Morning Call For June 17, 2015

OVERNIGHT MARKETS AND NEWS

September E-mini S&Ps (ESU15 +0.07%) this morning are slightly higher by +3.75 points (+0.18%) as the market hopes for a relatively dovish outcome from today's FOMC meeting. The EuroStoxx 50 index is down -0.35% this morning as Greek woes continue and the Greek central bank warned that Greece would be put on a "painful" course towards default and a Greek exit from the Eurozone if it cannot reach an agreement with its creditors. Asian stocks today closed mostly higher: Japan -0.19%, Hong Kong +0.70%, China +1.65%, Taiwan -0.25%, Australia +1.08%, Singapore +0.84%, South Korea +0.24%, India +0.55%, Turkey +0.46%.

The dollar index (DXY00 -0.15%) is down -0.20 points (-0.21%) this morning with EUR/USD (^EURUSD) up +0.0009 (+0.08%) and USD/JPY (^USDJPY) up +0.60 (+0.49%). Sep 10-year T-note prices (ZNU15 -0.10%) are down -4.5 ticks.

Commodity prices are up +0.59% this morning due to part to a weaker dollar. Jul crude oil (CLN15 +1.72%) is up +1.15 and Jul gasoline (RBN15+2.09%) is up sharply by +0.0516 (+2.43%) as the market looks for the 7th consecutive decline in U.S. crude oil inventories in today's weekly EIA report. Metals prices are mixed with Aug gold (GCQ15 -0.21%) down 2.7 (-0.23%), July silver (SIN15 -0.19%) down -0.025 (-0.16%), and Jul copper (HGN15+0.23%) up +0.010 (+0.38%).

Grain prices are higher this morning on concern that rain from Tropical Storm Bill will delay planting. Softs are mixed with sugar and coffee higher, but with cocoa and cotton lower.

The Greek central bank released a report today saying that Greece would be put on a "painful" course towards default and an exit from the Eurozone if the Greek government does not reach a new bailout agreement with its creditors. The bank said that there was a Greek bank deposit outflow of about 30 billion euros between October and April.

The British pound today rallied by +0.6% to a 1-month high after the BOE's June policy meeting minutes showed that BOE members believe that the restraints on the economy and inflation are fading. The MPC said that factors holding back inflation were "likely to dissipate fairly shortly," and could strengthen "notably" by year-end. The MPC added, "The strength of the headwinds to growth had begun to ease. As they ease further over time, the interest rate required to keep the economy operating at normal levels of capacity and inflation at the target was likely to continue to rise."

U.S. STOCK PREVIEW

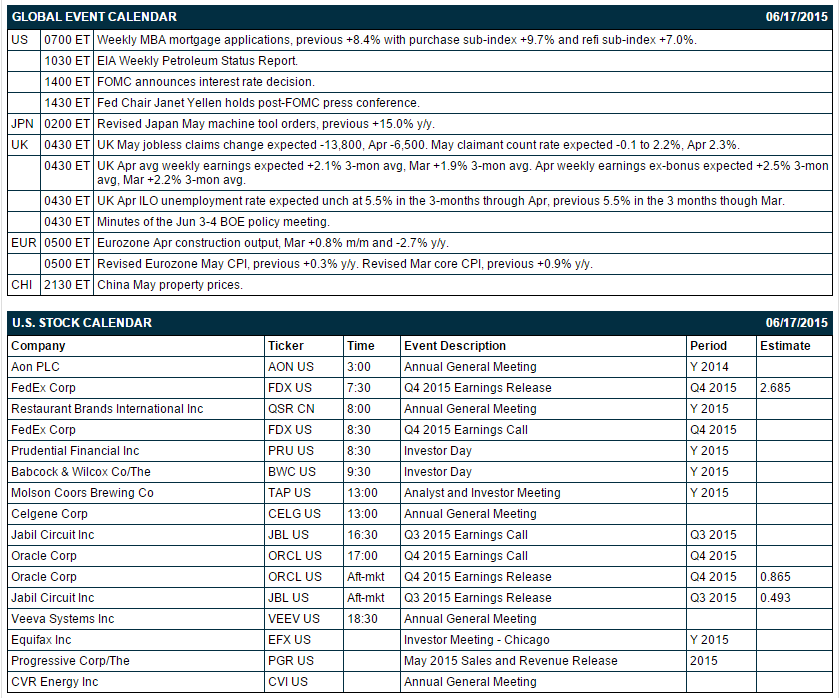

Key U.S. news today includes: (1) weekly MBA mortgage applications (last week +8.4% with purchase sub-index +9.7% and refi sub-index +7.0%), and (2) the second day of the FOMC's 2-day meeting, which concludes with the release of updated Fed projections and a press conference by Fed Chair Yellen.

