NRG Energy Is A Free Roll On Natural Gas Prices

10 Year Lows

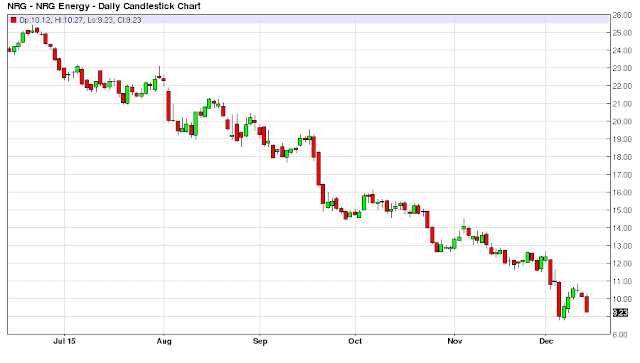

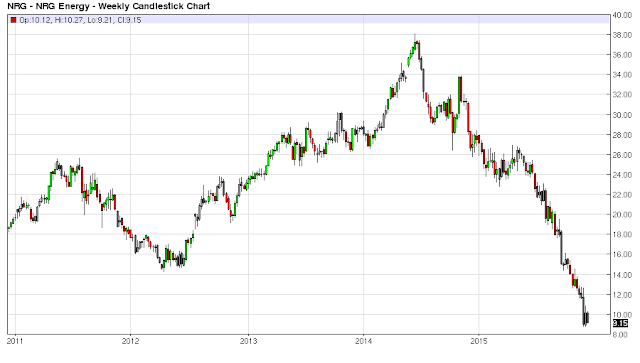

The Stock price is at a 10 year low, a myriad of factors have come together over the past 6 months to push the stock down from $25 a share on June 22nd to as low as $8.81 on December 4th 2015. The previous 10 year low in the stock was $15.32 on April 30, 2012 on similarly low natural gas prices for the spot market where natural gas dipped below $2 per MMBtu. Thus a low natural gas environment is nothing new for NRG, and Natural Gas prices recovered on declining rig counts and colder weather as did NRG`s stock moving from the 2012 low of $15.32 towards $37.20 a share as recently as May 31, 2014.

Negative Catalysts

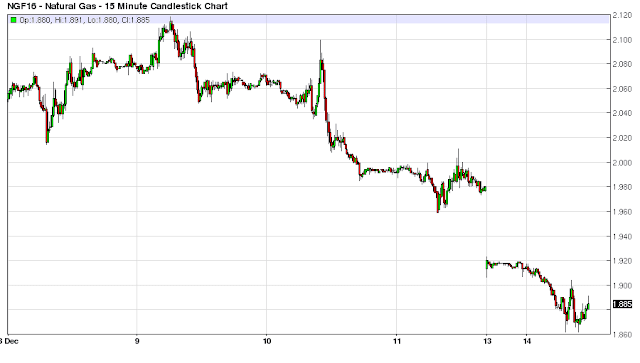

The catalysts for the recent plunge in the stock are many fold. First the utilities sector is weaker as investors anticipate a 25 basis point rate hike by the Federal Reserve. Second the Power Generation Firms like Calpine (CPN), Dynegy (DYN) and NRG (NRG) are all getting hit on lower priced electricity at the wholesale level due to a mild winter so far, and a downward trek in Natural Gas prices moving from $3.30 MMBtu on August 13, 2015 to $2.12 MMBtu on December 7, 2015. NRG has company specific headwinds in a failed and costly excursion into Green Businesses with the likes of Home Solar, Renew: Solar/Wind, and EVgo. And the sudden resignation of David Crane who has been the face of the company for over a decade. Add to this over $20 Billion in debt, a dismal 2015 for earnings, around an 8% short interest in the float and technical algo selling on new lows and you end up with an $8 stock.

Are these catalysts reversible?

The utilities sector and bond prices could continue to take a hit in 2016 if inflation takes off and the Fed is forced into playing catchup with several rate hikes in the span of the next 6 months. However, given the tepid global growth environment and other central banks` dovishness this scenario seems less likely. It is looking like a “One and Done” rate hike for the next 6 months by the Federal Reserve. Money should not retreat from the utilities sector in 2016 due to extensive rate hikes. At any rate, this catalyst shouldn`t be the defining reason for investing in NRG one way or the other.

