Morning Call For Thursday, Oct. 19

OVERNIGHT MARKETS AND NEWS

Dec E-mini S&Ps (ESZ17 -0.44%) this morning are down -0.51% at a 1-week low and European stocks are down -0.80% at a 2-week low as rising tensions between Spain and Catalonia spurs liquidation in equities and pushed the VIX volatility index up to a 5-week high. In a response to a Thursday deadline set by Spain for the state of Catalonia to renounce its claims to independence, Catalan President Puigdemont said his state may declare independence from Spain unless the government in Madrid agrees to talks. Spanish Prime Minster Rajoy said the Spanish government will start the process of taking direct control of the Catalan regional administration under Article 155 of Spain's Constitution unless the Catalan government steps back from its push for independence. A slide in Apple suppliers is also weighing on technology stocks after the Taipei-based Economic Daily reported that Apple has cut orders linked to its iPhone 8 models by as much as 50% over the rest of the year due to lukewarm reception for its newest model. Asian stocks settled mixed: Japan +0.40%, Hong Kong -1.92%, China -0.34%, Taiwan +0.37%, Australia +0.10%, Singapore +0.18%, South Korea -0.59%, India closed for holiday. China's Shanghai Composite fell to a 1-week low on disappointment that a 3-hour speech by Chinese President Xi Jinping at China's 19th Communist Party Congress failed to provide details to support the market. The rally in Japanese stocks continues as the Nikkei Stock Index rose to a 21-year year ahead of Sunday's elections in Japan where Prime Minister Abe's party is expected to win in a landslide.

The dollar index (DXY00 -0.16%) is down -0.16%. EUR/USD (^EURUSD) is up +0.32%. USD/JPY (^USDJPY) is down -0.43%.

Dec 10-year T-note prices (ZNZ17 +0.16%) are up +7 ticks.

The Japan Sep trade balance widened to a surplus of +670.2 billion yen. larger than expectations of +556.8 billion yen. Sep exports rise +14.1% y/y, weaker than expectations of +15.0% y/y. Sep imports rose +12.0% y/y, weaker than expectations of +14.7% y/y.

China Q3 GDP rose +6.8% y/y, right on expectations.

China Sep industrial production rose +6.6% y/y, stronger than expectations of +6.5% y/y.

