Morning Call For October 14, 2016

OVERNIGHT MARKETS AND NEWS

Dec E-mini S&Ps (ESZ16 +0.47%) are up +0.48% and European stocks are up +1.94% after stronger-than-expected Chinese inflation data calmed market fears of a slowdown in China. Global stocks rallied after China Sep PPI unexpectedly rose +0.1% y/y, the first increase in 4-1/2 years. Stronger-than-expected Q3 earnings results for JPMorgan Chase are another positive for equity prices with JPMorgan up over 1% in pre-market trading after it reported Q3 EPS of $1.58, well above of consensus of $1.39. The markets await today's U.S. retail sales data and a speech by Fed Chair Yellen later today for clues as to when the Fed may raise interest rates. Asian stocks settled mostly higher: Japan +0.49%, Hong Kong +0.88%, China +0.08%, Taiwan -0.59%, Australia -0.03%, Singapore +0.35%, South Korea +0.46%, India +0.11%.

The dollar index (DXY00 +0.34%) is up +0.32%. EUR/USD (^EURUSD) is down -0.33%. USD/JPY (^USDJPY) is up +0.58%.

Dec 10-year T-note prices (ZNZ16 -0.20%) are down -10 ticks.

China Sep CPI rose +1.9% y/y, stronger than expectations of +1.6% y/y. Sep PPI unexpectedly rose 0.1% y/y, stronger than expectations of -0.3% y/y and the first increase in 4-1/2 years.

U.S. STOCK PREVIEW

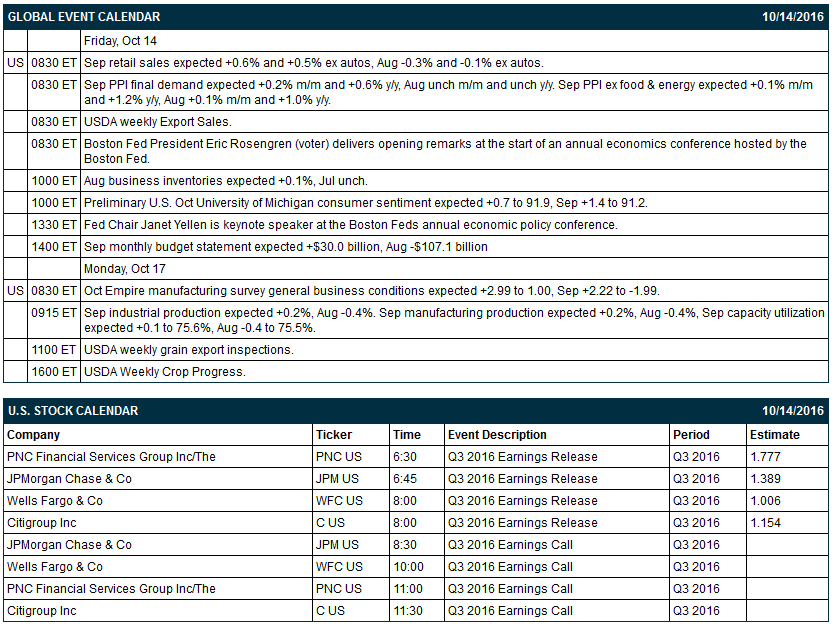

Key U.S. news today includes: (1) Sep retail sales (expected +0.6% and +0.5% ex autos, Aug -0.3% and -0.1% ex autos), (2) Sep PPI final demand (expected +0.2% m/m and +0.6% y/y, Aug unch m/m and unch y/y) and Sep PPI ex food & energy (expected +0.1% m/m and +1.2% y/y, Aug +0.1% m/m and +1.0% y/y), (3) Boston Fed President Eric Rosengren (voter) delivers opening remarks at the start of an annual economics conference hosted by the Boston Fed, (4) Aug business inventories (expected +0.1%, Jul unch), (5) preliminary Oct University of Michigan U.S. consumer sentiment index (expected +0.7 to 91.9, Sep +1.4 to 91.2), (6) Fed Chair Janet Yellen is keynote speaker at the Boston Fed’s annual economic policy conference, (7) Sep monthly budget statement (expected +$30.0 billion, Aug -$107.1 billion) and (8) USDA weekly Export Sales.

S&P 500 companies that report earnings today include: Citigroup (consensus $1.15), JPMorgan Chase (1.39), Wells Fargo (1.01), PNC Financial (1.78).

U.S. IPO's scheduled to price today: ICC Holdings (ICCH).

Equity conferences during the remainder of this week include: none.

OVERNIGHT U.S. STOCK MOVERS

JPMorgan Chase (JPM -0.57%) is up over 1% in pre-market trading after it reported Q3 EPS of $1.58, higher than consensus of $1.39.

Advanced Micro Devices (AMD -1.96%) gained nearly 3% in pre-market trading after it said Alibaba Group Holding Ltd. plans to provide cloud-computing services based on AMD's graphic semiconductors.

