Morning Call For Wednesday, Jan. 11

OVERNIGHT MARKETS AND NEWS

Mar E-mini S&Ps (ESH17 -0.03%) are little changed, up +0.03%, and European stocks recovered from a 1-week low and are up +0.10%. Equity markets are marking time ahead of President-elect Trump's first press conference since his election. That press conference is scheduled for later today and may provide clues on his promises to boost the economy. Strength in energy producing stocks is limiting declines in U.S. markets and boosting European bourses with Feb WTI crude oil (CLG17 +0.39%) up +0.59%. Crude has support on the outlook for tighter supplies after Saudi Arabia was said to cut Feb crude sales to China and southern Asian nations as it curbs supply as part of its planned production cuts. Mining stocks and raw-material producers are higher as well with Feb COMEX gold GCG17 +0.22%) up +0.37% at a 6-week high. Gold has pushed higher on increased safe-haven demand due to the uncertainty regarding President-elect Trump's policies. Asian stocks settled mixed: Japan +0.33%, Hong Kong +0.84%, China -0.79%, Taiwan -0.04%, Australia +0.19%, Singapore -0.17%, South Korea +1.68%, India +0.90%.

The dollar index (DXY00 +0.43%) is up +0.31%. EUR/USD (^EURUSD) is down -0.37%. USD/JPY (^USDJPY) is up +0.44%.

Mar 10-year T-note prices (ZNH17 +0.03%) are down -0.5 of a tick.

UK Nov manufacturing production rose +1.3% m/m, stronger than expectations of +0.5% m/m and the biggest increase in 7 months.

UK Nov industrial production rose +2.1% m/m, stronger than expectations of +1.0% m/m and the largest increase in 7 months.

U.S. STOCK PREVIEW

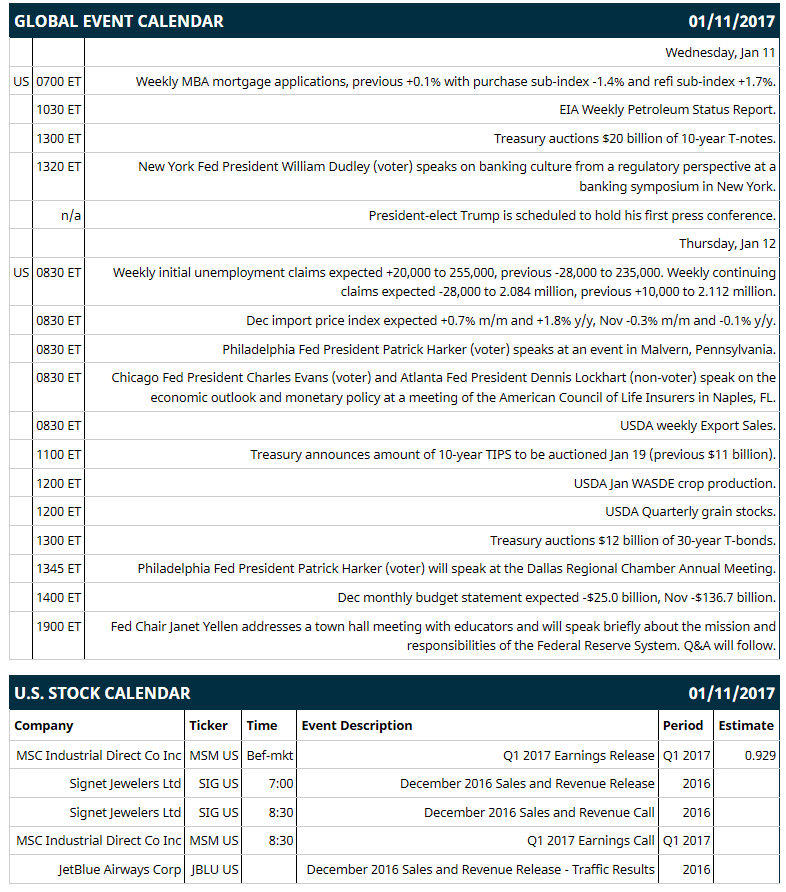

Key U.S. news today includes: (1) weekly MBA mortgage applications (previous +0.1% with purchase sub-index -1.4% and refi sub-index +1.7%), (2) Treasury auctions $20 billion of 10-year T-notes, (3) New York Fed President William Dudley (voter) speaks on banking culture from a regulatory perspective at a banking symposium in New York, (4) President-elect Trump is scheduled to hold his first press conference, (5) EIA Weekly Petroleum Status Report.

Russell 1000 earnings reports today include: MSC Industrial Direct (consensus $0.93).