There are 3 of the Russell 1000 companies that report earnings today: FedEx (consensus $2.69), Oracle (0.87), Jabil Circuit (0.49).

U.S. IPO's scheduled to price today include: FitBit (FIT), Univar (UNVR).

Equity conferences during the remainder of this week include: BIO International Convention on Tue-Wed, Real Estate Investment World Asia 2015 on Wed, Goldman Sachs dotCommerce Day on Thu, JP Morgan Oil & Gas Forum on Thu, Leerink Health Care Services Conference on Thu, Telsey Advisory Group Advertising Trends Symposium on Thu.

September E-mini S&Ps this morning are slightly higher by +3.75 points (+0.18%) as the market hopes for a relatively dovish outcome from today's FOMC meeting. Tuesday's closes: S&P 500 +0.57%, Dow Jones +0.64%, Nasdaq +0.52%. The S&P 500 on Tuesday closed higher on (1) the unexpected +11.8% jump in U.S. May building permits, a proxy for future home building, to 1.100 million, stronger than expectations of -3.5% and the most in 7-3/4 years, and (2) strength in health-care stocks on expectations of increased M&A activity in the sector after reports of a merger between Aetna and UnitedHealth. Stocks saw early weakness after Greece signaled it wouldn't make additional concessions in order to receive bailout funds.

OVERNIGHT U.S. STOCK MOVERS

- FedEx (FDX -0.29%) reported Q4 adjusted EPS of $2.66, stronger than the consensus of $2.43. FedEx FY16 guidance of adjusted EPS of $10.60-$11.10 was in line with the consensus of $10.88.

- Allergan (AGN -1.11%) agreed to acquire KYTHERA (KYTH) for $75 per share or approximately $2.1 billion.

- Hill-Rom (HRC -0.27%) will acquire Welch Allyn for about $2.05 billion in cash and stock.

- Celgene (CELG +0.10%) announced an additional $4 billion share repurchase authorization.

- Deutsche Telekom and Comcast are in talks over possible T-Mobile sale, according to a Reuters report.

- UBS added Cigna (CI +0.35%) to its Most Preferred List and raised its target to $175.

- British American Tobacco (BTI +2.85%) was upgraded to 'Neutral' from 'Sell' at Goldman Sachs.

- NovaBay (NBY -10.96%) filed to sell 16.34 million shares of common stock for holders.

- La-Z-Boy (LZB +1.76%) reported Q4 adjusted EPS of 38 cents, right on consensus, although Q4 revenue of $374.94 million was weaker than consensus of $379.13 million.

- Adobe (ADBE +1.32%) dropped over 1.5% in after-hours trading after it reported Q2 EPS of 48 cents, higher than consensus of 45 cents, but then lowered guidance on fiscal 2015 revenue estimate to $4.845 billion, below consensus of $4.880 billion.

- Bob Evans (BOBE -0.73%) rose 4% in after-hours trading after it reported Q4 EPS of 56 cents, much better than consensus of 41 cents.

MARKET COMMENTS

Sep 10-year T-notes this morning are down -4.5 ticks. Tuesday's closes: TYU5 +10.00, FVU5 +5.25. Sep 10-year T-notes on Tuesday posted a 1-1/2 week high on the larger-than-expected decline in U.S. May housing starts and on increased safe-haven demand for T-notes after Greece's PM indicated the Greek government will not make additional concessions.

The dollar index is down -0.20 points (-0.21%) this morning with EUR/USD up +0.0009 (+0.08%) and USD/JPY up +0.60 (+0.49%). Tuesday's closes: Dollar Index +0.189 (+0.20%), EUR/USD -0.00354 (-0.31%), USD/JPY -0.054 (-0.04%). The dollar index on Tuesday settled higher on weakness in EUR/USD tied to the decline in the German Jun ZEW expectations index to a 7-month low and increased concerns about a Greek exit from the Eurozone. The dollar also rallied on short covering ahead of Wednesday's post-FOMC meeting statement that may prepare the markets for a Fed interest rate increase.

Jul crude oil is up +1.15 and Jul gasoline is up sharply by +0.0516 (+2.43%) as the market looks for the 7th consecutive decline in U.S. crude oil inventories in today's weekly EIA report. Tuesday's closes: CLN5 +0.58 (+0.97%), RBN5 +0.0479 (+2.28%). Jul crude oil and gasoline prices on Tuesday closed higher on expectations that Wednesday’s weekly EIA report will show the 7th consecutive decline in U.S. crude oil inventories, and on reduced crude output from the Gulf of Mexico after Tropical Storm Bill forced the closure of several oil installations in the Gulf.

Disclosure: None.