Morning Call For August 10, 2015

OVERNIGHT MARKETS AND NEWS

September E-mini S&Ps (ESU15 +0.41%) are up +0.29% on increased M&A activity led by a 17% jump in Precision Castparts in pre-market trading on reports that Berkshire Hathaway was in talks to buy the company. European stocks are up +0.55%, led by a +1.2% increase in ASML Holding NV, which boosted technology stocks. Gains were limited as miners and energy producers declined on Chinese economic concerns after China Jul exports and imports fell more than expected. Asian stocks closed mostly higher: Japan +0.41, Hong Kong -0.13%, China +4.92%, Taiwan +0.29%, Australia +0.63%, South Korea -0.25%, India -0.48%. China's Shanghai Stock Composite jumped nearly 5% to a 2-week high on speculation that the government will boost stimulus measures to revive the economy after China Jul exports and imports fell more than expected and after China Jul producer prices fell by the most in 5-3/4 years. Chinese stocks also received a boost after the South China Morning Post reported that China's cabinet has approved plans to overhaul state-owned enterprises to allow mergers that may boost the economy.

The dollar index (DXY00 +0.15%) is up +0.32%. EUR/USD (^EURUSD) is down -0.34%. USD/JPY (^USDJPY) is up +0.39%.

Sep T-note prices (ZNU15 -0.11%) are down -6 ticks.

Eurozone Aug Sentix inventor confidence unexpectedly fell -0.1 to 18.4, weaker than expectations of +1.8 to 20.3.

China Jul CPI rose +1.6% y/y, more than expectations of +1.5% y/y and the most in 9 months. Jul PPI fell -5.4% y/y, weaker than expectations of -5.0%y/y and the fastest pace of decline in 5-3/4 years.

The China Jul trade balance unexpectedly shrank to a +$43.03 billion surplus from +$46.54 billion in Jun, when expectations were for a widening of the surplus to +$54.70 billion. Jul exports fell -8.3% y/y, more than expectations of -1.5% y/y and the biggest decline in 4 months. Jul imports fell -8.1% y/y, close to expectations of -8.0% y/y.

U.S. STOCK PREVIEW

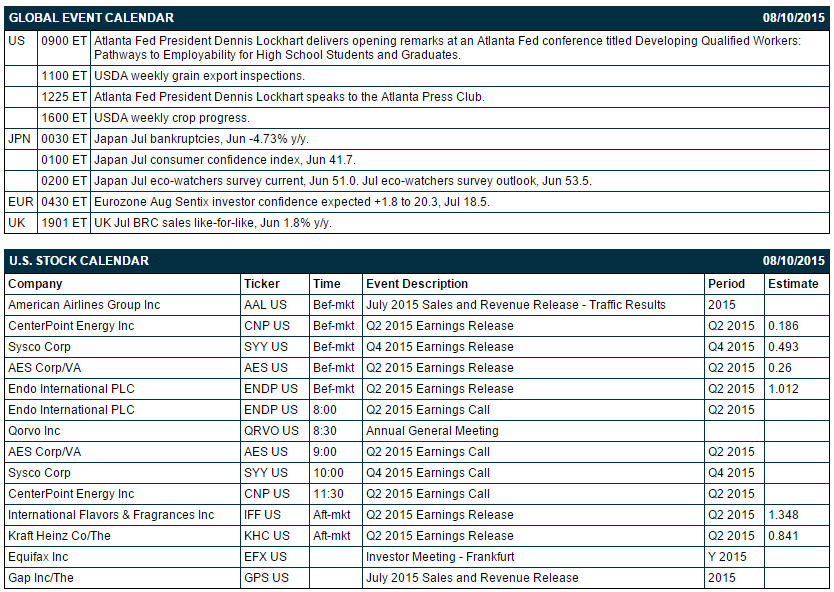

Key U.S. news today includes: (1) Atlanta Fed President Dennis Lockhart's opening remarks at an Atlanta Fed conference titled “Developing Qualified Workers: Pathways to Employability for High School Students and Graduates,” and (2) Atlanta Fed President Dennis Lockhart's speech to the Atlanta Press Club.

There are 6 of the S&P 500 companies that report earnings today: Kraft Heinz (consensus $0.84), CenterPoint Energy (0.19), Sysco (0.49), AES (0.26), Endo International (1.01), International Flavors & Fragrances (1.35).

U.S. IPO's scheduled to price today include: none.

