Overwriting Madness

Closed-end funds are an interesting sentiment indicator. Although there are individual factors that determine whether a specific closed-end fund trades at a premium or discount, there can be no arguing with the cold hard reality of what investors are willing to pay above (or below) NAV to gain exposure to a particular asset.

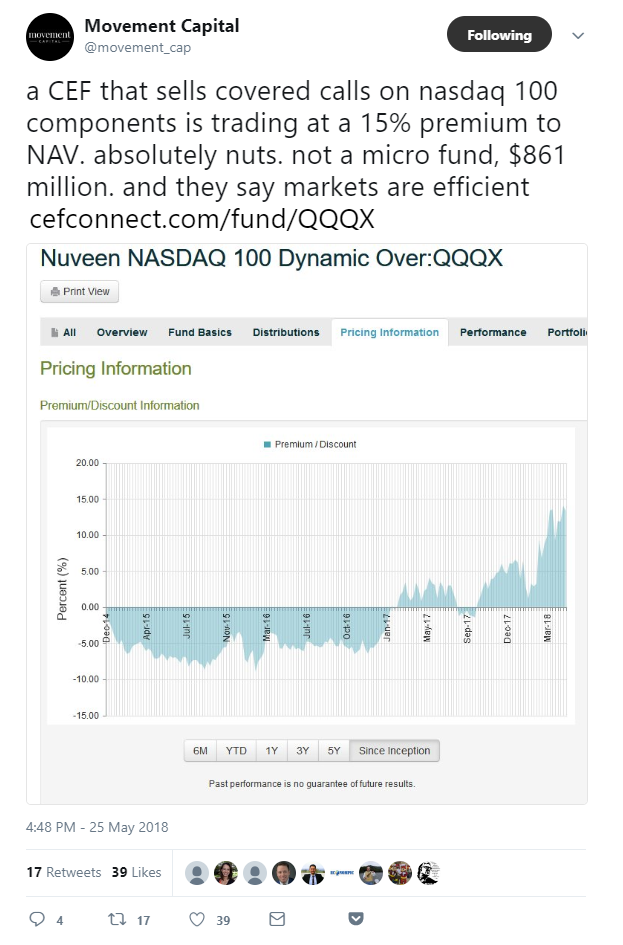

Therefore it was with great interest that I dug into the following tweet by my pal Adam Collins at Movement Capital (a must follow on twitter):

CEF stands for Closed-End Fund and the product in question is the Nuveen Nasdaq 100 Dynamic Overwrite Fund - symbol QQQX.

Adam is being facetious when he jests that “they say markets are efficient”. He knows - like we all do - that markets are far from efficient.

