Why, after eight years of economic expansion, does inflation remain in the doldrums, presenting a real challenge to monetary policy? In an earlier blog, I looked at how the digital revolution cut the costs of manufacturing and also the delivery of services to the extent that this revolution thwarted any prospects of inflation accelerating. In this note, I report on recent research done by the Federal Reserve on spending patterns that keep inflation down [1]. In particular, the research delves into price data by spending categories that are relatively insensitive to overall economic growth. The researchers expect that the prices in these sectors will continue to hold inflation down indefinitely.

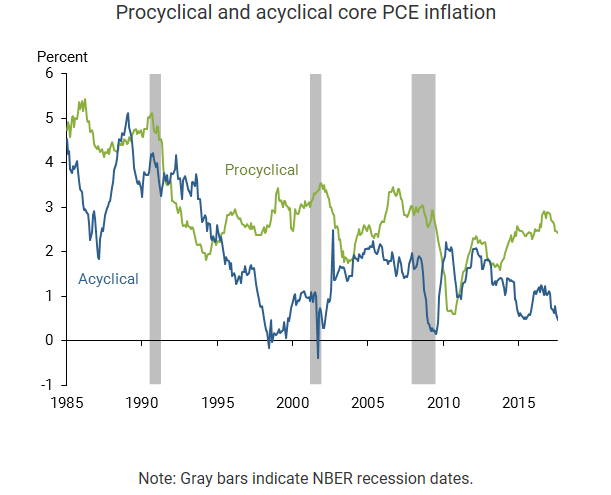

The researchers start out by looking at specific sectors to judge how sensitive they are to changes in the unemployment rate, a proxy for economic conditions. If inflation in a sector is sensitive to economic conditions then that sector can be classified as “procyclical”. Conversely, if the inflation rate in the sector does not move in relationship to changes in economic conditions, then the sector is categorized as “acyclical”. They found that procyclical sectors make up 42% of the PCE, the inflation measure used by the Federal Reserve. Procyclical sectors include housing, food services, and many non-durable goods. The acyclical sectors, the remaining 58%, include health-care, financial services, transportation and clothing among others. The indices for both price deflators are presented in the accompanying chart.

Procyclical and acyclical indices diverged in the late 1990s and again since 2014, both periods of relatively low inflation. The weakness in the overall PCE inflation measure is due, in large part, to the falling rate of inflation in the acyclical sectors.

Further research revealed that:

“persistently low acyclical inflation since the recession has been driven by the substantial drag from health-care services… were it not for this steady decline in health-care services inflation, core PCE inflation would have hovered above 2% for most of the post-recession period.”

This is a startling conclusion given that the Fed officials interpret inflation data as “noisy “and “transitory”. While lower health care costs are a welcome development, the downside is that inflation will likely continue to fall short of the 2% target.

[1] FRSF Economic Letter, “What’s Down with Inflation?”, T. Mahedy and A. Shapiro, November 27, 2017

Comments

Log in or sign up to join the conversation.