Morning Call For February 18, 2016

OVERNIGHT MARKETS AND NEWS

March E-mini S&Ps (ESH16 +0.42%) are up +0.36% at a 2-week high and European stocks are up +1.06% at a 1-1/2 week high as crude oil moved higher and after St. Louis Fed President Bullard said the Fed should delay interest rate hikes. U.S. stock index futures fell back from their best levels as Wal-Mart slid 3% in pre-market trading after it lowered its sales forecast for the year. Mar crude is up +2.45% at a 2-week high after API data late Wednesday showed U.S. crude inventories fell -3.26 million bbl and St. Louis Fed President Bullard said that recent turmoil that has contributed to a decline in inflation expectations gives the Fed scope to delay further interest rate increases. Asian stocks settled mostly higher: Japan +2.28%, Hong Kong +2.32%, China -0.16%, Taiwan +1.22%, Australia +2.25%, Singapore +1.67%, South Korea +1.21%, India +1.14%. China's Shanghai Composite retreated from a 3-week high and closed lower after government data showed inflation picked up in January on rising food prices.

The dollar index (DXY00 +0.12%) is up +0.10%. EUR/USD (^EURUSD) is down -0.28%. USD/JPY (^USDJPY) is down -0.23%.

Mar T-note prices (ZNH16 -0.02%) are down -1 tick.

St. Louis Fed President Bullard suggested Wednesday evening that he favors delaying further interest rate hikes when he said "I regard it as unwise to continue a normalization strategy in an environment of declining market-based inflation expectations."

The Organization for Economic Cooperation and Development (OECD) cut its 2016 global GDP forecast to 3.0%, down from a 3.3% projection in Nov, citing a slowdown in Germany and the U.S. along with exchange-rate volatility that may hurt emerging markets.

The China Jan CPI rose +1.8% y/y, weaker than expectations of +1.9% y/y, but still the fastest pace of increase in 5 months. Jan PPI fell -5.3% y/y, a smaller decline than expectations of -5.4% y/y.

