I use technical analysis in my investment decisions, and the chart that gets me most excited is the inverted head and shoulders, which analysts often describe as a head and shoulders bottom, a topic I mentioned in an earlier column.

The graphic illustrates just such a pattern. As you can see in the circles I’ve drawn, last summer the price of West Texas Intermediate oil fell to a trough and then rose. It then fell well below the former trough before rising again, forming a head. The price then fell again, but not so much.

In practice, this prefigures a sustained rise in the stock’s or commodity’s chart, and that’s where I’m putting my money – some of it, anyway. Oil prices are now likely to touch US$60 per barrel – a level they haven’t seen since the spring of last year – before they meet serious resistance.

A new bull market in oil, of course, will fuel a bull market in the shares of companies producing and selling the stuff. Don’t get too excited, though: This part of oil’s boom-and-bust cycle is likely to be modest, compared to the last one. Here’s why.

The background

Since oil became a serious business in the 19th century, petroleum busts have always followed petroleum booms, and vice versa. Indeed, in tough times people in the oil patch always trot out the old joke that “to make a small fortune in the oil industry, you have to begin with a large fortune.” A spectacular period of wealth creation, followed by wealth destruction, took place in 2007-8. You can see it on the left side of the chart below. It’s pretty obvious, but I nonetheless marked the period with a blue arrow. The red arrow on the right of the chartpoints to the current situation. I’ll conclude by zeroing in on that pattern.

Many factors led to this period of stock market turmoil. It began with the US subprime mortgage crisis, which produced a global collapse in interest rates. Investors sought higher yields than those offered by US Treasury bonds, briefly putting their money into oil, the price of which was going through the roof. By 2009, oil prices themselves had collapsed in response to a world-wide deterioration in economic activity. Then they rapidly began to rise.

In a presentation to the 2014 World Petroleum Congress, BP economist Christof Rühl explained that world oil prices had, in constant dollars, been extremely high for a number of years because of supply disruptions throughout the developing world ‘though especially in North Africa and the Middle East.

“Cumulative supply disruptions since the advent of the ‘Arab Spring’ from these countries have reached an extraordinary 3 million barrels per day,” he said. “We are now in a better position to return to the question of why oil prices were so stable,” despite “violent shifts” in production.

The main reason was the application of horizontal wells and underground fracturing to source rocks. The first impact of those technologies was to bring on enough oil supply to offset supply disruptions elsewhere in the world. Reflecting on the near-perfect balance between new supplies and supply disruptions, Rühl said “the match is sheer coincidence. Higher prices may induce more shale production. But virtually nothing else of logic or substance connects the two developments. And so markets will remain on edge – or eerily calm – until one side gains the upper hand.”

Who had the upper hand soon became clear. So effective was fracking in the United States in particular that, in December 2015, America lifted a 40-year-old oil export ban; producers and shippers responded quickly. By the first quarter of 2016, American exports totalled 416,000 barrels per day. The top customers included Canada – exempted from the ban on exports since 1985 – and Curaçao, where Venezuela’s national oil company, Petróleos de Venezuela, has a refinery. In the second quarter, total US exports rose to 547,000 barrels per day.

Growing demand was more than offset by growing supplies from outside OPEC. The world was awash with oil. Reluctantly, producers everywhere were hoarding record stockpiles. Petroleum reserves – by definition, the recoverable portion of resources available for use based on current knowledge technology and economics – have been on the rise for 20 years, world-wide. So effective have tight oil technologies been that, for the first time in more than 40 years, the United States is exporting oil again. And this happened just as all of the world’s oil-producing regions sought export markets.

In 2015 the world’s super-majors – BP (BP), Shell (RDS-A), Statoil (STO), TOTAL (TOT), Chevron (CVX), ExxonMobil (XOM) and ConocoPhillips (COP) – cut their capital expenditures by 27 per cent from 2013 levels. These dramatic reductions could mean that within a few years world oil supplies would struggle to keep pace with consumption, thus driving prices upward again. Did this mean the oil sands industry would soon regain the momentum it enjoyed at the beginning of the 21st Century? Maybe not.

