S&P 500 Continues In Lévy Flight In Week 2 Of January 2018

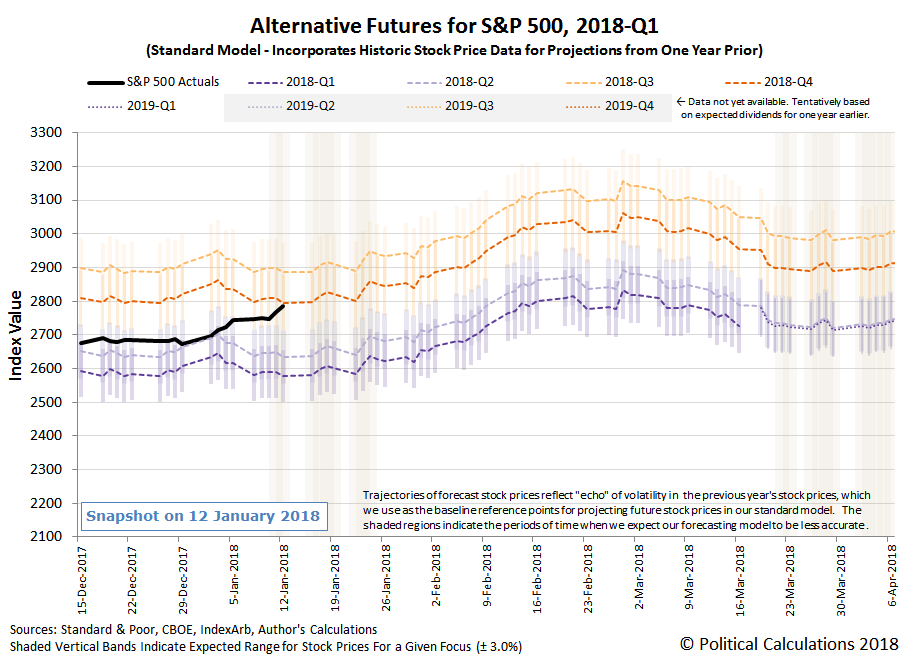

The S&P 500 continued its rapid rise in the second week of January 2018, having now risen some 112.63 points, or 4.2%, since the last day of trading in 2017, to close at a new record high value of 2,786.24 on Friday, 12 January 2018.

Although slower than in Week 1, the actual trajectory of the S&P 500 in Week 2 of January 2018 continues to be consistent with a Lévy flight, where investors are shifting their forward-looking focus from one point of time in the future to another.

We are observing an interesting development in that process. More often than not, when we see shifts in how far investors are looking into the future, we can typically tie the shifts to changing expectations for things like how and when the Fed will change its interest rate policies, which is why we pay close attention to the CME Group's Fedwatch tool, which provides an indication of the kind of odds that investors are giving for various changes in the Federal Funds Rate that investors are expecting at different points of time in the future. The following table summarizes those probabilities at several key future dates.

| Probabilities for Target Federal Funds Rate at Selected Upcoming Fed Meeting Dates (CME FedWatch on 12 January 2018) | ||||||

|---|---|---|---|---|---|---|

| FOMC Meeting Date | Current | |||||

| 125-150 bps | 150-175 bps | 175-200 bps | 200-225 bps | 225-250 bps | 250-275 bps | |

| 12-Mar-2018 (2018-Q1) | 26.3% | 72.6% | 1.1% | 0.0% | 0.0% | 0.0% |

| 13-Jun-2018 (2018-Q2) | 8.4% | 40.7% | 49.2% | 1.8% | 0.0% | 0.0% |

| 26-Sep-2018 (2018-Q3) | 3.6% | 22.0% | 43.0% | 28.2% | 3.0% | 0.1% |

| 19-Dec-2018 (2018-Q4) | 2.3% | 15.3% | 35.1% | 33.2% | 12.4% | 1.6% |

What this table shows is that investors are expecting two rate hikes in 2018. The first would be a quarter-point increase that they expect would be announced at the FOMC meeting scheduled for 21 March 2018, which has been expected for some time. The second would be another quarter-point increase that would take place at the FOMC meeting scheduled for 13 June 2018, which is a new development - prior to the second week of January 2018, investors had been anticipating that action would not take place until sometime during the third quarter of 2018.

