Significant Milestone For Monmouth Real Estate

A few days ago, I wrote about two Net Lease REITs that are seemingly trading at or below sound value: Lexington Realty (NYSE:LXP) and STAG Industrial (NYSE:STAG). I own both stocks, and I consider the durability of both REITs solid, based upon their past and future dividend growth prospects.

Dividend growth is something that I'm extremely interested in, especially in those REITs that can demonstrate that they can consistently generate steady and growing dividend income, while not sacrificing tenant or credit quality.

In today's rising interest rate environment, it's especially important to seek out investments that can not only generate robust dividend growth, but also maintain stable operating traits. The last thing we all need is another sucker yield REIT (like American Realty Capital Properties (NASDAQ:ARCP)).

One REIT that seems to get lost in the crowd is Monmouth Real Estate (NYSE:MNR). I have previously written on the company, and have come close to buying a few shares; however, I have never been able to pull the trigger YET. Today, I'm going to take another look to see if it may be time to jump onboard.

Let's Start With The Differentiators

At the end of the latest quarter, Monmouth's capital structure consisted of approximately $412 million in debt, of which $347 million was property-level fixed-rate mortgage debt, and $65 million were in loans payable. The company also has $111 million in perpetual preferred equity at quarter-end. Combined with an equity market capitalization of $655 million, Monmouth's total market capitalization was approximately $1.2 billion at quarter-end.

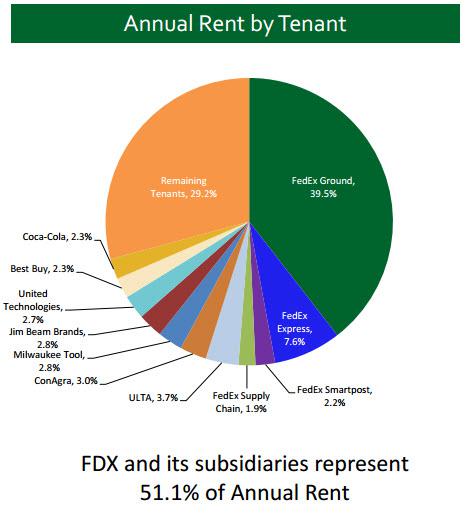

Monmouth is unique compared with other peers, based upon the composition of its portfolio - FedEX (NYSE:FDX) and its subsidiaries represent 51.1% of Monmouth's Annual Rent paid.

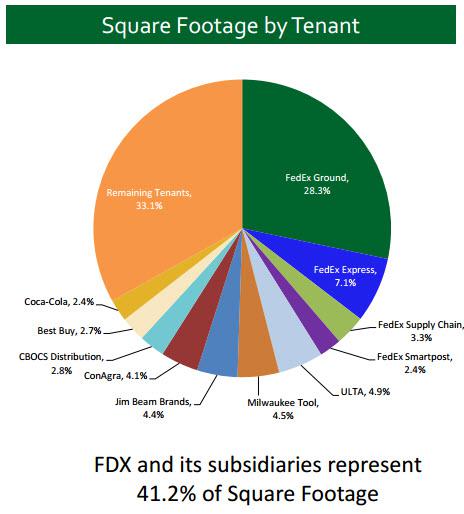

In addition, FDX and its subsidiaries represent 41.2% Monmouth's Square Footage:

Also, when you compare Monmouth's portfolio with the leading peers, you can see that the overall credit composition of its portfolio is the highest in the sector - around 79% of Monmouth's rental income is from investment-grade tenants or subsidiaries. The rental roster includes Anheuser-Busch Inbev (NYSE:BUD), Bunzl (OTCPK:BZLFY), Caterpillar (NYSE:CAT), Coca-Cola (NYSE:KO), Dr Pepper Snapple Group (NYSE:DPS), FedEx (FDX), International Paper (NYSE:IP), Jim Beam Brands, Keebler/Kellogg's (NYSE:K), National Oilwell (NYSE:NOV), ConAgra (NYSE:CAG), Sherwin Williams (NYSE:SHW), Siemens (OTCPK:SIEGY), Ulta (NASDAQ:ULTA), United Technologies (NYSE:UTX) and other high-quality companies.

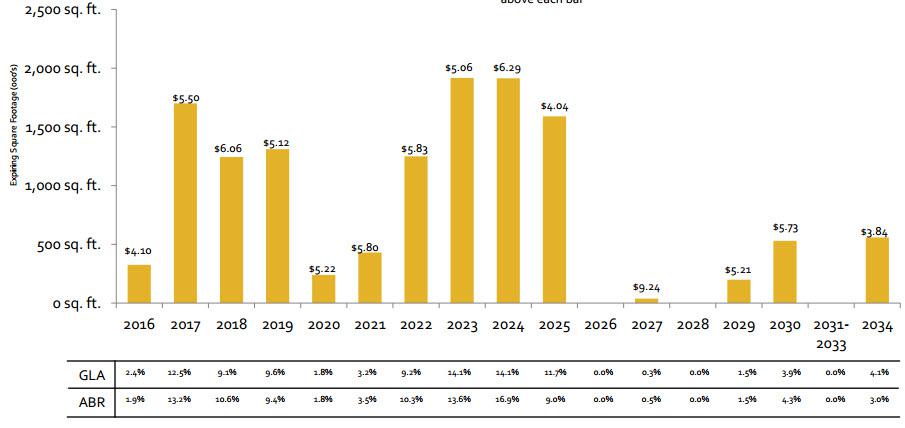

What Monmouth lacks in size, it makes up for in credit quality. It's also important to recognize that while the company does have high exposure to one tenant, the leases are well-laddered, meaning that the Fed-Ex leases are staggered. Here's a snapshot of the lease maturity schedule:

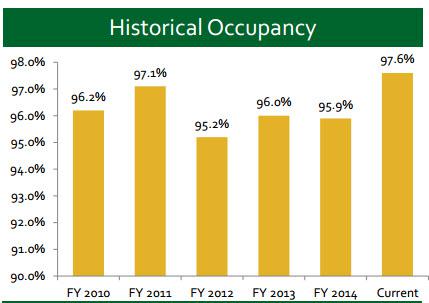

Not that Monmouth's non-rated tenants (around 15%) shouldn't infer that the tenants are speculative-grade, and as of the latest quarter, the company has the highest occupancy rate in the industrial REIT sector at 97.6%.

Here's how the occupancy compares with its peer group:

Monmouth's occupancy rate is up 120 bps over the prior quarter, and the weighted average lease maturity at quarter-end was 7.2 years, as compared to 6.8 years in the prior-year period. That brings me to another key differentiator for this REIT: Monmouth has the youngest weighted average building age in the Industrial REIT sector of 10.3 years.

The Balance Sheet

The company has consistently maintained conservative capitalization, with net debt-to-total market capitalization at 33%, net debt plus preferred equity-to-total market capitalization at 42%, fixed charge coverage at 2.3x and net debt-to-EBITDA at 6.3x.

From a liquidity standpoint, Monmouth ended the latest quarter with $25.5 million in cash and cash equivalents and around $20 million available from the accordion feature of the line of credit. In addition, it has around $52.5 million in marketable REIT securities, representing 5.4% of total undepreciated assets; at the end of the quarter, Monmouth had $1.3 million in unrealized gains on securities (around $100 million potential liquidity).

Continue reading this article here.

Brad Thomas is the Editor of the Forbes Real Estate Investor.

more