Mixed Signals In The Manufacturing PMIs

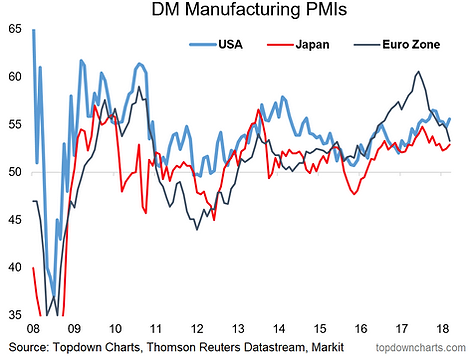

The September flash manufacturing PMIs from Markit brought with them some mixed signals on the path of developed economies. The composite flash PMI (calculated by us) was up +0.1 to 54.4, which came as a result of US rebounding +0.9pts to 55.6 and Japan up +0.4pts to 52.9, but Europe continuing its decline, -1.3pts to 53.3. The uptick in US and Japan is promising from a global macroeconomic cycle outlook, but the softening in Europe is a concern, and probably goes some way to explaining some of the performance differentials in global risk assets.

(Click on image to enlarge)

Looking again at the DM composite PMI vs US 10 year bond yield chart (this was a key chart in picking the surge in bond yields because a gap had previously opened between price and fundamentals)... At this point, the 10-year treasury yield has moved beyond where the DM composite PMI suggests it "should" be (although you get different answers on that if you use the ISM vs Markit PMIs). But I wonder if at this point maybe this time it's the bond market that has it right... in other words, the rise in Treasury yields could be reflecting greater optimism on the growth/inflation outlook.

(Click on image to enlarge)

Anyway, the main takeaways from the latest round of flash manufacturing PMIs are: 1. Global growth is not collapsing (Japan + US rebounding); 2. Global growth appears to become less synchronized, and divergent/asynchronous cyclical signals are becoming more apparent; .3. Overall it still justifies a bias to be long risk assets and short/underweight bonds.

For more and deeper insights on the global markets, good charts, and actionable investment ideas you may want to more