HP Inc. (HPQ -1.30%) slipped over 1% in pre-market trading after it said it will eliminate as many as 4,000 jobs in the next 3 years to bring costs in line with slumping demand for personal computers and printers.

Estee Lauder (EL -0.03%) was downgraded to ‘Neutral' from 'Overweight' at Piper Jaffray with a 12-month target price of $90.

Ollie's Bargain Outlet Holdings (OLLI -1.89%) was rated a new 'Buy' at MKM Partners with a 12-month target price of $33.

Zumiez (ZUMZ -2.54%) rose 3% in after-hours trading after it was upgraded to 'Overweight' from 'Neutral' at Piper Jaffray with a price target of $28.

Restaurant Brands International (QSR -1.09%) was rated a new 'Outperform' at BMO Capital Markets with a target price of $52.

Under Armour (UA -0.88%) gained over 1% in after-hours trading after it was upgraded to 'Overweight' from 'Neutral' at Piper Jaffray.

Natural Health Trends (NHTC -3.10%) fell over 12% in after-hours trading after it announced preliminary Q3 revenue of $70.7 million versus $80.8 million q/q.

Landmark Infrastructure Partners LP (LMRK -1.15%) dropped 5% in after-hours trading after it filed to sell 3 million common units and use the proceeds to repay debt.

Reed's Inc. (REED +1.74%) jumped over 10% in after-hours trading after it reported a Q3 loss of -2 cents per share, narrower than consensus of -4 cents.

Enzo Biochem (ENZ -0.39%) rose over 6% in after-hours trading after it reported a Q4 adjusted loss of -4 cents per share, a narrower loss than consensus of -6 cents.

Scorpio Bulkers (SALT +0.26%) climbed nearly 3% in after-hours trading after the president of the company, Robert Bugbee, bought 30,000 shares of the stock.

Aerohive Networks (HIVE -2.26%) tumbled over 15% in after-hours trading after it lowered guidance on Q3 adjusted EPS to a net loss of -6 cents to -7 cents, weaker than an August 3 view of -1 cent to -7 cents.

Smith Micro Software (SMSI +0.91%) plunged 20% in after-hours trading after it said preliminary Q3 revenue will be $6.5 million, well below a prior view of $7.9 million-$8.4 million, citing several large deals that were not closed as expected.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ16 +0.47%) this morning are up +10.25 points (+0.48%). Thursday's closes: S&P 500 -0.31%, Dow Jones -0.25%, Nasdaq -0.34%. The S&P 500 on Thursday slumped to a 3-month low and closed lower on concern about global economic growth after China Sep exports fell -10.0% y/y, weaker than expectations of -3.3% y/y and the biggest decline in 7 months. Stocks were also undercut by Philadelphia Fed President Harker's comment that he supports a Fed rate hike by year-end. Stocks found a little support after U.S. weekly jobless claims were unchanged at 246,000, better than expectations of +4,000 to 253,000 and the fewest since Nov of 1973.

Dec 10-year T-notes (ZNZ16 -0.20%) this morning are down -10 ticks. Thursday's closes: TYZ6 +12.00, FVZ6 +7.50. Dec 10-year T-notes on Thursday closed higher on increased safe-haven demand with the sell-off in stocks. T-notes were also boosted by the -10.0% y/y drop in Chinese exports that could indicate more trouble in China that could delay a Fed rate hike.

The dollar index (DXY00 +0.34%) this morning is up +0.313 (+0.32%). EUR/USD (^EURUSD) is down -0.0037 (-0.33%). USD/JPY (^USDJPY) is up +0.60 (+0.58%). Thursday's closes: Dollar index -0.450 (-0.46%), EUR/USD +0.0049 (+0.45%), USD/JPY -0.50 (-0.48%). The dollar index on Thursday closed lower on concern about the global economy that may keep the Fed from raising interest rates after China Sep exports fell -10.0% y/y, the biggest decline in 7 months. In addition, there was weakness in USD/JPY after a plunge in stocks boosted the safe-haven demand for the yen.

Nov WTI crude oil (CLX16 +1.11%) this morning is up +54 cents (+1.07%) and Nov gasoline (RBX16 +0.63%) is up +0.0049 (+0.33%). Thursday's closes: Nov crude +0.37 (+0.74%), Nov gasoline +0.0186 (+1.27%). Nov crude oil and gasoline on Thursday closed higher on a weaker dollar and on the -1.318 million bbl drop in crude supplies at Cushing to a 10-month low. Gasoline prices received support from the -1.07 million bbl decline in EIA gasoline inventories (versus expectations of -900,000 bbl). However, crude oil prices were undercut by the +4.85 million bbl gain in EIA crude inventories, more than double expectations of +2.0 million bbl. Crude oil was also undercut by doubts about whether OPEC members would be able to agree on cuts in output after Iraq and Venezuela disputed OPEC data on the amount of oil each country was producing.

(Click on image to enlarge)

Disclosure: None.