Meditative Monday Markets – Contemplating The Fed

It's the last week of summer.

That's something my kids are keenly aware of as they head back to high school. Turns out Jackie's(14) summer bucket list included a weekend at Martha's Vineyard and she was devastated to find out that telling me this on Thursday last week wasn't adequate notice to plan a trip for next weekend, even if I were so inclined.

The Fed schedules their Jackson Hole conference for the last week of summer because they know no one on Wall Street does anything until after Labor Day (9/5) so the purpose of the whole circus is to give us something to chew on over the holiday, when the G20 Meeting will be held in Hangzhou, China. As you can see from JackDamn's SPY chart, the market has been running hot all summer but we're having a lot of trouble at that top channel and there's very little support below 2,160 on the S&P all the way back to 2,100.

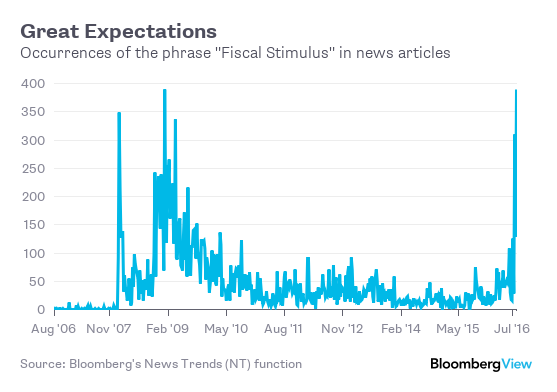

Hope, though, springs eternal into the fall as bullish investors are still salivating over the possibility (they think certainty) of another major round of fiscal stimulus and God help us all if the G20 disappoints on that front next weekend because the Fed certainly gave us no clear direction out of their meeting.

What Yellen said on Friday (key quote) was:

"In light of the continued solid performance of the labor market and our outlook for economic activity and inflation, I believe the case for an increase in the federal-funds rate has strengthened in recent months."

"I believe" is not the same as "we believe" and a divided Fed is what has given us this choppy summer trading pattern. Vice Chairman Fisher seemed to have more of the team spirit saying: "We should be on a program of gradual rate increases," though he added, "We can afford to be patient" when it comes to acting. The Fed Governors were all over the place in their statements, however but, generally, all hedged towards data-dependence:

- "If we had a lot of good news and we got into the September meeting and other people wanted to go, I could support that--but again I'm talking about one increase and no planned increases after that." - St. Louis Fed President James Bullard

- "The case for raising rates in the near term "has been strengthened." - Dallas Fed President Robert Kaplan

- "I see a gradual…upward pace in interest rates as being appropriate." As to when the Fed might raise rates next, she said, "I go into every meeting with an open mind." - Cleveland Fed President Loretta Mester

Yellen's own chart on rate outlook is sort of a joke as she says she sees rates coming in somewhere between 0 and 4.5% over the next two years, "depending on the data." Someone needs to inform Janet that companies and people like to PLAN for the future and those plans are much easier to make if we had some sort of indication of where rates would be in that future.

4.5% rate swings can break borrowers and lenders alike if the moves go against them yet the Fed likes to play this game of "openness" when all they actually open up is a ball of confusion. The bulls for their part, are just like children who have their hearts set on an expensive and unrealistic vacation – if they get a no from one parent, they go right to the other parent – in this case the G20 and, if the G20 fails to satisfy them, they'll run right back to the Fed, hoping to see what they want in the September meeting.

This kind of back and forth activity can go on for ages until the parents are willing to give the children a firm "no" and deal with the disappointment. For my part, I like to run the numbers with my kids to show them why doing certain things are unrealistic – in time and money, as I want them to grow up to be economically responsible citizens. John Hussman, in his Annual Report (thanks Winston) also ran the numbers and boy, are they disappointing:

"For stocks, our view is that the relevant statistic for the S&P 500 is not the current 2.2% dividend yield, but the roughly -26% decline that would be necessary to bring estimated prospective 10-year returns even to 5%; a figure that we view as rather minimal given cyclical equity market volatility. A market loss on the order of 40-55% would presently be required to bring prospective 10-year S&P 500 total returns into the 8-10% range that has always been reached or surpassed during the completion of every other market cycle across history".

The bulls want the market to go higher and Big Daddy Hussman is trying to tell them that higher is very unrealistic and, in fact, we've gone far too high already and they should expect a correction – not more of the same. Hussman is, of course, a market historian and this time may well be different but I, for one, would feel a whole lot better if the data would catch up to the valuations at some point, wouldn't you?

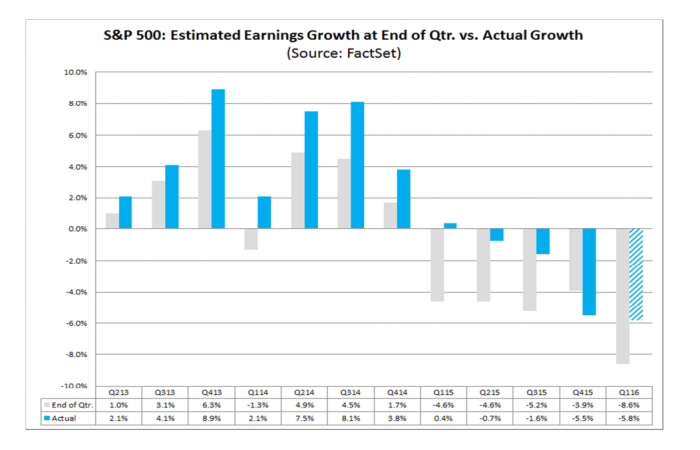

While 80% of the S&P 500 beat low expectations this quarter, only 55% actually managed to have better revenues than expected and, in large part, these "incredible" (as in "not credible") earnings beats stem from a combination of Non-GAAP Financial Reporting and Stock Buybacks and the whole thing unravels when you realize that, even with all these shenanigans, overall earnings are down 1.3% for the 6th CONSECUTIVE QUARTERLY DECLINE IN EARNINGS.

And how much are we being asked to pay for these ever-decreasing profits?

No wonder the markets are gyrating so wildly. Every once in a while, someone wakes up and actually looks at the numbers but this week is not one of those times because the G20 will FIX everything – or at least that's what I believe…

more