Writing in the Harvard Business Review, economists Bernhard Hartmann and Saji Sam argued that “countries and companies should prepare for oil to hover around $50 per barrel for the foreseeable future. Historically this wouldn’t be shocking at all.” Using the 2014 US dollar as their baseline, they calculated that the average price of oil for since oil production began to develop as an important industry has been $35 per barrel. “In fact,” they said, the prices we now consider “low are actually near the real average price of a barrel of oil for the last 150 years.”

“What is surprising,” they continued, “is the fundamental shift we think is happening. The current low oil price environment is not an ‘oil bust’ that will be followed by an ‘oil boom’ in the near future. Instead, it looks as if we have entered a new normal of lower oil prices that will impact not just oil and gas producers but also every nation, company, and person depending on it.”

An International Energy Agency (IEA) report said “stockpiles of oil at a record three billion barrels are providing world markets with a degree of comfort” – unprecedented protection against geopolitical shocks and unexpected supply disruptions. This may have been comfortable for consumers, but for the petroleum producer those “comforting” inventories were disruptive.

That said, at this writing, global investment has dropped by 45 per cent since 2014. This was a disaster for the capital-intensive business that relies on steady development to keep supply available. Whatever grade of oil is in question – light oil, heavy or bitumen – equilibrium cannot occur until the price of the commodity equals the cost of bringing the last barrel consumed out of the ground. Supply cannot respond as fast as demand, so the two sides do not react to prevailing price signals in real time. The result has been “the mother of all market share battles,” ARC Energy’s Peter Tertzakian said. “Expect many years of ups and downs; steep price recoveries followed by destabilizing price wars that weaken prices.”

Recovery

Based on past performance, the conventional wisdom is that prices will rebound and prosperity will return to the sector, including the oil sands. Remember: after each bust comes a boom. Furthermore, according to that same wisdom, the rebound would lead to a boom which would again enable investors to make larger fortunes out of smaller ones. The crash of 2015-2016 was the worst in recent memory, however. Over a two-year period, Alberta’s economy would decline by some 6.5 per cent, compared to a 5.5 per cent decline during the Great Recession of 2008-2009, an analyst with the TD Bank said.

I beg to differ. At the beginning of this piece I included a 12-year chart of oil prices. Now, I would like to focus on the pattern that chart has shown during the last two years. It is a clear head-and-shoulders bottom with rising share volume – one of the most bullish patterns in the technician’s armory. Although at the moment there is a short-term sell signal on the far right of the PPO line, which I have circled, over the medium term there doesn’t seem to be resistance between oil’s present price and something approaching $60 per barrel.

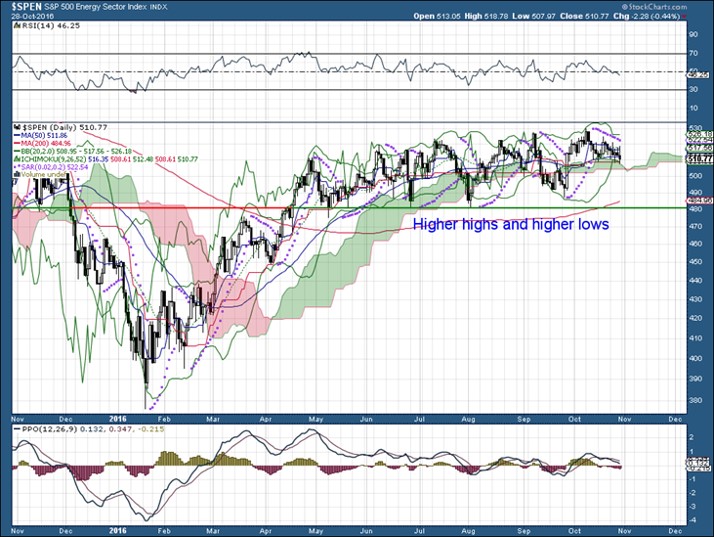

As confirmation of this idea, you will notice that the S&P Energy Index has been enjoying the bullish pattern of higher highs and higher lows since the awful oil price crash at the beginning of this year.

