short-term basis (red circles), a rally over the next day, or so, would not be surprising.

As I noted, it is the outcome of any rally which is most important to the current bull market advance.

This is what we are looking for to drive our next set of portfolio actions:

- If the market rallies back and sets a new closing high, the bullish trend will be confirmed and equity allocations will remain at target levels and hedges removed.

- If the market rallies back BUT FAILS to set a new high, a series of actions will take place.

- At the point of rally failure, portfolio hedges will be modestly increased.

- If the subsequent decline breaks the previous low, the hedges will be further increased and tactical trading long positions will be reduced.

With the “sell signal” being issued at such a high level technically, I certainly expect any rally to ultimately fail before setting new highs. As stated, any failed rally will be used to reduce long-equity exposure and rebalance hedges accordingly.

Just A Flesh Wound

Yes, the correction has certainly “felt” much worse than it actually was. In fact, to steal a line from Monty Python, “tis but a flesh wound.”

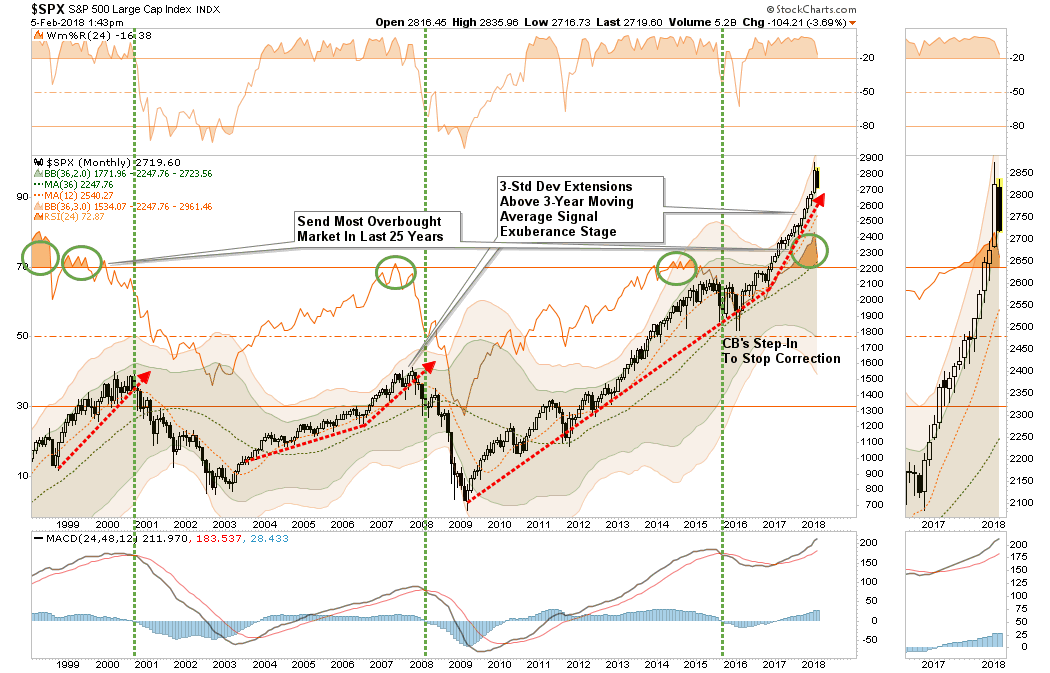

Before we get into the short-term view, let’s keep the current correction within the context of the bigger picture. In the context of the ongoing bull market trend, the correction is, well, just that. Corrections are a part of a healthy market process.

But keep in mind the recent market advance has been anything but normal. The market, as measured by the S&P 500 index, had gone 112 trading days without closing lower than 1% in a single day, or 349-days without a 2% decline, both of which were the longest streak in 30-years.

Therefore, it should NOT be surprising that with such an ABNORMAL advance you would also see a more ABNORMAL correction.

Such is the nature of markets, corrections and mean reversions.

The good news, if you want to call it that, is on a very short-term basis the market has worked off much of the temporary overbought condition.

(Click on image to enlarge)

Putting corrections into perspective should help reduce the “emotional stress” caused by such events. While we certainly understand the “emotional need” to “do something,” such is often the worst thing you can do.

“The investor’s chief problem—and even his worst enemy—is likely to be himself.” – Benjamin Graham

We have been warning for weeks that such an event would occur. We have also repeatedly recommended various actions to take to reduce inherent portfolio risk. To wit:

“The combined overbought, over-leveraged condition of the financial markets is of extreme risk to investors currently. While the bullish trend remains intact currently, it is extremely prudent to perform some risk management in portfolios.

