Morning Call For Thursday, Dec. 1

OVERNIGHT MARKETS AND NEWS

Dec E-mini S&Ps (ESZ16 -0.14%) are down -0.08% and European stocks are down -0.75% as investors remained sidelined ahead of Friday's U.S. monthly non-farm payrolls report, Italy's vote Sunday on constitutional reform and next Thursday's ECB meeting. Interest rate concerns are also weighing on stocks with the 10-year T-note yield climbing to a 16-1/2 month high of 2.415%. The prospects on a Fed interest rate increase later this month is pressuring gold prices with Feb COMEX gold (GCG17 -0.20%) down -0.36% at a 9-3/4 month low. On the positive side is the +0.87% increase in Jan WTI crude oil prices (CLF17 +1.13%) to a 1-month high, which is bullish for energy producing stocks. On the positive side for European stocks was the unexpected decline in the Eurozone unemployment rate to the lowest in over 7 years in Oct. Asian stocks settled mostly higher: Japan +1.12%, Hong Kong +0.39%, China +0.72%, Taiwan +0.25%, Australia +1.10%, Singapore +0.81%, South Korea +0.09%, India -0.35%. Japan's Nikkei Stock Index rallied to a 10-3/4 month high as exporters gained on improved earnings prospects after the yen tumbled to a 9-1/2 month low against the dollar on Wednesday. China's Shanghai Composite closed higher on signs of economic strength after the China Nov manufacturing PMI unexpectedly expanded at the fastest pace in 4-1/2 years.

The dollar index (DXY00 -0.34%) is down -0.27%. EUR/USD (^EURUSD) is up +0.34%. USD/JPY (^USDJPY) is down -0.7%.

Mar 10-year T-note prices (ZNH17 -0.28%) are down -12 ticks at a new contract low.

The Eurozone Oct unemployment rate unexpectedly fell -0.1 to 9.8%, stronger than expectations of no change at 10.0% and the lowest in 7-1/3 years.

The China Nov manufacturing PMI (NBS) unexpectedly rose +0.5 to 51.7, stronger than expectations of -0.2 to 51.0 and matched July 2014 as the fastest pace of expansion in 4-1/2 years.