U.S. STOCK PREVIEW

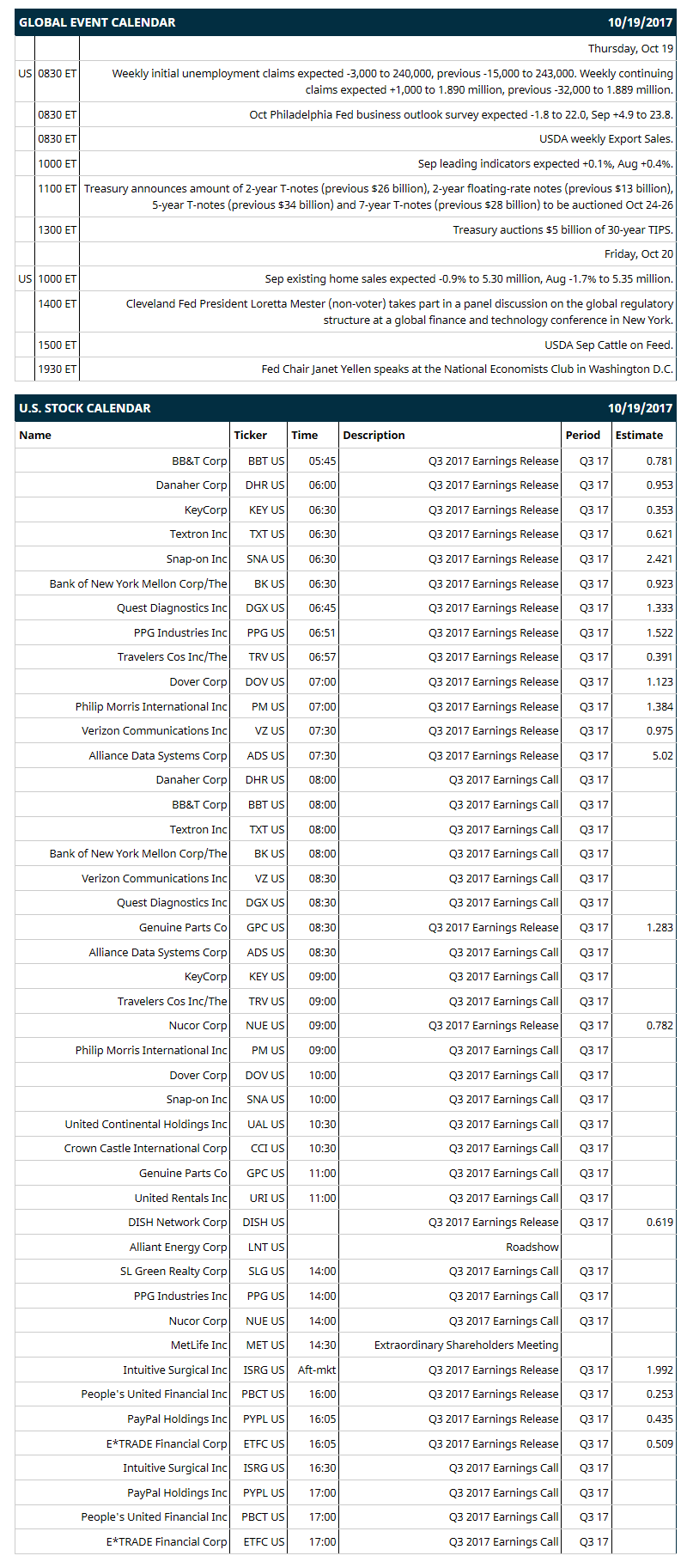

Key U.S. news today includes: (1) weekly initial unemployment claims (expected -3,000 to 240,000, previous -15,000 to 243,000) and continuing claims (expected +1,000 to 1.890 million, previous -32,000 to 1.889 million), (2) Oct Philadelphia Fed business outlook survey (expected -1.8 to 22.0, Sep +4.9 to 23.8), (3) Sep leading indicators (expected +0.1%, Aug +0.4%), (4) Treasury auctions $5 billion of 30-year TIPS, and (5) USDA weekly Export Sales.

Notable S&P 500 earnings reports today include: PayPal (consensus $0.44), PPG (1.52), Quest Diagnostics (1.33), Genuine Parts (1.28), Verizon (0.98), Danaher (0.95), Bank of New York Mellon (0.92), Nucor (0.78), Textron (0.62), Dish Network (0.62), ETrade (0.51), Travelers (0.39), KeyCorp (0.35), People's United Financial (0.25).

U.S. IPO's scheduled to price today: Sea Ltd (SE), Mosaic Acquisition (MOSC/U), RISE Education Cayman (REDU).

Equity conferences this week: BIO Investor Forum on Tue, METALCON Conference on Thu, SAP Retail Executive Forum on Thu, American Association for the Study of Liver Diseases Liver Meeting on Fri.

OVERNIGHT U.S. STOCK MOVERS

Nike (NKE +0.58%) was downgraded to 'Neutral' from 'Buy' at Goldman Sachs.

Grainger (GWW +1.65%) may open lower this morning after it was downgraded to 'Sell' from 'Neutral' at UBS with a price target of $195.

Jazz Pharmaceuticals Plc (JAZZ -0.03%) was initiated at a 'Buy' at FBR Capital Markets with a 12-month target price of $206.

Sprint (S -0.56%) was downgraded to 'Neutral' from 'Outperform' at Macquarie.

Adobe Systems (ADBE +1.74%) jumped 8% in after-hours trading after it said it sees fiscal 2018 adjusted EPS of $5.50, better than consensus of $5.20.

eBay (EBAY +1.28%) slid 5% in after-hours trading after it said it sees Q4 adjusted EPS from continuing operations of 57 cents-59 cents, weaker than consensus of 60 cents.

Pattern Energy (PEGI unch) slid 4% in after-hours trading after it said it expects its Q3 operating loss to be materially and substantially greater than a year ago due to hurricanes this fall.

Supernus Pharmaceuticals (SUPN +0.49%) was initiated at a 'Buy' at FBR Capital Markets with a 12-month target price of $53.

