Mean Reverting Value With Material Growth Opportunities, Intevac

Intevac (IVAC) supports the electronic components industry with two business units; Thin-film equipment and Photonics.

The Thin film equipment division designs, manufacture, and services capital equipment that deposit thin films on the surface to produce magnetic disks for hard disk drives, centralized storage for cloud computing. Additionally, other applications and a key to material near-term growth include touch panels such as mobile phones front and back, notebooks, smartwatch, tablets, automotive monitors. Solar power industry benefits from the thin film equipment division by maximizing solar cell efficiency/lower cost per watt.

The Photonics division offers digital night-vision products and services to the defense industry. Specific products include night vision cameras, soldier night vision, and integrated night vision.

Management presented the below slide for their optimistic forecasts at the 19th Annual B. Riley FBR Investor Conference on May 24th, 2018.

Quarter 1 reported on 05/01/2018 was within expectations, revenues of $18 million and a loss of $0.23 per share. The short-term outlook is disappointing. But, medium-term and longer the future is positive with new products supported by patents and a growing pipeline. The second half of the fiscal year management expects positive operating results. Buying IVAC shares at today's valuation offers a sound opportunity. I will add additional shares if the stock continues to weaken.

Two new Board Members are Kevin Barber and Mark Popovich. They both have deep experience in the cell phone and advanced packaging markets. Their key role will advise on current pipeline and expected growth for mobile phones, touch panels, notebooks, smartwatch, tablets and automotive monitors.

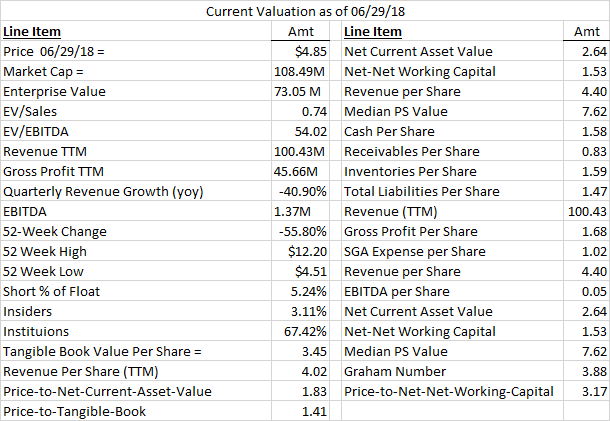

Current Valuation:

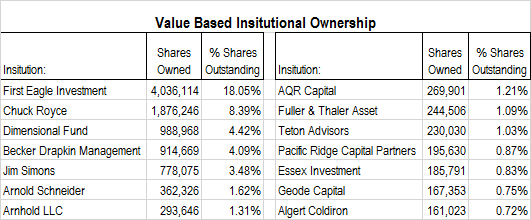

Value-Based low portfolio turnover institutions invested in IVAC

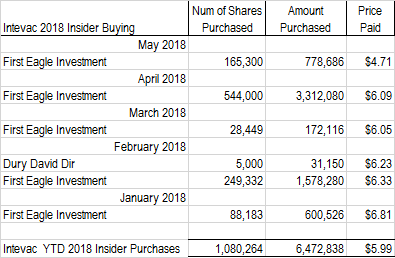

Insider Buying for YTD 2018

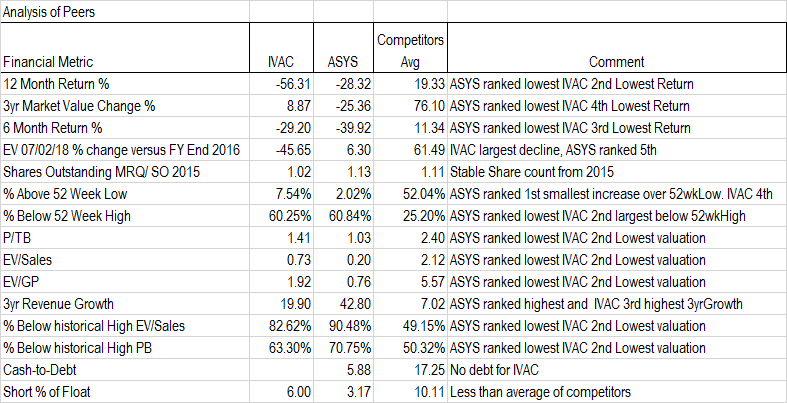

Relative Peer Valuation: The 14 peer companies (ASYS, KOPN, ACLS, CLFD, IVAC, AXTI, NPTN, EMAN, XCRA, CYBE, PRCP, COHU, NANO, ESIO)

used to evaluate compensation in the 05/16/18 proxy were also used for my relative valuation. These 14 companies were in the Scientific / Technical Instruments, Electronic Components, Semiconductor Equipment / Materials industries.

After an analysis of the 14 peer companies, I separated financial metrics for both IVAC and ASYS. I purchased IVAC along with ASYS as both value outliers.

Opportunities:

Mean reverting attributes such as -56.50% 12-month stock return for IVAC and -27.20% ASYS. IVAC enterprise value declined -45.65% from FY end 2016 to 07/02/18. ASYS increased +6.30% over the same period.

ASYS Median P/S is $12.10 versus the current price of $6.11. IVAC Median P/S is $7.62 versus a price of $4.85. EV/Sales and P/TB trade near historical lows. IVAC P/TB improved from 2016 ratio of 2.52 to its current value of 1.39, 44.84% improved valuation. ASYS P/TB was 1.26 for FY end 2016. This improved to 1.06 or 15.87 %. IVAC EV/Sales improved from 2016 balance of 1.68 to .73 or a 56.54% improved valuation. ASYS EV/Sales 1.26 for FY end 2016 improved to 1.06 or 47.36 %.

YTD IVAC material insider buying with no sales of $6,472,838 or 1,080,264 shares purchased at the average price of $5.99.

Value-based institution buying or holding IVAC shares such as activist Becker Drapkin Management, Royce, First Eagle, Simons, Tenton, and others.

A strong balance sheet with a P/NCAV 1.83 for IVAC, P/Networking capital = 1.53, gross profit per share of 1.68, cash per share of 1.58, no long-term debt and trading near 52 Week low.

Strong growth opportunities with new markets for display covers, solar, night vision.

Risks:

The main risk is that medium and long-term projection for display markets and night vision are not fully realized.