Morning Call For February 10, 2016

OVERNIGHT MARKETS AND NEWS

March E-mini S&Ps (ESH16 +1.01%) are up +1.03% and European stocks are up +2.67% as crude oil (CLH16 +2.18%) rallied +1.65% and bank stocks climbed. Bank of America, Citigroup and Morgan Stanley were all up at least 1.5% in pre-market trading ahead of Fed Chair Yellen's testimony on the economy to the House Financial Services Committee later this morning. Technology stocks are also higher, as Amazon.com, Facebook and Netflix were all up at least 2% in pre-market trading. European bank stocks also rallied to lead European stocks higher with Commerzbank AG up over 8% and Deutsche Bank AG surged 13% on reports that Germany's biggest bank was considering a share buyback, which eased concern about its funds. Asian stocks settled lower: Japan -2.31%, Australia -1.17%, Singapore -1.57%, India -1.09%. Hong Kong, China, Taiwan and South Korea were all closed for holiday. Japan's Nikkei Stock Index tumbled to a 1-1/4 year low as strength in the yen undercut exporter stocks along with concern that margin calls were generating forced selling of stocks.

The dollar index (DXY00 +0.06%) is up +0.07%. EUR/USD (^EURUSD) is down -0.34%. USD/JPY (^USDJPY) is down -0.11%.

Mar T-note prices (ZNH16 -0.18%) are down -7.5 ticks.

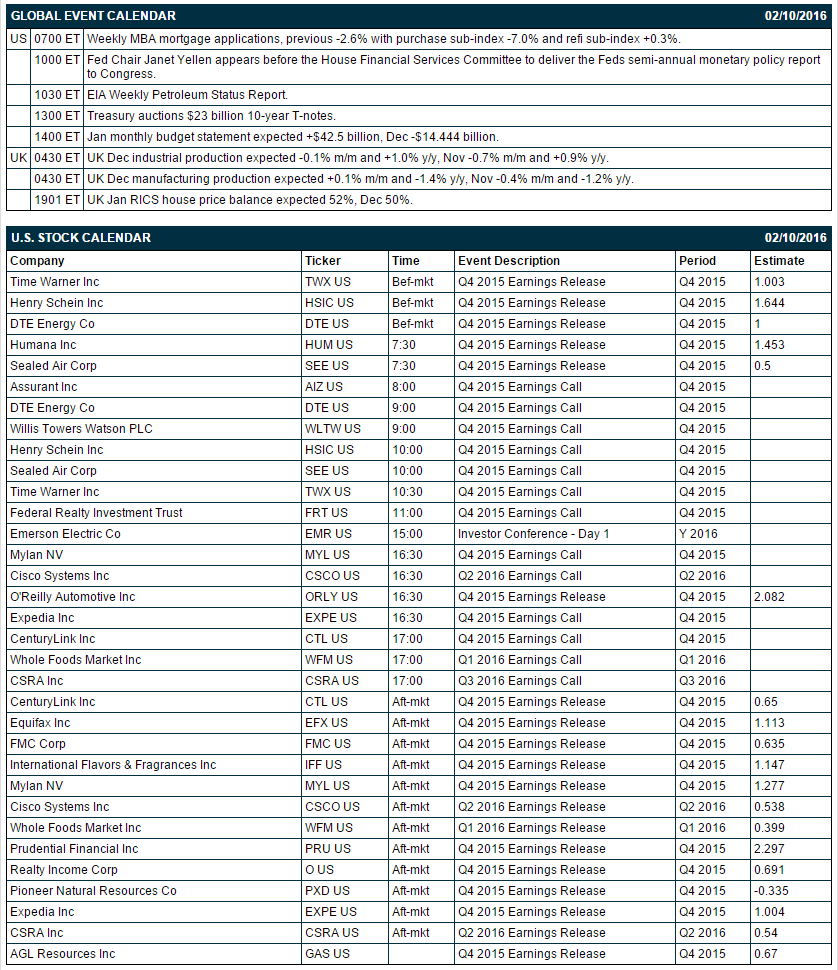

UK Dec industrial production fell -1.1% m/m, weaker than expectations of -0.1% m/m and the largest monthly decline in 3-1/4 years. Dec manufacturing production unexpectedly fell -0.2% m/m, weaker than expectations of +0.1% m/m and the third consecutive decline.

U.S. STOCK PREVIEW

Key U.S. news today includes: (1) weekly MBA mortgage applications (previous -2.6% with purchase sub-index -7.0% and refi sub-index +0.3%), (2) Fed Chair Janet Yellen's testimony before the House Financial Services Committee to deliver the Fed’s semi-annual monetary policy report to Congress, (3) the Treasury's auction of $23 billion of 10-year T-notes, and (4) Jan monthly budget statement (expected +$10.1 billion, Dec -$14.444 billion).

There are 19 of the S&P 500 companies that report earnings today with notable reports including: Cisco (consensus $0.54), Time Warner (1.00), Humana (1.45), Whole Foods (0.40), Expedia (1.00), Prudential Financial (2.30).

U.S. IPO's scheduled to price today: Avexis (AVXS), Proteostasis Therapeutics (PTI), Advanced Disposal Services (ADSW).