U.S. STOCK PREVIEW

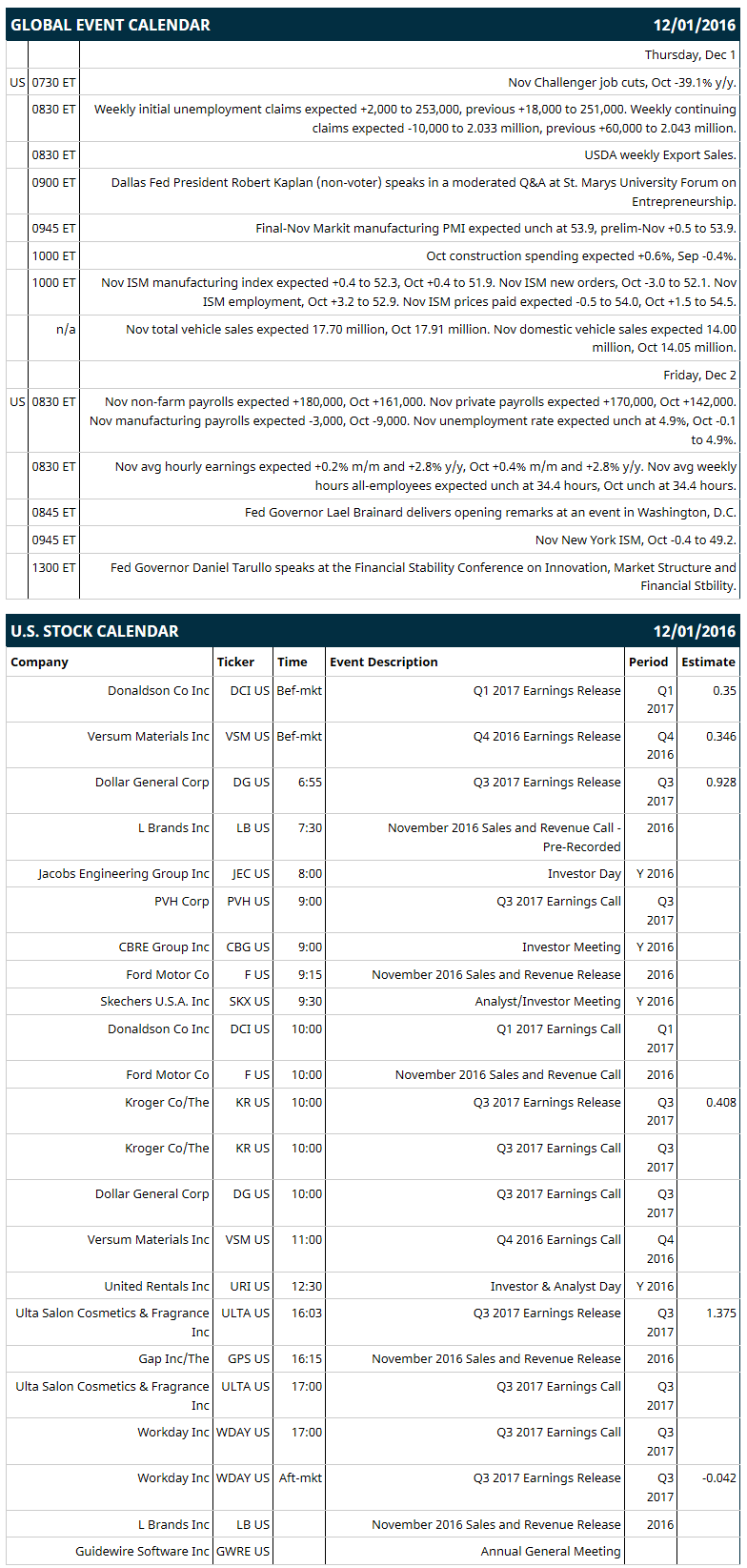

Key U.S. news today includes: (1) Nov Challenger job cuts (Oct -39.1% y/y), (2) weekly initial unemployment claims (expected +2,000 to 253,000, previous +18,000 to 251,000) and continuing claims (expected -10,000 to 2.033 million, previous +60,000 to 2.043 million), (3) Dallas Fed President Robert Kaplan (non-voter) speaks in a moderated Q&A at St. Mary’s University Forum on Entrepreneurship, (4) final-Nov Markit manufacturing PMI (expected unch at 53.9, prelim-Nov +0.5 to 53.9), (5) Oct construction spending (expected +0.6%, Sep -0.4%), (6) Nov ISM manufacturing index (expected +0.4 to 52.3, Oct +0.4 to 51.9), (7) Nov total vehicle sales (expected 17.70 million, Oct 17.91 million), and (8) USDA weekly Export Sales.

Russell 1000 earnings reports today include: Kroger (consensus $0.41), Dollar General (0.93), Ulta Salon (1.38), Donaldson (0.35), Versum Materials (0.35), Workday (-0.04).

U.S. IPO's scheduled to price today: Supportingsmallbusiness Inc, Innovative Industrial Properties (IIPR).

Equity conferences during the remainder of this week include: Credit Suisse Industrials Conference on Tue-Thu.

OVERNIGHT U.S. STOCK MOVERS

Wells Fargo (WFC +2.04%) was downgraded to 'Neutral' from 'Positive' at Susquehanna with a 12-month target price of $56.

Skechers (SKX +6.05%) was upgraded to 'Buy' from 'Neutral' at Buckingham Research Group with a price target of $31.

Cerner (CERN +0.02%) was downgraded to 'Market Perform' from 'Outperform' at Leerink Partners with a 12-month target price of $50.

PVH Corp. (PVH -0.08%) fell 2% in after-hours trading after it said it sees Q4 non-GAAP EPS of $1.13-$1.18, below consensus of $1.29.

Rockwell Collins (COL +0.41%) rallied over 3% in after-hours trading after it people familiar with the matter said it is under pressure from Starboard Value LP, one of its three biggest shareholders, to reconsider its $6.4 billion purchase of B/E/ Aerospace and instead explore alternative options, including selling itself.

Pure Storage (PSTG -2.17%) rose over 1% in after-hours trading after it said it added more than 300 customers in Q3 and that it sees Q4 revenue of $219 million-$227 million versus estimates of $221.2 million.

Semtech (SMTC -0.71%) gained 3% in after-hours trading after it reported Q3 adjusted EPS of 37 cents, better than consensus of 36 cents, and said it sees Q4 adjusted EPS of 33 cents-37 cents, above consensus of 33 cents.