It is worth remembering that portfolios, like a garden, must be carefully tended to otherwise the bounty will be reclaimed by nature itself.

- If fruits are not harvested (profit taking) they ‘rot on the vine.’

- If weeds are not pulled (sell losers), they will choke out the garden.

- If the soil is not fertilized (savings), then the garden will fail to produce as successfully as it could.

So, as a reminder, and considering where the markets are currently, here are the rules for managing your garden:

1) HARVEST: Reduce “winners” back to original portfolio weights. This does NOT mean sell the whole position. You pluck the tomatoes off the vine, not yank the whole plant from the ground.

2) WEED: Sell losers and laggards and remove them from the garden. If you do not sell losers and laggards, they reduce the performance of the portfolio over time by absorbing “nutrients” that could be used for more productive plants. The first rule of thumb in investing “sell losers short.”

3) FERTILIZE AND WATER: Add savings on a regular basis. A garden cannot grow if the soil is depleted of nutrients or lost to erosion. Likewise, a portfolio cannot grow if capital is not contributed regularly to replace capital lost due to erosion and loss. If you think you will NEVER LOSE money investing in the markets…then STOP investing immediately.

4) WATCH THE WEATHER: Pay attention to markets. A garden can quickly be destroyed by a winter freeze or drought. Not paying attention to the major market trends can have devastating effects on your portfolio if you fail to see the turn for the worse. As with a garden, it has never been harmful to put protections in place for expected bad weather that didn’t occur. Likewise, a portfolio protected against “risk” in the short-term, never harmed investors in the long-term.

With overall market trend still bullish, there is little reason to become overly defensive in the very short-term. However, I have this nagging feeling the ‘spring’ is now wound so tightly, that when it does break loose, it will likely surprise most everyone.”

So, with these actions taken in portfolios already, there is little to do here but wait to see what the market does next.

As investors we DO NOT want to try and predict what the market will do. That is guessing, and guessing often leads to poor outcomes. We DO want to react to price action and make changes necessary to either increase or reduce related portfolio risk.

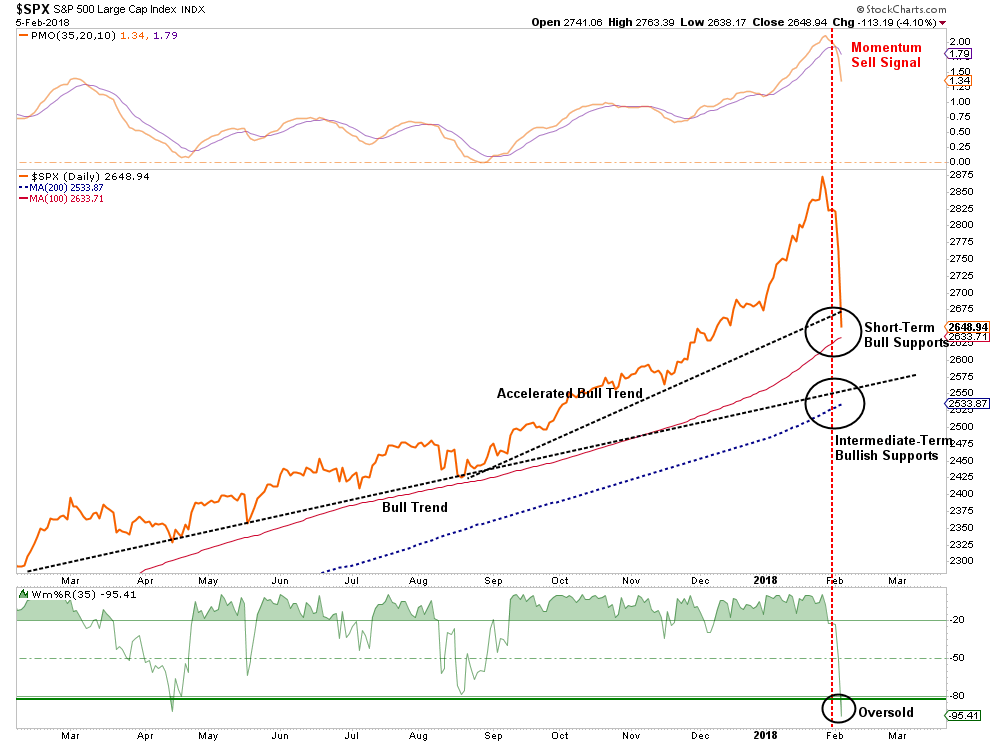

Currently, the market has done nothing except retrace to the short-term accelerated bullish trend line as shown below. It is also the intersection of the market with the 100-day moving average. These two supports provide a reasonable point for a market bounce, as discussed above, to rebalance risk into.