U.S. STOCK PREVIEW

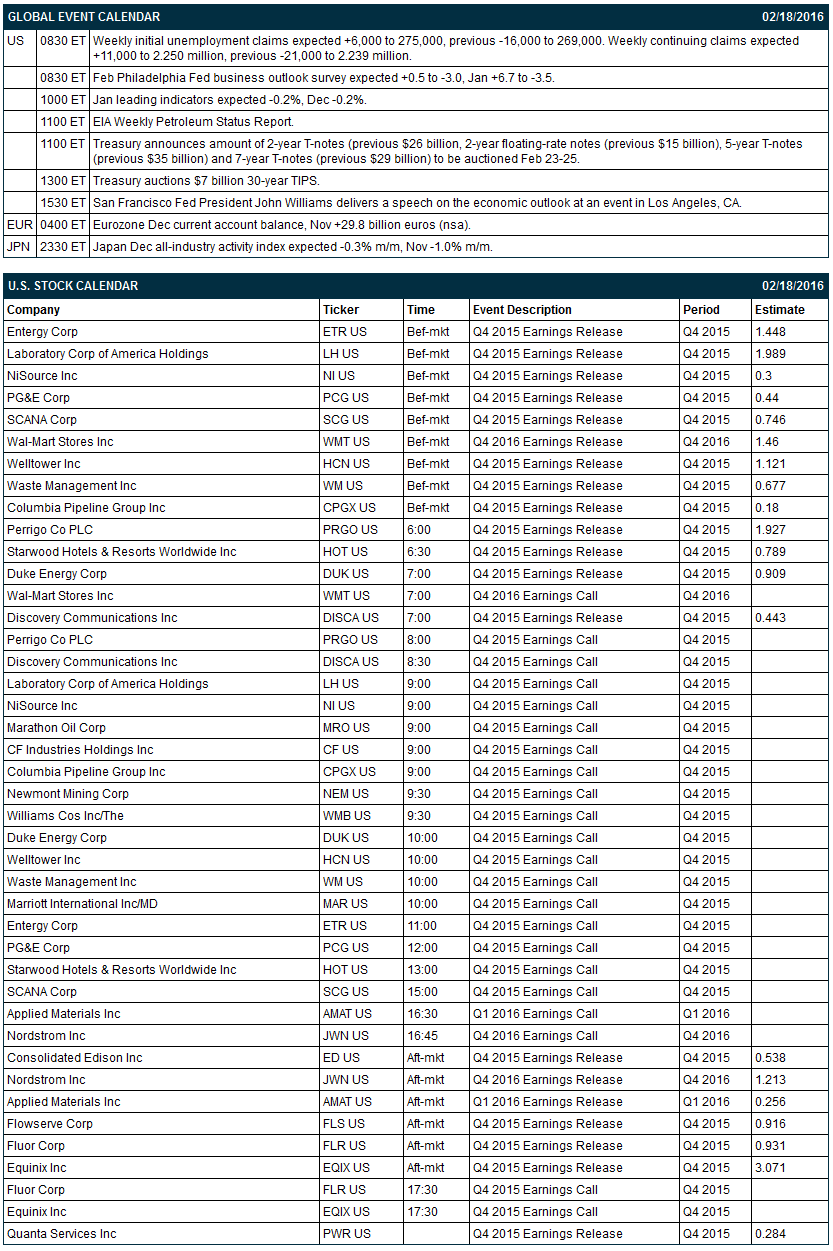

Key U.S. news today includes: (1) weekly initial unemployment claims (expected +6,000 to 275,000, previous -16,000 to 269,000) and continuing claims (expected +11,000 to 2.250 million, previous -21,000 to 2.239 million), (2) Feb Philadelphia Fed business outlook index (expected +0.5 to -3.0, Jan +6.7 to -3.5), (3) Jan leading indicators (expected -0.2%, Dec -0.2%), (4) the Treasury's auction of $7 billion of 30-year TIPS, (5) San Francisco Fed President John Williams' speech on the economic outlook at an event in Los Angeles, and (6) EIA Weekly Petroleum Status Report.

There are 20 of the S&P 500 companies that report earnings today with notable reports including: Wal-Mart (consensus $1.46), PG&E (0.44), Waste Management (0.8), Duke Energy (0.91), Nordstrom (1.21), Applied Materials (0.26), Fluor (0.93).

U.S. IPO's scheduled to price today: none.

Equity conferences during the remainder of this week include: none.

OVERNIGHT U.S. STOCK MOVERS

NVIDIA (NVDA +2.48%) jumped nearly 8% in pre-market trading after it reported Q4 adjusted EPS of 52 cents, higher than consensus of 43 cents.

Wal-Mart (WMT +0.32%) slid 3% in pre-market tradng after it reported Q4 revenue of $129.7 billion, below consensus of $130.6 billion, and cut its yearly sales forecast to "relatively flat" from a previous view of up 3%-4%.

Brocade Communications Systems (BRCD +3.02%) rallied over 5% in after-hours trading after it reported Q1 adjusted EPS of 29 cents, above consensus of 24 cents.

Williams Cos. (WMB +4.53%) lost over 2% in after-hours trading after it reported Q4 adjusted EPS continuing operations of 1 cent, weaker than consensus of 27 cents.

Intercept Pharmaceuticals (ICPT +5.42%) rose over 5% in after-hours trading after departing CFO Barbara Duncan said she will delay her departure date of June 30 if no successor is in office by that time.

CF Industries (CF +1.80%) fell over 4% in after-hours trading after it reported Q4 adjusted EPS of 76 cents, below consensus of 82 cents.

Synopsys (SNPS +1.51%) climbed 6% in after-hours trading after it reported Q1 adjusted EPS of 68 cents, above consensus of 62 cents and then raised guidance on Q2 adjusted EPS to 78 cents-81 cents, above consensus of 70 cents.

Marriott International (MAR +2.49%) dropped over 2% in after-hours trading after it lowered guidance on Q1 EPS to 81 cents-85 cents, weaker than consensus of 89 cents.

