Morning Call For November 19, 2015

OVERNIGHT MARKETS AND NEWS

December E-mini S&Ps (ESZ15 +0.32%) are up +0.35% at a 1-week high and European stocks are up +0.91% at a 1-1/2 week high after the minutes of the Oct 27-28 FOMC meeting on Wednesday indicated the U.S. economy is strong enough to handle an interest rate increase at next month's FOMC meeting, while policy makers stressed that the pace of tightening will be gradual. Stronger-than-expected quarterly earnings results from Salesforce.com and Keurig Green Mountain are also giving equities a boost, while an increase in M&A activity is supportive as well with Allergan up over 1% in pre-market trading after Pfizer was said to be in advanced talks to buy the company for as much as $150 billion. Asian stocks settled higher: Japan +1.07%, Hong Kong +1.41%, China +1.36%, Taiwan +1.64%, Australia +2.13%, Singapore +1.17%, South Korea +1.39%, India +1.41%. Asian markets all closed higher, with Japan's Nikkei Stock Index at a 2-3/4 month high, after the Oct 27-28 FOMC minutes stated that the Fed's pace of tightening will be gradual.

The dollar index (DXY00 -0.43%) is down -0.51%. EUR/USD (^EURUSD) is up +0.50%. USD/JPY (^USDJPY) is down -0.44% as the yen rallied after the BOJ left monetary policy unchanged and said "inflation expectations appear to be rising."

Dec T-note prices (ZNZ15 +0.02%) are unchanged.

ECB Executive Board member Praet said he sees confirmation of downside risks in the global economy and that ECB policy makers are having "rich discussions" and will decide in December what further policy actions are needed and that more reductions in interest rates are "part of a toolbox."

U.S. STOCK PREVIEW

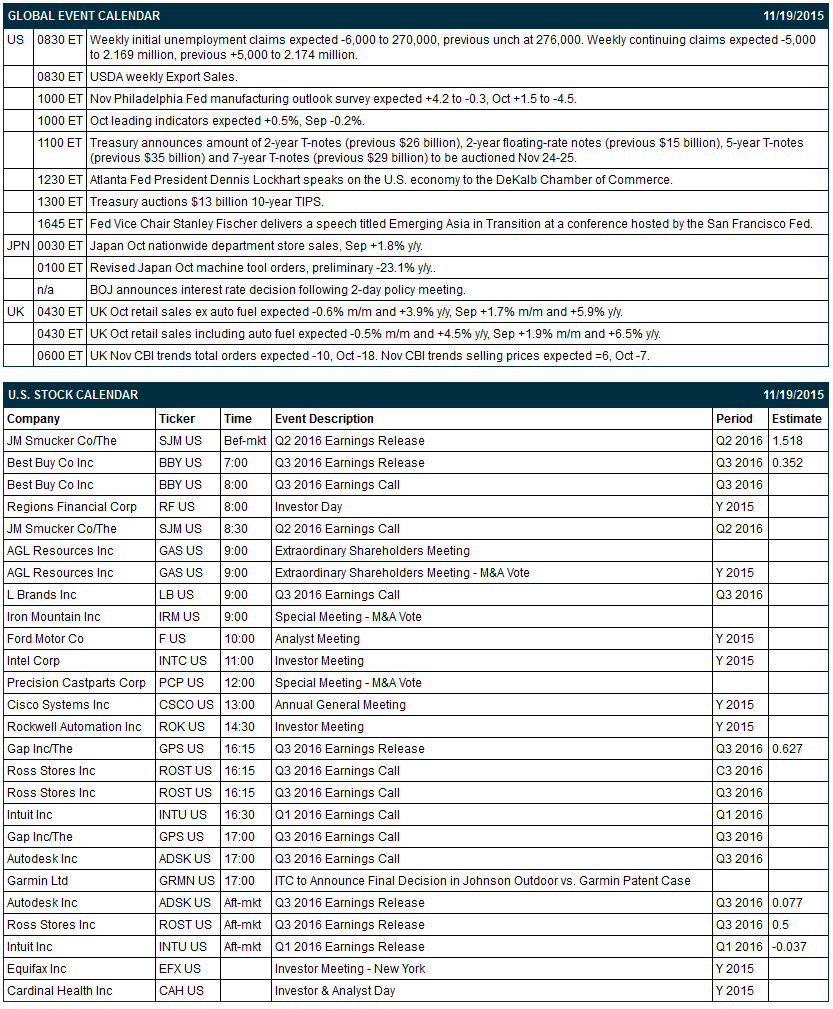

Key U.S. news today includes: (1) weekly initial unemployment claims (expected -6,000 to 270,000, previous unch at 276,000) and continuing claims (expected -5,000 to 2.169 million, previous +5,000 to 2.174 million), (2) Nov Philadelphia Fed manufacturing outlook survey (expected +4.2 to -0.3, Oct +1.5 to -4.5), (3) Oct leading indicators (expected +0.5%, Sep -0.2%), (4) Atlanta Fed President Dennis Lockhart's speech on the U.S. economy to the DeKalb Chamber of Commerce, (5) the Treasury's auction of $13 billion 10-year TIPS, (6) Fed Vice Chair Stanley Fischer's speech titled “Emerging Asia in Transition” at a conference hosted by the San Francisco Fed.

There are 6 of the S&P 500 companies that report earnings today: Best Buy (consensus $0.35), JM Smucker (1.52), GAP (0.63), Autodesk (0.08), Ross Stores (0.50), Intuit (-0.04).