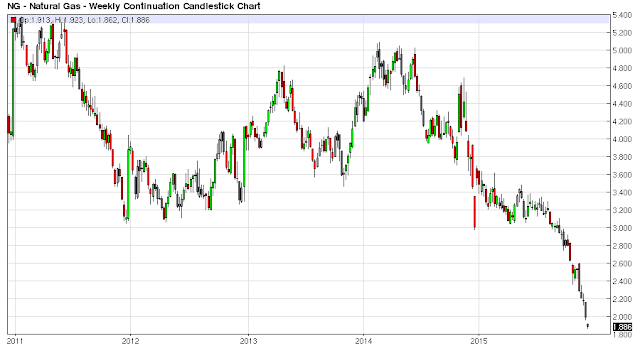

Low Natural Gas Prices

In regard to the Power Generation Firms trading down on low natural gas prices, if this correlation continues, this actually serves as a positive catalyst with natural gas prices close to where they bottomed in 2012. We are heading into the heart of the winter heating season in February where natural gas prices tend to rise, this bodes well for Electricity pricing at the wholesale level. At any rate, natural gas prices trend, and given enough natural gas rigs going offline, natural gas prices will recover to the $5 MMBtu level. Sure there is a lot of natural gas in storage, but there was a lot in storage in 2012 as well, rigs were idled, weather patterns changed and natural gas prices moved well above $7 MMBtu on cold weather two years ago. It is just a matter of time but natural gas prices will make a long sustained trend higher towards the $5 MMBtu level sometime over the next two years. It is just how the market trades, but even if it is different this time, I anticipate a rebound in natural gas prices this winter to around the $3 MMBtu area which should serve as a positive catalyst for a rebound in NRG and the rest of the Power Generation Firms.

Going Green is Costly

NRG`s attempt to revolutionize the electricity market with its Green initiatives like Home Solar, Renew: Solar/Wind, and EVgo is already being reversed out as the market has voted and this is what got David Crane fired. He understood this fact, but it was too little too late. Somebody had to pay for destroying shareholder value in 2015. NRG is trying to spin these Green assets out in a joint venture type of structure, but basically these assets are for sale, and have already been given a $125 Million runway to either start making money or fail altogether for 2016.

This change is not being reflected in the stock price, for example, Home Solar alone had a $50 million budget for 2015 and David Crane`s ego let that balloon to a $175 million loss for full year 2015, this is why the board forced him out. This $125 million runway is the aggregate exposure for these Green businesses for 2016 and beyond. The company is changing its strategy and focusing on running a much better P/L with its existing core business of solid Power Generation Assets and a highly successful retail arm in Reliant Energy, and ditching the earning`s drag of the Green Businesses. They haven`t announced a job cuts number for morale reasons, but make no mistake behind the scenes they are reassigning personnel, and embarking on a substantial cost cutting program across the various business units. There is enough fat that can be cut to make a difference going forward in 2016 in speaking with insiders at the company. In short, the company gets it and they are going to be much more fiscally responsible for 2016, and these changes will eventually find their way to the quarterly earning`s reports next year. This strategy change should be a positive catalyst for a rebound in the stock for 2016.

David Crane Resignation

With regard to the resignation of David Crane, he was the face of the company and he had grand visions for the future of the electricity market. However, just like Enron with broadband ambitions he was ahead of his time, and the execution just wasn`t good enough, given the other headwinds the company faced in a low natural gas environment. Mauricio Gutierrez has been with the company since 2004 in various roles and he understands the core business. It is obvious that the board understand the market mandate as well: get back to the basics, focus on the businesses that bring in cash flow, get rid of the Green initiatives that eat into corporate profits, cut costs across the board, and improve earning`s results for full year 2016. In short, David Crane`s enormous ego had NRG writing checks that albeit in part laudable, just didn`t make for good operational business sense. The board felt that his presence was always going to be too big at the company to fully recognize underlying value in getting back to the basics of a much leaner, less transformative, but better run company from a profitability standpoint. His resignation is a positive catalyst going forward given what NRG`s new mandate is for 2016, running the business focusing strictly on a P/L standpoint.

Debt Concerns

The $20 Billion in debt is a concern, but the debt has always been there as NRG has a collection of great assets acquired through this debt financing. The concern was the fiscal approach by the company, they needed to be throwing off much more cash flow towards paying down some of this debt, as opposed to incurring further expenses trying to transform into a Green Next Generation Technology company. Now that the market has spoken, the market is going to reward NRG for paying down some of this debt due to cutting costs, and improving the profitability of the company. Although it is currently a lower Wholesale Power Rate Environment due to lower natural gas prices, the core business generates solid cash flows; more than enough to start paying off some of this debt, now that costs are being addressed at the company. Moreover, the board has gotten the message to start focusing on being more fiscally responsible with these existing cash flows. In short, NRG is in no danger of going bankrupt or having solvency issues in the foreseeable future. The company had this much debt 6 months ago when it was a $25 stock. The debt issue isn`t prohibitive from NRG recovering as a stock to the $22 a share range.

