Morning Call For August 25, 2016

OVERNIGHT MARKETS AND NEWS

Sep E-mini S&Ps (ESU16 -0.24%) are down -0.21% and European stocks are down -0.86% as fallout concerns from Brexit resurfaced after German Aug IFO business sentiment unexpectedly fell to the lowest in 6 months. Long liquidation and position-squaring ahead of Fed Chair Yellen's speech Friday at the Fed's symposium in Jackson Hole, Wyoming, also weighed on equity prices. Technology shares are also weaker, led by a nearly 6% drop in HP Inc. after it forecast weaker-than-expected Q4 profit. Asian stocks settled mostly lower: Japan -0.25%, Hong Kong -0.03%, China -0.57%, Taiwan +1.09%, Australia -0.36%, Singapore +0.26%, South Korea -0.02%, India -0.80%. China's Shanghai Composite fell to a 1-1/2 week low, led by losses in property stocks, on concern the government will act to thwart speculative activity after people familiar with the matter said Shanghai authorities are planning to hold meetings to discuss ways to cool surging property prices.

The dollar index (DXY00 -0.10%) is down -0.16%. EUR/USD (^EURUSD) is up +0.24%. USD/JPY (^USDJPY) is down -0.04%.

Sep T-note prices (ZNU16 +0.02%) are up +2 ticks.

The German Aug IFO business climate unexpectedly fell -2.1 to 106.2, weaker than expectations of +0.2 to 108.5 and the lowest in 6 months.

U.S. STOCK PREVIEW

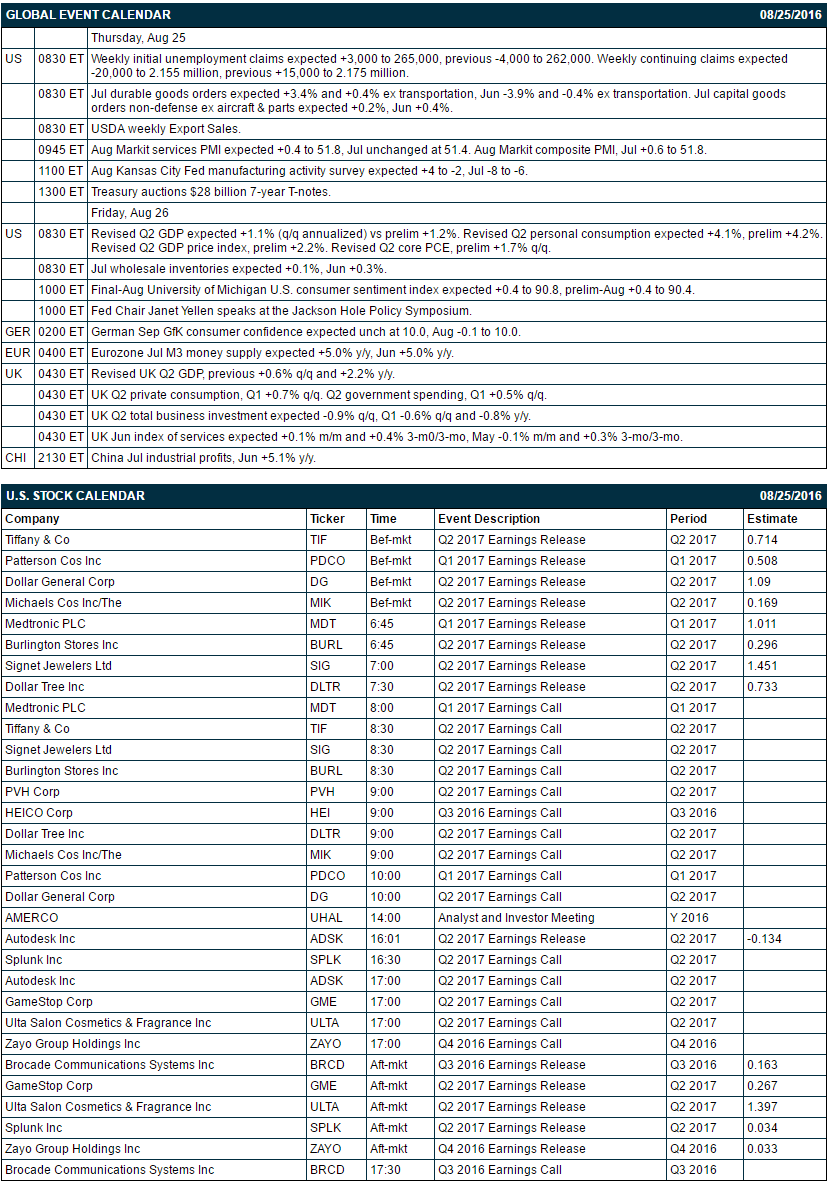

Key U.S. news today includes: (1) weekly initial unemployment claims (expected +3,000 to 265,000, previous -4,000 to 262,000) and continuing claims (expected -20,000 to 2.155 million, previous +15,000 to 2.175 million), (2) Jul durable goods orders (expected +3.4% and +0.4% ex transportation, Jun-3.9% and -0.4% ex transportation), (3) Aug Markit services PMI (expected +0.4 to 51.8, Jul unchanged at 51.4), (4) Aug Kansas City Fed manufacturing activity survey (expected +4 to -2, Jul -8 to -6), (5) the Treasury's auction of $28 billion of 7-year T-notes, and (6) USDA weekly Export Sales.

Russell 1000 companies that report earnings today: Tiffany (consensus $0.71), Patterson Cos (0.51), Dollar General (1.09), Michaels Cos (0.17), Medtronic (1.01), Burlington Stores (0.30), Signet Jewelers (1.45), Dollar Tree (0.73), Autodesk (-0.13), Brocade Communications Systems (0.16), Gamestop (0.27), Ulta Salon (1.40), Splunk (0.03), Zayo Group (0.03).

