Morning Call For June 24, 2015

OVERNIGHT MARKETS AND NEWS

September E-mini S&Ps (ESU15 -0.20%) are down -0.20% and European stocks are down -0.47% after Greek Prime Minister Tsipras said that creditors didn't accept his government's proposals for more aid. According to a person familiar with the matter, a new set of measures were sent to the Greek government today ahead of a meeting between Greek Prime Minister Tsipras and the three creditor institutions; the ECB, the IMF and the European Commission. Another negative for European stocks was the decline in German business confidence after the Jun IFO business climate fell more than expected to a 4-month low. Asian stocks closed mostly higher: Japan +0.28%, Hong Kong +0.26%, China +2.48%, Taiwan +0.07%, Australia +0.04%, Singapore +0.35%, South Korea +0.17%, India -0.27%. Japan's Nikkei Stock Index rallied to a fresh 15 year high after the minutes of the May BOJ policy meeting showed many policy makers want to continue monetary stimulus until Japan's inflation rate stabilizes at 2%. A rally in shipping stocks also aided gains in Asian stocks after the Baltic Dry Index, a gauge of commodity shipping rates, rose 1.4% to its highest close this year.

Commodity prices are mostly higher due to a weaker dollar. Aug crude oil (CLQ15 -0.05%) is up +0.20%, Aug gasoline (RBQ15 +0.77%) is up +0.59%. Metals prices are stronger. Aug gold (GCQ15 unch) is up +0.08%. Jul copper (HGN15 +0.46%) is up +0.06%. Agricultural prices are weaker.

The dollar index (DXY00 -0.32%) is down -0.24%. EUR/USD (^EURUSD) is up +0.29%. USD/JPY (^USDJPY) is down -0.02%.

Sep T-note prices (ZNU15 +0.10%) are up +2.5 ticks.

Greece's creditors handed Greece an overhauled set of measures the country must meet in order to receive bailout funds ahead of a meeting today in Brussels between Greek Prime Minister Tsipras and the heads of the three creditor institutions; ECB President Draghi, IMF Managing Director Lagarde and European Commission President Juncker. Eurozone finance ministers will then meet later today in an effort to reach a deal on more aid for Greece before its current bailout expires and 1.5 billion euros in debt payments come due to the IMF on Jun 30.

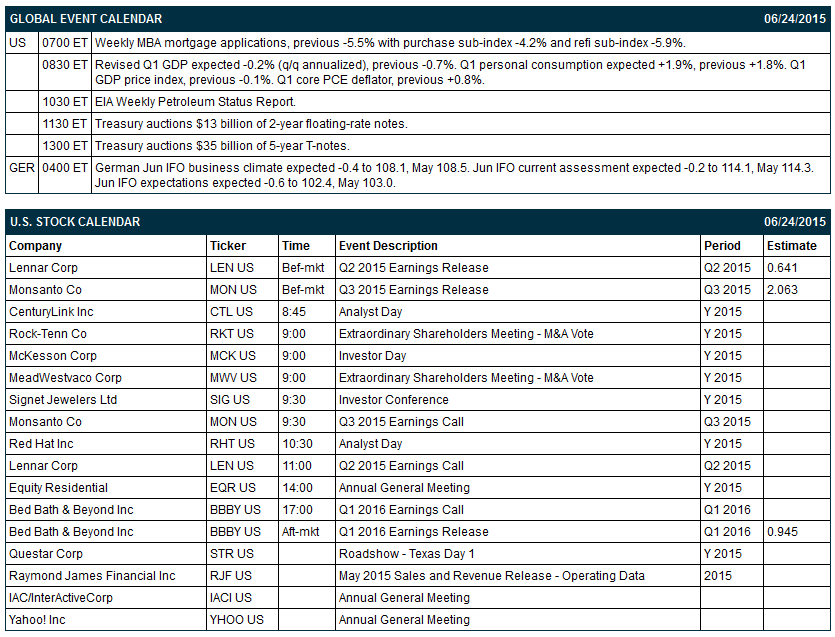

The German Jun IFO business climate fell -1.1 to 107.4, weaker than expectations of -0.4 to 108.1 and the lowest in 4 months.

U.S. STOCK PREVIEW

Key U.S. news today includes: (1) weekly MBA mortgage applications (last week -5.5% with purchase sub-index -4.2% and refi sub-index -5.9%), (2) Q1 GDP revision (expected -0.2% vs last -0.7%), and (3) the Treasury's auction of $13 billion of 2-year floating-rate notes and $35 billion of 5-year T-notes.

There are 3 of the Russell 1000 companies that report earnings today: Lennar (0.64), Monsanto (2.06), Bed, Bath & Beyond (0.95).