U.S. IPO's scheduled to price today: none.

Equity conferences this week include: J.P. Morgan Healthcare Conference on Mon-Thu, Deutsche Bank Global Auto Industry Conference on Tue-Wed, Needham & Company Growth Conference on Tue-Wed, ICR Conference on Tue-Wed, Evercore ISI Utility Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

JPMorgan Chase (JPM +0.29%) was rated a new 'Buy' at UBS with a price target of $98.

salesforce.com (CRM +0.03%) and Microsoft (MSFT -0.03%) were both rated 'Outperform' at Wells Fargo Securities.

Juniper Networks (JNPR +0.04%) fell over 2% in pre-market trading after the stock was downgraded to 'Sell' from 'Hold' at Deutsche Bank.

Citigroup (C +0.02%) was rated a new 'Sell' at UB with a price target of $58.

Torchmark (TMK +0.14%) was downgraded to 'Sell' from 'Hold' at Evercore ISI with a 12-month target price of $70.

United Continental Holdings (UAL +3.34%) climbed almost 3% in after-hours trading after it reported its December load factor improved 10 bps to 83.1% and that revenue passenger miles in December rose +2.6%.

Merck (MRK -1.93%) rose 4% in after-hours trading after the U.S. FDA granted priority review for its supplemental Biologics License Application (sBLA) for Keytruda, plus chemotherapy, as primary treatment of patients with advanced lung cancer.

Achaogen (AKAO +3.14%) rallied 7% in after-hours trading after Baker Brothers raised their passive stake in the company from less than 1% to 13.1%.

Parsley Energy (PE +2.54%) fell 4% in after-hours trading after it announced a public offering of 20 million shares of Class A common stock.

MagnaChip Semiconductor (MX +4.10%) gained almost 1% in after-hours trading after it reported Q4 preliminary revenue of $180 million, higher than consensus of $177 million.

Ichor Holdings Ltd (ICHR -4.29%) jumped 8% in after-hours trading after it reported Q4 preliminary sales of $131 million, above consensus of $118 million.

Veeco Instruments (VECO +1.89%) slid 3% in after-hours trading after it announced a public offering of $200 million convertible senior notes due 2023.

Bluerock Residential Growth REIT (BRG -0.07%) dropped 4% in after-hours trading after it announced a public offering of 4 million shares of Class A common stock.

MARKET COMMENTS

Mar E-mini S&Ps (ESH17 -0.03%) this morning are up +0.75 of a point (+0.03%). Tuesday's closes: S&P 500 unch, Dow Jones -0.16%, Nasdaq +0.20%. The S&P 500 on Tuesday closed little changed. Stocks were boosted by the unexpected +71,000 increase in U.S. Nov JOLTS job openings to 5.522 million, stronger than expectations of -34,000 to 5.500 million. In addition, mining stocks rallied after the price of copper climbed +2.92% to a 3-week high and the price of gold rose to a 5-week high. Energy producer stocks fell as crude oil prices fell to a 3-week low.

Mar 10-year T-notes (ZNH17 +0.03%) this morning are down -0.5 of a tick. Tuesday's closes: TYH7 -0.50, FVH7 unch. Mar 10-year T-notes on Tuesday closed slightly lower. T-note prices were undercut by the stronger-than-expected U.S. Nov JOLTS job openings report and by supply pressures as the Treasury auctions $56 billion in coupons this week. T-notes found support as Feb crude and gasoline prices fell to 3-week lows, which undercut inflation expectations.

The dollar index (DXY00 +0.43%) this morning is up +0.32 (+0.31%). EUR/USD (^EURUSD) is down -0.0039 (-0.37%). USD/JPY (^USDJPY) is up +0.51 (+0.44%). Tuesday's closes: Dollar index +0.080 (+0.08%), EUR/USD -0.0020 (-0.19%), USD/JPY -0.26 (-0.22%). The dollar index on Tuesday closed slightly higher. The dollar found support on the bigger-than-expected increase in U.S. Nov JOLTS job openings report, which was a sign of economic strength.

Feb WTI crude oil prices (CLG17 +0.39%) this morning are up +30 cents (+0.59%) and Feb gasoline (RBG17 +1.25%) is +0.0239 (+1.55%). Tuesday's closes: Feb crude -1.18 (-2.27%), Feb gasoline -0.0166 (-1.06%). Feb crude oil and gasoline on Tuesday fell to 3-week lows and closed lower on the slightly stronger dollar and on concerns about Iraqi production-cut compliance after news that Iraqi Dec crude exports rose +3% m/m to a record 3.51 million bpd.

(Click on image to enlarge)

Disclosure: None.