Ignyta (RXDX +13.24%) fell nearly 4% in after-hours trading after it announced that it had commenced an underwritten public offering of $125 million is shares of its common stock.

Limelight Networks (LLNW +2.75%) rallied 10% in after-hours trading after it raised its 2017 revenue estimate to $182 million-$185 million from a July 26 estimate of $180 million-$182 million.

Earthstone Energy (ESTE -1.40%) dropped over 7% in after-hours trading after it announced that it had commenced an underwritten public offering of 4.5 million shares of its Class A common stock.

Evoke Pharma (EVOK -3.68%) was initiated at a 'Buy' at FBR Capital Markets with a 12-month target price of $10.

Conatus Pharmaceuticals (CNAT +0.98%) jumped almost 7% in after-hours trading after it said the European Medicines Agency granted orphan designation to CNAT's drug candidate IDN-7314 for the treatment of primary sclerosing cholangitis.

MARKET COMMENTS

Dec S&P 500 E-mini stock futures (ESZ17 -0.44%) this morning are down -13.00 points (-0.51%) at a 1-week low. Wednesday's closes: S&P 500 +0.07%, Dow Jones +0.70%, Nasdaq -0.13%. The S&P 500 on Wednesday rose to a new record high and settled higher on a rally in technology stocks led by an 8% jump in shares of IBM after it reported stronger-than-expected Q3 EPS. Stocks were also boosted by the Fed Beige Book saying that U.S. economic activity from Sep through Oct 6 increased even amid "major disruptions" across the South from hurricanes. Stocks were undercut by weakness in housing stocks after U.S. Sep housing starts fell -4.7% to 1.127 million, weaker than expectations of -0.4% to 1.175 million and a 1-year low.

Dec 10-year T-note prices (ZNZ17 +0.16%) this morning are up +7 ticks. Wednesday's closes: TYZ7 -9.50, FVZ7 -4.25. Dec 10-year T-notes on Wednesday fell to a 1-week low and closed lower on comments from New York Fed President Dudley who said the Fed is on path to deliver three Fed rate hikes this year as forecast, which implies a third rate hike in December.

The dollar index (DXY00 -0.16%) this morning is down -0.149 (-0.16%). EUR/USD (^EURUSD) is up +0.0038 (+0.32%) and USD/JPY (^USDJPY) is down -0.48 (-0.43%). Wednesday's closes: Dollar Index -0.123 (-0.13%), EUR/USD +0.0021 (+0.18%), USD/JPY +0.74 (+0.66%). The dollar index on Wednesday fell back from a 1-week high and closed lower on the weaker-than-expected U.S. Sep housing starts and building permits report. In addition, EUR/USD rebounded from a 1-week low on hopes for some resolution of the independence movement in Catalonia ahead of Thursday's deadline for a response from Catalonia's president on whether or not the region has declared independence.

Nov crude oil (CLX17 -1.25%) this morning is down -61 cents (-1.17%) and Nov gasoline (RBX17 -0.62%) is -0.0072 (-0.44%). Wednesday's closes: Nov WTI crude +0.16 (+0.31%), Nov gasoline +0.0128 (+0.79%). Nov crude oil and gasoline on Wednesday closed higher on -5.731 million bbl drop in EIA crude inventories to a 1-3/4 year low, a bigger draw than expectations of -3.0 million bbl, and on the -11.3% plunge in U.S. crude production in the week of Oct 13 to to a 3-1/3 year low of 8.406 million bpd due to Hurricane Nate.

Metals prices this morning are mixed with Dec gold (GCZ17 +0.37%) +5.4 (+0.42%), Dec silver (SIZ17 +0.31%) +0.078 (+0.46%) and Dec copper (HGZ17 -0.65%) -0.021 (-0.66%). Wednesday's closes: Dec gold -3.2 (-0.25%), Dec silver -0.044 (-0.26%), Dec copper -0.0175 (-0.55%). Metals on Wednesday closed lower with Dec gold and Dec silver at 1-week lows. Metals prices were undercut by the rally in the S&P 500 to a new record high, which reduced safe-haven demand for precious metals, and by signs of weaker copper demand after U.S. Sep housing starts and building permits fell more than expected.

(Click on image to enlarge)

Disclosure: None.