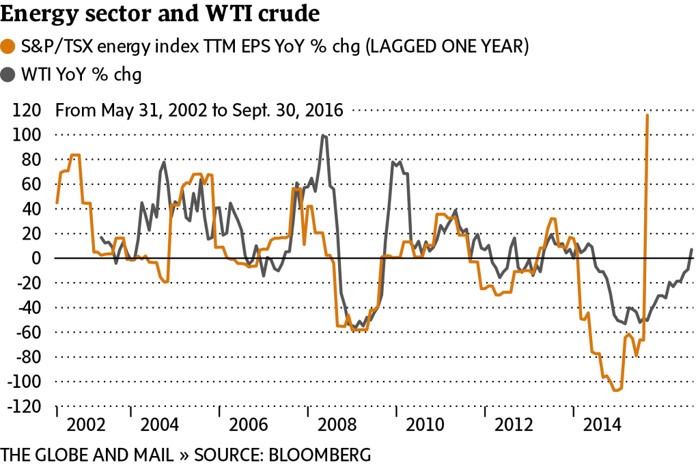

Now, this discussion brings me to a chart based on fundamental analysis, but it confirms the notion that a new bull market in oils has begun. The idea originated with Tobias Levkovich, who is chief U.S. equity strategist for Citi Investment Research.

“The grey line shows the year-over-year decline or appreciation in the oil price,” Globe and Mail market strategist Scott Barlow explains. “The orange line shows annual change in 12-month trailing earnings for the S&P/TSX energy sector – lagged for one year.” The fact that the lines track each other so closely shows that changes in crude prices effectively forecasted growth in the oil and gas sector – which, in itself, is not a surprise. After all, if the price of a commodity goes up, those who produce and sell the stuff are likely to make money.

The first mover

The last data point on the energy index line is “startling,” Barlow says dryly. The increase of about 116 per cent in profits by the members of the S&P/TSX energy index barely fits on the chart. “The increase is plotted at Sept. 30, 2015,” he says. Since the series is lagged one year to show the trend, though, “it’s actually year-over-year profit growth as of the end of September, 2016.”

The change is an incongruity caused by the small profit-per-share numbers for the 51-member index. Over the last 14 years, 12-month earnings per share for the index have been $130.67, on average. Compare this to the recent average of $9.93 per share, which is more than double the $4.60 earned in the 12 months a year ago. “Small dollar amount changes are causing huge swings in percentage growth.”

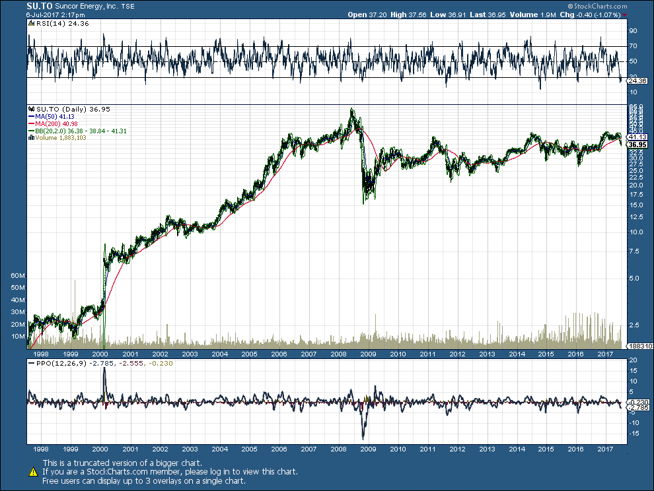

Continuing with the technical charts that have peppered this report, the first energy stock to make a move is likely to be Suncor (SU) – Canada’s largest integrated energy company, the fifth largest in North American and one of the largest private-sector energy enterprises in the world.

As the blue arrow indicates, at the end of October share prices broke out, reaching their highest levels in more than a year. The reasons? There were three: Oil prices were rising; the company had acquired majority ownership of Syncrude in the depths of the recession, and the company had implement important cost-cutting and streamlining operations during the oil-price collapse. In relative terms, therefore, its second-quarter financial results sparkled.

Comments

Log in or sign up to join the conversation.