Box Inc. (BOX -0.46%) gained almost 1% in after-hours trading after it reported a Q3 adjusted loss of -14 cents a share, narrower than consensus of -19 cents, and then raised its 2017 revenue view to $397 million-$398 million from an August 31 view of $394 million-$396 million.

Guess? (GES -1.54%) tumbled over 10% in after-hours trading after it reported Q3 EPS of 11 cents, weaker than consensus of 14 cents, and then cut its fiscal 2017 adjusted EPS view to 42 cents-52 cents from a prior view of 62 cents-75 cents.

Xencor (XNCR -2.96%) slid nearly 4% in after-hours trading after it announced a proposed public offering of common stock but gave no size.

La-Z-Boy (LZB -1.83%) climbed nearly 5% in after-hours trading after it reported Q2 EPS of 42 cents, higher than a preliminary view of 37 cents-39 cents.

Tilly's (TLYS -4.17%) surged over 15% in after-hours trading after it reported Q3 EPS of 22 cents, double consensus of 11 cents.

Fred's (FRED +1.01%) rose over 5% in after-hours trading after rescheduling the release of its Q3 results and Nov sales data to Dec 8 from Dec 2.

Rexnord (RXN +3.77%) fell 4% in after-hours trading after it announced a public offering of 7 million shares of preferred stock.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ16 -0.14%) this morning are down -1.75 points (-0.08%). Wednesday's closes: S&P 500 -0.27%, Dow Jones +0.01%, Nasdaq -1.23%. The S&P 500 on Wednesday rose to a new record high early but then fell back the rest of the day and closed lower. Stocks were undercut by weakness in technology stocks and by the 10 bp jump in the 10-year T-note yield that pressured the interest-rate-sensitive utility, phone and consumer staple stock sectors. Stocks were supported by the +216,000 increase in Nov ADP employment (stronger than expectations of +170,000 and the biggest increase in 5 months) and by the +7.0 point increase in the Nov Chicago PMI to 57.6 (stronger than expectations of +1.9 to 52.5 and the fastest pace of expansion in 1-3/4 years). Energy producer stocks got a big boost from the OPEC production cut agreement, which prompted a +9.31% surge in crude oil prices to a 1-month high.

Mar 10-year T-notes (ZNH17 -0.28%) this morning are down -12 ticks at a fresh contract low. Wednesday's closes: TYH7 -19.00, FVH7 -9.00. Mar 10-year T-note futures on Wednesday closed lower on the stronger-than-expected Nov ADP and Nov Chicago PMI reports, which may lead to faster-than-expected Fed rate hikes. T-notes were also undercut by the surge in crude prices to a 1-month high, which boosted inflation expectations.

The dollar index (DXY00 -0.34%) this morning is down -0.270 (-0.27%). EUR/USD (^EURUSD) is up +0.0036 (+0.34%). USD/JPY (^USDJPY) is -0.08 (-0.07%). Wednesday's closes: Dollar index +0.570 (+0.56%), EUR/USD -0.0061 (-0.57%), USD/JPY +2.08 (+1.85%). The dollar index on Wednesday closed higher on the stronger-than-expected U.S. Nov ADP and Nov Chicago PMI reports, which bolstered the case for the Fed to raise interest rates. The dollar was also boosted by the 10 bp increase in the 10-year T-note yield, which improved the dollar's interest rate differentials against the yen and sent USD/JPY soaring to an 8-1/2 month high.

Jan crude oil prices (CLF17 +1.13%) this morning are up +43 cents (+0.87%) and Jan gasoline (RBF17 +1.27%) is up +0.0158 (+1.07%), both at new 1-month highs. Wednesday's closes: Jan crude +4.21 (+9.31%), Jan gasoline +0.0975 (+7.08%). Jan crude oil and gasoline rallied sharply with Jan crude and Jan gasoline at 1-month highs. Crude oil prices were boosted by OPEC's agreement to cut its crude production by -1.2 million bpd to 32.5 million bpd after Saudi Arabia softened its stance and said Iran can increase its crude output to 3.9 million bpd. In addition, Russia said that it will cut its crude production by 300,000 bpd. Crude oil prices were also boosted by the unexpected -884,000 bbl decline in EIA crude inventories versus expectations for a +1.5 million bbl increase.

(Click on image to enlarge)

Disclosure: None.