(Click on image to enlarge)

However, with the momentum “sell” signal registered at very high levels, it is conceivable the market could decline further. If the market fails to bounce, and breaks the 100-dma, it is highly probable the market will seek support at the intermediate bullish trend line which also coincides with the 200-dma. Such a decline would likely put the markets around 2550 which would equate to a -13% decline from the recent peak. Again, such a decline, while painful, is well within the context of a “normal and healthy” market correction.

The Bigger Correction Is Still Coming

Don’t misunderstand me.

While I am telling you “not to panic” about this short-term corrective action, I am NOT suggesting that everything is “just peachy” longer-term.

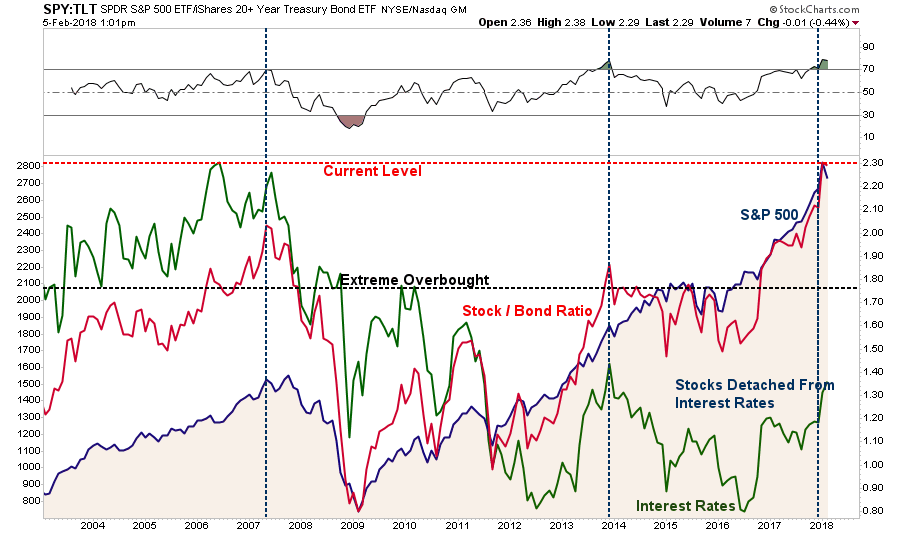

Very likely, this the first “shot across the bow” for investors. With the stock-bond ratio completely out of whack, there is a very relevant risk of a “re-coupling” as higher rates impact economic growth and earnings.

(Click on image to enlarge)

Furthermore, on a longer-term perspective of the market, the market remains egregiously overbought and bullish. Asset allocations are grossly overweight equity risk, cash levels are at historic lows, and margin-debt is near record levels. As shown in the chart below, the recent corrective action has done little to rebalance equity risk in the markets to any significant degree.

That correction is still coming in the months ahead which will most likely coincide with the onset of a recessionary contraction in the economy.

(Click on image to enlarge)

As I noted this past weekend, the next bull market will likely be in bonds, not stocks. As our analyst John Coumarianos recently noted:

“PIMCO’s Dan Ivascyn and Mark Kiesel say 3% yield on 10-Year Treasuries might be a signal to buy, according to another Bloomberg article. The article quotes Ivascyn saying ‘[T]here’ll be buyers of bonds if we back up to 3 percent,'”

This is likely particularly as investors begin to quickly equate the risk of being long equity risk with a sub-2% dividend yield versus the safety U.S. Treasuries with a yield of 3%.

Furthermore, given the extreme long-term “oversold” condition of bonds, versus the still extreme long-term “overbought” condition of stocks, the risk/return ratio is clearly in favor of bonds currently. Such will become much more pronounced particularly as economic strength wanes over the coming months as the temporary boost provided by a slate of natural disasters fades.

While I am certainly not now, nor have I been a “raging bull,” I also remain steadfastly dedicated to evaluating risk and acting accordingly. It is important NOT to mistake a short-term correction for a full-blown reversion.

Keeping perspective is always important.

While this COULD be the beginning of a larger corrective process that will require further action, it is simply WAY to early to know for sure. As I laid out above, the actions of the market over the next week, or two, will determine our next major course of action.

For now, it remains but a “flesh wound.”

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Real Investment Advice is expressly disclaims all liability in ...

more