Capital One Financial (COF +1.51%) gained over 1% in after-hours trading after it said its board authorized an additional $300 million to its stock buyback plan.

ARRIS International PLC (ARRS +2.11%) dropped 5% in after-hours trading after it said it sees Q1 adjusted EPS of 37 cents-42 cents, below consensus of 53 cents.

Tyler Technologies (TYL +3.47%) slip nearly 8% in after-hours trading after it reported Q4 adjusted EPS of 59 cents, below consensus of 66 cents, and then lowered guidance on fiscal 2016 adjusted EPS to $3.33-$3.45, below consensus of $3.55.

Jack in the Box (JACK +2.68%) tumbled 20% in pre-market trading after it reported Q1 adjusted EPS of 93 cents, below consensus of $1.03.

Lattice Semiconductor (LSCC unch) slid over 2% in after-hours trading after it reported Q4 revenue of $101.3 million, below consensus of $110.3 million.

Aerie Pharmaceuticals (AERI +6.46%) jumped 15% in after-hours trading after it reported successful 12-month safety results in its Phase 3 trial for its Rhopressa once-daily eye drop for its ability to lower intraocular pressure in patients with glaucoma or ocular hypertension.

Ingram Micro (IM +0.78%) surged over 20% in after-hours trading after Tianjin Tianhai bought the company for $6 billion or $38.90 a share.

MARKET COMMENTS

Mar E-mini S&Ps (ESH16 +0.42%) this morning are up +7.00 points (+0.36%) at a 2-week high. Wednesday's closes: S&P 500 +1.65%, Dow Jones +1.59%, Nasdaq +2.31%. The S&P 500 on Wednesday climbed to a 2-week high and closed higher on a rally in bank stocks and retailers that had been beaten down to start the year, the +0.5% increase in U.S. Jan manufacturing production (stronger than expectations of +0.2% and the largest increase in 6 months), and the +5% jump in crude oil, which sparked a rally in energy producer stocks.

Mar 10-year T-notes (ZNH16 -0.02%) this morning are down -1 tick. Wednesday's closes: TYH6 -15.00, FVH6 -7.50. Mar T-notes on Wednesday dropped to a 1-week low and closed lower on reduced safe-haven demand with the rally in the S&P 500 to a 2-week high, the larger-than-expected increase in U.S. Jan PPI, and the stronger-than-expected U.S. Jan manufacturing and industrial production reports.

The dollar index (DXY00 +0.12%) this morning is up +0.099 (+0.10%). EUR/USD (^EURUSD) is down -0.0031 (-0.28%). USD/JPY (^USDJPY) is down -0.26 (-0.23%). Wednesday's closes: Dollar Index +0.082 (-0.08%), EUR/USD -0.0016 (-0.14%), USD/JPY +0.03 (+0.03%). The dollar index on Wednesday closed lower on the rally in crude oil that benefited the oil-exporting currencies of Russia and Canada as the Russian ruble rallied to a 2-week high and the Canadian dollar climbed to a 1-week high against the U.S. dollar. The dollar was also undercut by the minutes of the Jan 26-27 FOMC meeting that stated policy makers saw increased downside risks, which may keep the Fed from additional rate hikes.

Mar WTI crude (CLH16 +3.03%) this morning is up +75 cents (+2.45%) and Mar gasoline (RBH16 +1.24%) is up +0.0092 (+0.92%). Wednesday's closes: CLH6 +1.62 (+5.58%), RBH6 +0.0325 (+3.35%). Mar crude and gasoline on Wednesday closed higher on comments from Iran's Oil Minister Bijan Zanganeh who said that Iran supports cooperation between OPEC and non-OPEC countries and supports an accord by Saudi Arabia and Russia to cap their crude output at Jan levels. Mar crude oil was also boosted by signs of strength in the U.S. economy that is positive for energy demand after U.S. Jan manufacturing production rose +0.5%, the most in 6 months.

(Click on image to enlarge)

Disclosure: None.