Equity conferences this week include: Pacific Crest Global Technology Leadership Forum on Mon-Tue, Goldman Sachs Power, Utility, MLP & Pipeline Conference on Tue, J.P. Morgan Auto Conference on Tue-Wed, Oppenheimer Technology, Internet & Communications Conference on Tue-Wed, Jefferies Industrials Conference on Tue-Thu, Cowen and Co. Communications Infrastructure Summit on Wed, Canaccord Genuity Growth Conference on Wed-Thu, Nomura Media & Telecom Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

Precision Castparts (PCP +0.04%) surged 17% in pre-market trading on reports that Berkshire Hathaway was in talks to purchase the company for $37.2 billion.

Genesis Healthcare (GEN +4.04%) was upgraded to 'Outperform' from 'Sector Perform' at RBC Capital.

Transocean (RIG -1.95%) was upgraded to 'Hold' from 'Underperform' at Jefferies.

AES Corp. (AES +0.32%) reported Q2 adjusted EPS of 25 cents, below consensus of 27 cents.

Intuit (INTU +1.22%) was downgraded to 'Market Perform' from 'Outperform' at Raymond James.

Westlake Chemical (WLK -3.82%) was downgraded to 'Sell' from 'Neutral' at Goldman Sachs.

Piper Jaffray maintains an 'Overweight' rating on Electronic Arts (EA -0.88%) and raised its price target on the stock to $85 from $79.

Endo International PLC (ENDP +2.51%) reported Q2 EPS of $1.08, higher than consensus of $1.01.

Berkshire Hathaway (BRK-B +0.14%) fell over 1% in European trading after it reported Q2 operating EPS of $2,367, below consensus of $3,038.

JP Morgan Chase reported a 10.2% passive stake in Spark Energy (SPKE -0.97%) .

The New Home Company (NWHM -4.36%) was downgraded to 'Neutral' from 'Overweight' at JPMorgan Chase.

Lehigh Gas (LDP +0.04%) was downgraded to 'Perform' from 'Outperform' at Oppenheimer.

Intel reported a 5.0% passive stake in CareDx (CDNA +1.11%) .

Sands Capital reported a 10.9% passive stake in LendingClub (LC -0.78%) .

MARKET COMMENTS

Sep E-mini S&Ps (ESU15 +0.41%) this morning are up +6.00 points (+0.29%). Friday's closes: S&P 500 -0.29%, Dow Jones -0.27%, Nasdaq -0.19%. The S&P 500 on Friday fell to a 1-1/2 week low and closed lower on (1) increased fears of a Fed rate hike after the as-expected +215,000 increase in U.S. July payrolls, and (2) weakness in energy and commodity producers after crude oil fell to a 4-1/2 month low and copper plunged to a 6-year low.

Sep 10-year T-note prices (ZNU15 -0.11%) this morning are down -6 ticks. Friday's closes: TYU5 +14.0, FVU5 +4.50. Sep T-note prices on Friday closed higher on benign wage pressures after U.S. Jul average hourly earnings rose +2.1% y/y, less than expectations of +2.3% y/y, and on increased safe-haven demand for T-notes after the S&P 500 fell to a 1-1/2 week low.

The dollar index (DXY00 +0.15%) this morning is up +0.314 (+0.32%). EUR/USD (^EURUSD) is down -0.0037 (-0.34%). USD/JPY (^USDJPY) is up +0.49 (+0.39%). Friday's closes: Dollar Index -0.270 (-0.28%), EUR/USD +0.00404 (+0.37%), USD/JPY -0.550 (-0.44%). The dollar index on Friday posted a 3-1/2 month high but gave up its gains and closed lower on pre-weekend long liquidation pressure. USD/JPY fell after the S&P 500 dropped to a 1-1/2 week low and boosted the safe-haven demand for the yen. The dollar index saw some early support on Friday on the July +215,000 U.S. payroll report, which was strong enough to allow the Fed to go through with a rate hike later this year.

Sep crude oil (CLU15 +0.39%) this morning is up +4 cents (+0.09%) and Sep gasoline (RBU15 +1.12%) is up +0.0206 (+1.27%). Friday's closes: CLU5-0.79 (-1.77%), RBU5 -0.0248 (-1.51%). Sep crude oil and gasoline on Friday closed lower with Sep crude at a 4-1/2 month low and Sep gasoline at a 5-1/2 month low. Negative factors included the early rally in the dollar index to a 3-1/2 month high and concern the U.S. supply glut will persist with U.S. crude inventories 94 million bbl above the 5-year seasonal average. Crude oil prices rebounded higher from the day's lows afer the dollar index moved lower.

Disclosure: None.