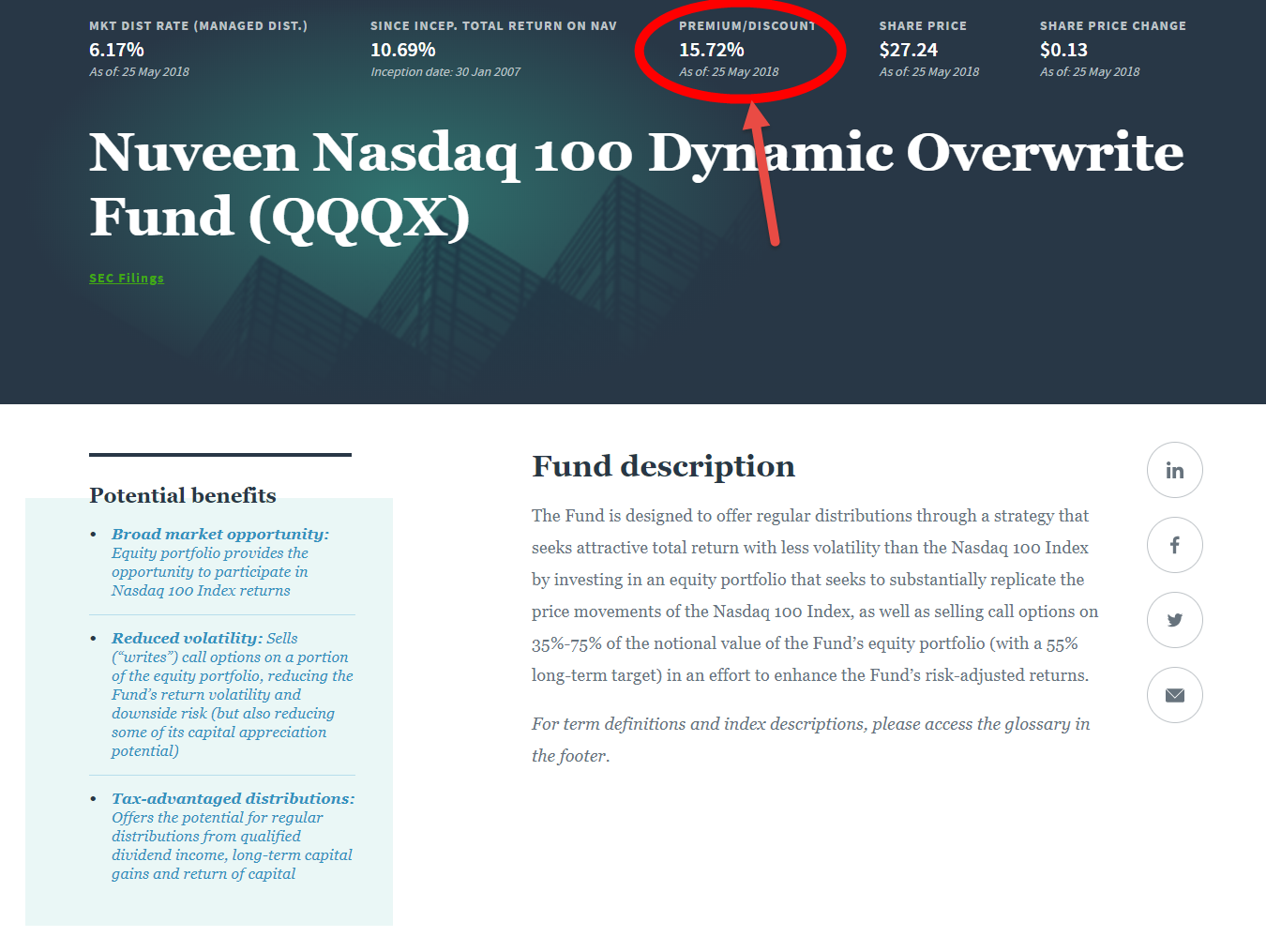

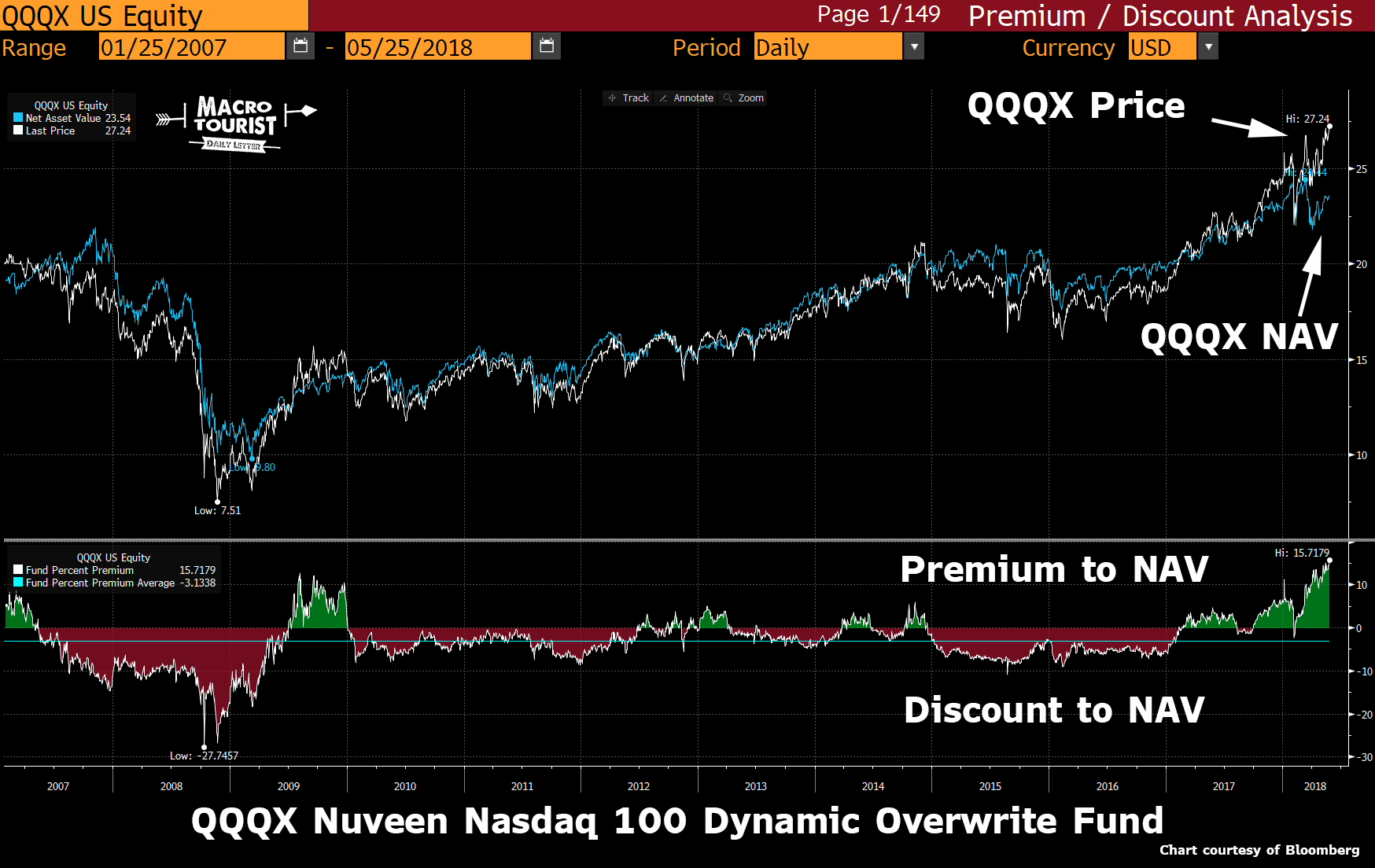

If markets were even remotely efficiently no one would pay at 15.72% premium to NAV (Net Asset Value) for a fund that buys QQQs and then shorts some calls against the position.

(Click on image to enlarge)

The return stream could be easily replicated with a little work. There is no need to pay an extra 15% of your principal for the privilege of another money manager executing this strategy.

Think about the absurdity of investors driving the fees on ETFs down to single digit basis points, but then paying almost 1600 basis points over the intrinsic value of this closed-end fund. The outperformance from this manager would have to be spectacular to justify this sort of premium.

I have nothing against Nuveen’s product. They figured out what investors wanted and delivered. Good for them. Free markets for free people.

But let’s use this to our advantage to examine the signals this popularity is sending.