U.S. IPO's scheduled to price today: Bright Horizons Family Solutions (BFAM), Habit Restaurants (HABT), Noble Midstream Partners (NBLX), Truck Hero (TRUK), Congatec Holding (CONG), Duluth Holdings (DLTH).

Equity conferences this week include: Canaccord Genuity Medical Technology and Diagnostics Forum on Thu, Jefferies Global Health Care Conference on Thu, Scotiabank Canadian Energy Infrastructure Conference on Thu, UBS Industrials and Transportation Conference on Thu-Fri.

OVERNIGHT U.S. STOCK MOVERS

Allergan (AGN +4.53%) rose over 1% in pre-market trading after Pfizer is said to be near a deal to acquire the company for as much as $380 a share.

Keurig Green Mountain (GMCR +0.92%) surged over 15% in pre-market trading after it reported Q4 adjusted EPS of 85 cents, well above consensus of 71 cents.

Salesforce.com (CRM +0.14%) rose over 7% in pre-market trading after it reported Q3 adjusted EPS of 21 cents, higher than consensus of 19 cents, and then raised guidance on fiscal 2016 adjusted EPS to 74 cents-75 cents from an August estimate of 70 cents-72 cents, above consensus of 73 cents.

Best Buy (BBY +2.02%) dropped over 8% in pre-market trading after it reported Q3 domestic comparable sales were up +0.8%, weaker than consensus of +1.4%.

General Dynamics (GD +0.59%) was upgraded to a 'Buy' at Argus Research with a price target of $160.

NetApp (NTAP -0.83%) climbed over 4% in after-hours trading after it reported Q2 adjusted EPS of 61 cents, better than consensus of 57 cents.

DaVita (DVA +1.15%) slid almost 2% in after-hours trading after it said the U.S. Department of Justice is conducting a false claims investigation into DaVita’s wholly owned subsidiary, RMS Lifeline.

Hillenbrand (HI +2.10%) reported Q4 EPS of 55 cents, right on consensus, but reported Q4 revenue of $392 million, below consensus of $421 million.

L Brands (LB +1.55%) reported Q3 adjusted EPS of 55 cents, above consensus of 53 cents, but then said it sees fiscal 2015 EPS of $3.69-$3.79, below consensus of $3.79.

Semtech (SMTC +1.53%) dropped over 6% in after-hours trading after it reported Q3 adjusted EPS of 19 cents, below consensus of 24 cents, and said it sees Q4 adjusted EPS of 14 cents-18 cents, weaker than consensus of 23 cents.

Delta Airlines (DAL -0.04%) rallied nearly 3% in after-hours trading after it said it will buy another 32% stake in Aeromexico and increase its total stake in the company to 49%.

SunEdison (SUNE +7.62%) dropped over 10% in after-hours trading after Blackstone said it is not interested in investing in the company.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ15 +0.32%) this morning are up +7.25 points (+0.35%). Wednesday's closes: S&P 500 +1.62%, Dow Jones +1.42%, Nasdaq +1.92%. The S&P 500 on Wednesday closed sharply higher on reduced interest rate concerns after the Oct 27-28 FOMC minutes showed that policy makers stressed that they want the pace of interest rate increases to be gradual and on the +4.1% increase in Oct building permits, a proxy for future construction, to 1.150 million, more than expectations of +3.8% to 1.147 million. Technology stocks received a boost from a 3% gain in Apple after Goldman Sachs added Apple to its "Conviction Buy" list.

Dec 10-year T-notes (ZNZ15 +0.02%) this morning are unchanged. Wednesday's closes: TYZ5 -2.50, FVZ5 -2.25. Dec T-note prices on Wednesday closed lower on the minutes of the Oct 27-28 FOMC meeting showing that policy makers wanted to convey that "it may well become appropriate" to raise the benchmark lending rate in December. T-notes were also undercut by reduced safe-haven demand tied to the rally in stocks. T-note prices rebounded from their worst levels after the FOMC minutes said that any interest rate increases would be gradual.

The dollar index (DXY00 -0.43%) this morning is down -0.505 (-0.51%). EUR/USD (^EURUSD) is up +0.0053 (+0.50%). USD/JPY (^USDJPY) is down -0.55 (-0.44%). Wednesday's closes: Dollar Index +0.021 (+0.02%), EUR/USD +0.0018 (+0.17%), USD/JPY +0.19 (+0.15%). The dollar index on Wednesday rose to a 7-month high but fell back and closed little changed. The dollar received a boost from the minutes of the Oct 27-28 FOMC that said it may be "appropriate" to raise interest rates at next month's FOMC meeting. In addition, USD/JPY rallied to a 2-3/4 month high as strength in stocks reduced the safe-haven demand for the yen. The dollar erased its advance after the Oct 27-28 FOMC minutes stated that any Fed rate hikes would be gradual.

Dec crude oil (CLZ15 -0.79%) this morning is unchanged and Dec gasoline (RBZ15 +1.33%) is up +0.0241 (+1.90%). Wednesday's closes: CLZ5 +0.08 (+0.20%), RBZ5 +0.0395 (+3.19%). Dec crude oil and gasoline on Wednesday erased early losses and closed higher on the slide in the dollar which fell back from a 7-month high and closed little changed. Dec crude had posted a 2-1/2 month low on bearish factors that included (1) the +1.5 million bbl increase in crude stockpiles at Cushing, more than expectations of +1.1 million bbl, and (2) the unexpected +1.009 million bbl increase in EIA gasoline supplies, more than expectations of a -1.5 million bbl draw.

(Click on image to enlarge)

Disclosure:None.