Earning`s Recovery

2015 was a dismal year for earnings, but this is reversible given a focus on the bottom line, and executing on the cost cutting initiatives spread out throughout the company. NRG will have better year over year comps in 2016, and if natural gas prices rebound a little this should help on the earning`s front. The big boost to earnings will be getting out from under the “GreenCo” assets that were a real drag on corporate profits, not to mention a major distraction from focusing on maximizing earnings for shareholders.

Short Interest

With a substantial short position in the stock, all these shares will have to cover at some point guaranteeing future buyers in the stock. NRG is not going bankrupt, they generate too much cash flows for that. There is no cure for low natural gas prices like low natural gas prices. Sure conceivably the stock could go lower, but I wouldn`t press a short here as one could wake up to a buyout of NRG at $18 a share on a sleepy Monday morning. I would prefer to be on the other side of this short squeeze.

Technical Selling

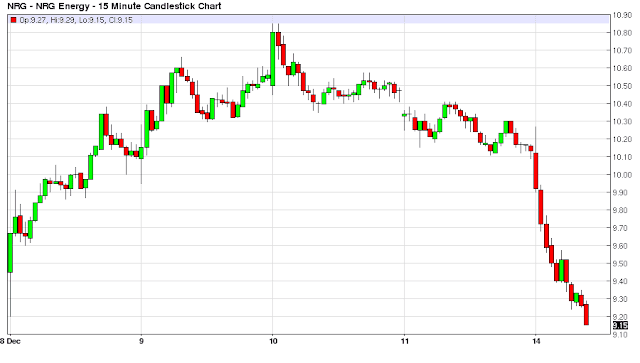

The technical selling often leads to overshooting on the downside, especially when key technical levels are breached towards year end. There was 4 times normal trading volume on Friday and a retest of the $8.80 level at the open on Monday on a risk off day in the overall markets. Buyers stepped in with support at this level and found value here. There should be substantial upside technical buying yet to go sometime in 2016, as shorts begin to cover positions, and new longs initiate positions as the cost cutting measures play out on the bottom line in 2016.

Forecast

I have followed this company`s stock for 10 years, and Friday as I watched it getting clobbered to the tune of nearly 20% I felt that the selling was overdone. This stock has moved around a lot over the last 7 years but it usually finds its way back to the $18-$22 a share range. This has not been a good year for the company. But none of the catalysts for the stock being so low now are permanent in nature, and overly cumbersome to overcome.

Oftentimes the stock moves before the underlying fundamentals, but in NRG`s case the Fundamentals are already changing for the better in the form of a change in strategic operational structure, this change has yet to be reflected in the current stock price. Alternatively, if investors view this strategic change as a negative then their analysis is incorrect. The strategic change will definitely unlock shareholder value in the future of this beaten down name. Furthermore, if NRG is strictly tracking spot natural gas prices, which given the operational strategy mistakes at the company I seriously doubt, the shares will recover along with natural gas prices just like 2012. Economics will play out in the natural gas market, because there is no OPEC inspired price war playing out in natural gas like there is in the oil market. A drop in Natural Gas and Oil Rigs which as a byproduct bring some natural gas to market will eventually lead to natural gas inventories being reduced. Natural Gas prices will move to the upside long before inventories rebalance as traders anticipate the effects of the idled rigs on future supply. It is just a matter of time before economics play out in the natural gas market, natural gas prices will eventually rise. We haven’t even gotten to the winter heating season yet. For example, last year natural gas prices rose from December 22nd 2014 to February 23, 2015 on colder weather.

However, let us assume that natural gas prices just hover around this $2 MMBtu level. The question for investors here is how much of this natural gas price is being currently reflected in NRG`s stock price? And are any changes to corporate strategy currently being priced into the stock? My assessment is that investors have the opportunity to initiate a position in the stock because of the negative sentiment regarding these two issues. This is why the opportunity exists in the first place.

This negative sentiment regarding these two issues is likely to change over time. It is my contention that the change in corporate strategy is able to mitigate the negative effects of low natural gas prices for 2016. Even with no rebound in natural gas prices for 2016, the positive changes in corporate strategy for 2016, should lead to positive operational growth profits year over year. In effect an investor is free rolling the eventual turnaround in natural gas prices over the next two years.

In conclusion, NRG Energy represents real value at these levels, and anything in the $8 area denotes an exceptional long term investment opportunity. I expect the stock to trade back in the $16 area sometime over the next 6 months. And if management really executes on the cost cutting measures, now that the company is no longer bogged down with green ambitions, this stock can reasonably move up to the $22 a share level sometime in 2016. Anything above $22 a share is just gravy given this entry point, but definitely a possibility.

Disclaimer: All of the content on EconMatters is provided without assurance or warranty of any kind. The opinions expressed here are personal views only, and ...

more