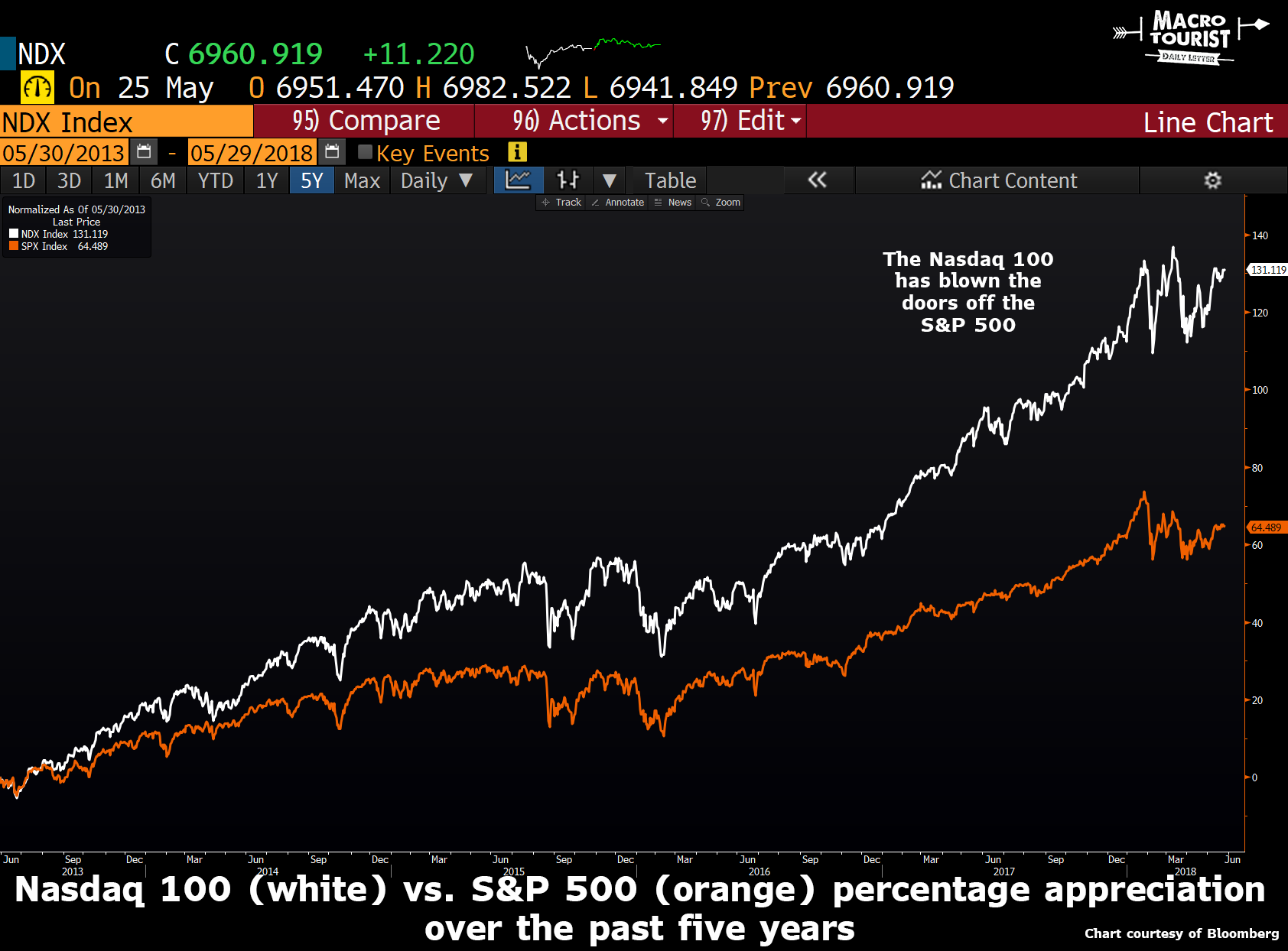

First of all, the base index is the Nasdaq 100. We might as well rename this the FAANG index. Apple (12%), Amazon (9.8%), Google (8.7%), Facebook (5.5%) and Netflix (1.9%) represent almost 40% of the index. And the Nasdaq 100 has more than doubled the S&P 500 price appreciation over the past five years.

(Click on image to enlarge)

Investors are definitely chasing the hot stocks.

But then instead of just buying the Nasdaq 100, the Nuveen QQQX fund is writing call options on the position - hence the name “Nuveen Nasdaq 100 Dynamic Overwrite Fund”. Yet what does this call selling mean? Well, once again it’s a bet on short volatility. This strategy does well when the implied volatility of the options that are shorted ends up being less than the realized volatility over the life of the options. It’s not quite that simple, but at its heart, this is a short vol strategy.

Let’s put it together. This closed-end fund invests in FAANG-type stocks and then shorts volatility against it. Yup, nothing to worry about there.

And not only that, for the privilege of chasing two of the hottest trends, you pay a premium.

(Click on image to enlarge)

We have seen this story play out time and time again. Investors chase returns and invest in the best performing asset at the worst possible time.

I am not short QQQX, but when it comes time to hit some bids in the FAANG stocks, I will give this closed-end fund serious consideration. I like trades where there is extra juice built into the position. And 15% extra premium for buying some QQQs and shorting some call options against it? Sold to them.

But then again, I believe markets are inefficient and there exist edges that an investor can exploit. What? I know - that’s crazy talk. Don’t look now, but I think there is a $100 bill lying in front of us.

Disclosure: None.