Equity conferences during the remainder of this week include: Credit Suisse Financial Services Forum on Tue-Wed, Stifel Nicolaus Transportation and Logistics Conference on Tue-Wed, Goldman Sachs Technology and Internet Conference on Tue-Thu, Bank Of America Merrill Lynch Insurance Conference on Wed-Thu, BB&T Capital Markets Transportation Services Conference on Wed-Thu, Leerink Partners Global Health Care Conference on Wed-Thu, Morgan Stanley Chemicals Corporate Access Day on Thu.

OVERNIGHT U.S. STOCK MOVERS

Time Warner (TWX -6.08%) reported Q4 EPS of $1.06, higher than consensus of $1.00.

Dean Foods (DF +0.26%) was upgraded to 'Buy' from 'Hold' at BB&T with a price target of $22.

Hess Corp. (HES -0.74%) was upgraded to 'Conviction Buy' from 'Hold' at Goldman Sachs.

Disney (DIS +0.22%) fell over 3% in pre-market trading after it reported Q1 adjusted EPS of $1.63, above consensus of $1.45, but reported a -6%decline in networks operating income for Q1, driven by a decline in subscribers from ESPN and lower advertising revenue from A&E.

Akamai (AKAM -3.44%) surged over 12% in after-hours trading after it reported Q4 adjusted EPS of 72 cents, higher than consensus of 62 cents, and then said its board authorized a new $1 billion share buyback plan.

Seattle Genetics (SGEN -1.06%) slid over 4% in after-hours trading after it lowered guidance on 2016 Adcetris sales to $255 million-$275 million, below consensus of $291.3 million.

Nuance Communications (NUAN -1.40%) rose nearly 7% in after-hours trading after it reported Q1 adjusted EPS of 36 cents, higher than consensus of 33 cents.

Paycom Software (PAYC -7.18%) jumped over 10% in after-hours trading after it reported Q4 adjusted EPS of 10 cents, higher than consensus of 8 cents, and then raised guidance on Q1 revenue to $82 million-$84 million, above consensus of $74.6 million.

Computer Sciences (CSC +0.33%) reported Q3 adjusted EPS continuing operations of 71 cents, better than consensus of 68 cents.

SolarCity (SCTY -5.69%) slumped 30% in after-hours trading after it lowered guidance on Q1 adjusted EPS to a loss of -$2.55 to -$2.65, a much wider loss than expectations of -$2.06.

Berkshire Partners reported a 10.4% stake in Mattress Firm (MFRM -4.08%) .

Empire District Electric (EDE +0.57%) jumped nearly 15% in after-hours trading after Algonquin Power & Utilities acquired the company for $2.4 billion.

Standard & Poor's cut the credit rating of Chesapeake Energy (CHK -4.41%) by one level to ccc, saying its debt is "unsustainable."

MARKET COMMENTS

Mar E-mini S&Ps (ESH16 +1.01%) this morning are up +19.00 points (+1.03%). Tuesday's closes: S&P 500 -.07%, Dow Jones -0.08%, Nasdaq -0.32%. The S&P 500 on Tuesday closed lower on negative carryover from a fall in European stocks to a 2-1/3 year low, a sell-off in bank stocks on concern the recent plunge in crude prices will force some oil producers and oil service companies into default, and concern that the global economic slowdown may deepen after German Dec industrial production unexpectedly fell -1.2% m/m, the biggest decline in 16 months. Losses were limited after the U.S. Dec JOLTS job openings unexpectedly rose +261,000 to 5.607 million, stronger than expectations of -18,000 to 5.413 million and the most in 5 months.

Mar 10-year T-notes (ZNH16 -0.18%) this morning are down -7.5 ticks. Tuesday's closes: TYH6 +0.50, FVH6 -0.75. Mar T-notes on Tuesday posted a new contract high but fell back and closed little changed. T-notes found support from increased safe-haven demand for T-notes as stocks prices declined and from reduced inflation expectations as the 10-year breakeven inflation expectations rate fell to a 6-3/4 year low. T-notes fell back from their best levels after the U.S. Dec JOLTS job openings unexpectedly rose to the highest in 5 months, a sign of labor market strength.

The dollar index (DXY00 +0.06%) this morning is up +0.069 (+0.07%). EUR/USD (^EURUSD) is down -0.0038 (-0.34%). USD/JPY (^USDJPY) is down-0.13 (-0.11%). Tuesday's closes: Dollar Index -0.499 (-0.52%), EUR/USD +0.010 (+0.89), USD/JPY -0.74 (-0.64%). The dollar index on Tuesday sold off to a 3-1/2 month low and closed lower on weakness in USD/JPY which plunged to a 14-3/4 month low a fall in global stocks fueled safe-haven buying of the yen, and on speculation that the slide in global equity markets will keep the Fed from additional interest rate increases.

Mar crude (CLH16 +2.18%) this morning is up +46 cents (+1.65%) and Mar gasoline (RBH16 +2.57%) is up +0.0186 (+2.07%). Tuesday's closes: CLH6-1.75 (-5.89%), RBH6 -0.0486 (-5.08%). Mar crude oil and gasoline on Tuesday closed sharply lower with Mar crude at a 2-week low and Mar gasoline at a 7-year low. Crude oil prices were undercut by the IEA's cut in its 2016 global crude oil demand forecast to 95.6 million bpd from last month's forecast of 95.7 million bpd, and by expectations for Wednesday's weekly EIA crude inventories to increase by +3.2 million bbl. Energy prices recovered from their worst levels after the dollar index slid to a 3-1/2 month low.

Disclosure: None.