U.S. IPO's scheduled to price today include: TransUnion (TRU), Milacron Holdings (MCRN), Gener8 Maritime (GNRT), Wayne Farms (WNFM), Glaukos (GKOS), Lantheus Holdings (LNTH), Catabasis Pharmaceuticals (CATB).

Equity conferences during the remainder of this week include: Global Hunter Securities Energy Conference on Tue-Wed, Jefferies Global Consumer Conference on Tue-Wed, Oppenheimer Consumer Conference on Tue-Wed, 3rd Annual Mobile Pharma Summit on Wed, and Sanford C. Bernstein Media Summit on Wed.

OVERNIGHT U.S. STOCK MOVERS

Citigroup (C +0.77%) and Goldman Sachs (GS +0.87%) were both downgraded to 'Hold' from 'Buy' at Deutsche Bank.

McCormick (MKC +0.06%) was upgraded to 'Outperform' from 'Market Perform' at Bernstein.

Electronic Arts (EA -0.06%) was upgraded to 'Buy' from 'Hold' at Jefferies with a price target of $80.

Anthem (ANTM -0.61%) was initiated with an 'Outperform' at RBC Capital with a price target of $222.

UnitedHealth (UNH +2.07%) was initiated with an 'Outperform' at RBC Capital with a price target of $159.

Comerica (CMA +1.10%) was upgraded to 'Buy' from 'Neutral' at BofA/Merril Lynch.

BHP Billiton (BHP +1.48%) was upgraded to 'Neutral' from 'Underperform' at Credit Suisse.

Lennar (LEN -1.01%) reported Q2 EPS of 79 cents, better than consensus of 64 cents.

Sysco (SYY -0.03%) dropped nearly 3% in after-hours trading after a federal judge blocked its bid to acquire U.S. Foods.

Ford (F +1.06%) was upgraded to 'Buy' from 'Neutral' at Goldman Sachs.

General Motors (GM +0.30%) was downgraded to 'Neutral' from 'Buy' at Goldman Sachs.

Columbia Pipeline Group (CPGX) will replace Allegheny Technologies (ATI +3.22%) in the S&P 500 as of the close of trading on July 1.

Netflix (NFLX +0.93%) rose nearly 3% in after-hours trading after it announced a seven-for-one stock split.

MARKET COMMENTS

September E-mini S&Ps (ESU15 -0.20%) this morning are down -4.25 points (-0.20%). Tuesday's closes: S&P 500 +0.06%, Dow Jones +0.13%, Nasdaq +0.10%. The S&P 500 on Tuesday closed slightly higher on strong global manufacturing data as the Eurozone Jun manufacturing PMI rose +0.3 to a 14-month high of 52.5 and the China Jun HSBC flash manufacturing PMI rose +0.4 to 49.6, stronger than expectations of +0.2 to 49.4. Stocks also received a boost from the +2.2% increase in U.S. May new home sales to 546,000, stronger than expectations of +1.2% to 523,000 and the highest in 7-1/4 years.

Sep 10-year T-notes (ZNU15 +0.10%) this morning are up +2.5 ticks. Tuesday's closes: TYU5 -12.00, FVU5 -6.25. Sep T-notes on Tuesday closed lower on the stronger-than-expected U.S. May new home sales report of +2.2% to a 7-1/4 year high of 546,000, and an increase in inflation expectations after the 10-year T-note breakeven inflation rate climbed to a 1-1/2 month high.

The dollar index (DXY00 -0.32%) this morning is down -0.233 (-0.24%). EUR/USD (^EURUSD) is up +0.0032 (+0.29%). USD/JPY (^USDJPY) is down -0.02 (-0.02%). Tuesday's closes: Dollar Index +1.103 (+1.17%), EUR/USD -0.01731 (-1.53%), USD/JPY +0.574 (+0.47%). The dollar index on Tuesday rose to a 1-week high and closed higher on the stronger-than-expected U.S. May new home sales report, which may prompt the Fed to raise interest rates sooner rather than later.

Aug WTI crude oil (CLQ15 -0.05%) this morning is up +12 cents (+0.20%). Aug gasoline (RBQ15 +0.77%) is up +0.0121 (+0.59%). Tuesday's closes: CLQ5 +0.63 (+1.04%), RBQ5 +0.0551 (+2.76%). Aug crude oil and gasoline on Tuesday closed higher on (1) expectations that Wednesday's weekly EIA data will show that crude inventories fell -1.5 million bbl, the eighth straight weekly decline, and (2) signs of strength in the global economy after the Eurozone Jun Markit manufacturing PMI and the China Jun HSBC manufacturing PMI were both stronger than expected.

Click on picture to enlarge

Disclosure: None.