U.S. IPO's scheduled to price today: none.

Equity conferences during the remainder of this week: none.

OVERNIGHT U.S. STOCK MOVERS

Northrop Grumman (NOC -0.23%) was downgraded to 'Neutral' from 'Overweight' at JPMorgan Chase.

Sprint (S -0.49%) was downgraded to 'Underperform' from 'Neutral at Buckingham Research Group.

Express (EXPR -25.51%) lost over 1% in pre-market trading after it reported Q2 EPS of 13 cents, weaker than consensus of 17 cents, and then lowered guidance on full-year adjusted EPS to $1.00-$1.14 from a prior view of $1.41-$1.54.

Fiat Chrysler Automobiles NV (FCAU +0.44%) climbed 3% in pre-market trading after the Maeil Business newspaper reported that the vice chaorman of Samsung Electronics will fly to Italy to discuss a deal regarding auto-parts maker Magneti Marelli, an auto-parts unit of Fiat.

Netflix (NFLX -0.79%) was upgraded to 'Outperform' from 'Market Perform' at William Blair & Co.

HEICO (HEI +1.19%) rose over 1% in after-hours trading after it reported Q3 EPS of 62 cents, higher than consensus of 59 cents, and then said it sees 2016 net income of 13%-15%, up from a previous view of 12%-14%.

Cree (CREE -1.22%) was rated a new 'Buy' at Roth Capital with a price target of $34.

Workday (WDAY -0.38%) climbed nearly 11% in pre-market trading after it reported Q2 revenue of $377.7 million, above consensus of $372.8 million.

PVH Corp. (PVH -0.67%) gained over 1% in after-hours trading after it reported Q2 adjusted EPS of $1.47, higher than consensus of $1.29.

Electronics for Imaging (EFII -0.88%) was rated a new 'Buy' at Stifel with a 12-month target price of $53.

HP Inc. (HPQ -1.17%) fell nearly 6% in pre-market trading after it said it sees Q4 adjusted EPS from continuing operations of 34 cents-37 cents, weaker than consensus of 40 cents.

Guess? (GES -6.23%) surged 15% in after-hours trading after it reported Q2 adjusted EPS of 14 cents, much better than consensus of 6 cents, and then raised guidance on full-year adjusted EPS to 62 cents-75 cents from a May 25 view of 55 cents-75 cents.

Tilly's (TLYS +7.11%) jumped 10% in after-hours trading after it reported an unexpected Q2 EPS profit of 5 cents, better than consensus of a -5 cent loss.

Nymox Pharmaceutical Corp. (NYMX +83.13%) rallied over 10% in after-hours trading on carryover from Wednesday's announcement of positive results from a long-term Phase 3 study evaluating the drug fexapotide in men with enlarged prostates.

Ballard Power Systems (BLDP -4.33%) jumped 10% in after-hours trading after it said its Protonex unit was notified by the U.S. Commerce Department that its family of fuel cell propulsion systems are now designated EAR99 (Export Administration Regulations 99) compliant.

MARKET COMMENTS

Sep E-mini S&Ps (ESU16 -0.24%) this morning are down -4.50 points (-0.21%). Wednesday's closes: S&P 500 -0.52%, Dow Jones -0.35%, Nasdaq-0.73%. The S&P 500 on Wednesday closed lower on the -3.2% drop in U.S. Jul existing home sales to 5.39 million (a bigger decline than expectations of -1.1% to 5.51 million) and on the -2.70% plunge in crude oil prices that undercut energy producer stocks. In addition, there was a sell-off in drugmaker stocks, led by a 5% decline in Mylan NV, after it raised the price of its EpiPen by 400% and U.S. presidential candidate Clinton called it "outrageous," which fueled speculation that Ms. Clinton may take action against drugmakers if she is elected president.

Sep 10-year T-notes (ZNU16 +0.02%) this morning are up +2 ticks. Wednesday's closes: TYU6 unch, FVU6 +0.25. Sep T-notes on Wednesday closed unchanged. T-note prices were boosted by increased safe-haven demand with the slide in stocks and by the weaker-than-expected U.S. Jul existing home sales report of -3.2%. T-notes were undercut by supply pressures with this week's $101 billion T-note auction package.

The dollar index (DXY00 -0.10%) this morning is down -0.148 (-0.16%). EUR/USD (^EURUSD) is up +0.0027 (+0.24%). USD/JPY (^USDJPY) is down-0.04 (-0.04%). Wednesday's closes: Dollar index +0.247 (+0.26%), EUR/USD -0.0041 (-0.36%), USD/JPY +0.21 (+0.21%). The dollar index on Wednesday closed higher on speculation that Fed Chair Yellen may be hawkish and warn the markets of an impending Fed rate hike in her comments in Jackson Hole on Friday. The dollar was also boosted by weakness in the currencies of the crude-exporting countries of Russia and Canada after crude oil prices tumbled -2.70%.

Oct crude oil (CLV16 -0.62%) this morning is down -7 cents (-0.15%) and Oct gasoline (RBV16 -1.50%) is down -0.0174 (-1.23%). Wednesday's closes: CLV6 -1.30 (-2.70%), RBV6 -0.0049 (-0.35%). Oct crude oil and gasoline on Wednesday closed lower on doubts that OPEC will be able to agree on a production freeze at next month’s informal talks in Algiers after Iran said it hasn't decided if it will attend the meeting. In addition, the EIA report was bearish with the unexpected +2.5 million bbl increase in EIA crude inventories (vs expectations for -1.0 million bbl) and the +36,000 bbl increase in EIA gasoline supplies (vs expectations of -1.7 million bbl).

Disclosure: None.