So there would appear to be a disconnect between where our dividend futures-based model is indicating that investors are focusing their future-oriented attention and what the current expectations are for the future of the Fed's monetary policies. The current trajectory of the S&P 500 with respect to our model's projections suggests that investors are focusing more of their attention on the more distant future of either 2018-Q3 or 2018-Q4, which coincides with where stock prices are today, than they are on the nearer term future of either 2018-Q1 or 2018-Q2, where stock prices would be considerably lower if that were the case.

The question is why, and we suspect the answer may be the recently passed permanent reduction in the U.S. corporate income tax rates, which would primarily impact investor expectations for their investments in one of three ways:

- The corporate tax cuts make more money available to pay increased dividends to shareholders.

- The corporate tax cuts make more money available for U.S. firms to pursue new growth opportunities that can lead to faster than previously expected growth.

- The corporate tax cuts make more money available for share buybacks for U.S. firms without strong growth prospects, allowing them to artificially boost their dividends per share.

Many of these share price-boosting actions at different companies may be in addition to other changes, where the corporate tax cuts have also made more money available to pay higher wages and/or bonuses to their employees or to lower their prices to their consumers, which we've seen in the case of public utilities, but would also apply in the case of companies seeking greater market share.

As of 12 January 2018, we haven't seen any significant change in the expected levels of future dividends, but that may be about to change as we get into the earnings reporting season for 2018-Q1, where we've mainly been waiting for corporate boards to meet and set their new policies following the passage of the Tax Cuts and Jobs Act of 2017 back on 23 December 2017. The next six weeks have the potential to be a lot of fun!

As for the second week of 2018, here are the headlines that stood out.

Monday, 8 January 2018

- Oil mostly flat as rising U.S. output offsets OPEC worries

- Fed's Bostic says three rate hikes in 2018 may be too much

- Fed's Rosengren urges study of creating target range for inflation

- Fed's Williams says price-level targeting has benefits

- S&P keeps New Year's rally alive, Dow eases

Tuesday, 9 January 2018

- U.S. crude hits three-year high as prices climb in tight market

- U.S. oil output to surpass record earlier than expected: EIA

- Fed's Kashkari: Keep interest rates low to boost wages, inflation

- Wall Street climbs with boost from healthcare, banks

Wednesday, 10 January 2018

- Tax cuts mean Fed must be vigilant on 'overheating': Kaplan

- Fed's Evans wants rate hike pause, not concerned on yield curve

- Fed's Bullard says inflation miss has 'cost' U.S. lost growth

- U.S. yields at 10-month high on China report; S&P 500 snaps rally

- Wall Street falls on China, NAFTA concerns

Thursday, 11 January 2018

- Brent hits $70 per barrel before retreating; equities rise with energy

- Oil dips away from levels last seen in late 2014, but analysts say market supported

- Key Fed official slams U.S. tax cuts for imperiling economy - the "key Fed official" is the outgoing New York Fed president Bill Dudley, who made similar arguments against sustaining excessively high deficits during the Obama administration, but who never-the-less worked to fully enable them, including executing the expanded quantitative easing policies that offset the negative economic impact from the 2013 fiscal cliff tax hikes to avoid recession. Something of a case study for hypocrisy.

- Wall St. rises with oil prices, earnings optimism

Friday, 12 January 2018

- Oil adds to rally, heads for fourth week of gains

- U.S. holiday spending surges to 12-year high, helped by tax cuts

- Wall Street hits new highs on earnings optimism, data

Barry Ritholtz lists the positives and negatives for the U.S. economy and markets in Week 2 of January 2018, and if that weren't enough, also discovers a new investment strategy based on betting on companies slammed by President Trump that has been delivering outsized returns.

Disclaimer: Materials that are published by Political Calculations can provide visitors with free information and insights regarding the incentives created by the laws and policies described. ...

more