March US Soybean Stocks

Market Analysis

A larger-than-expected decline in the USDA’s Argentine monthly soybeans output, an adjustment of 7 mmt, and limited rainfall in this major competitor’s main central crop region has tried to counter a rise in the US old-crop ending soybean stocks earlier this month. The trade will note the USDA’s quarterly soybean stocks level on March 29, but the US prospective planting report being released the same day probably will have more impact on bean prices going forward.

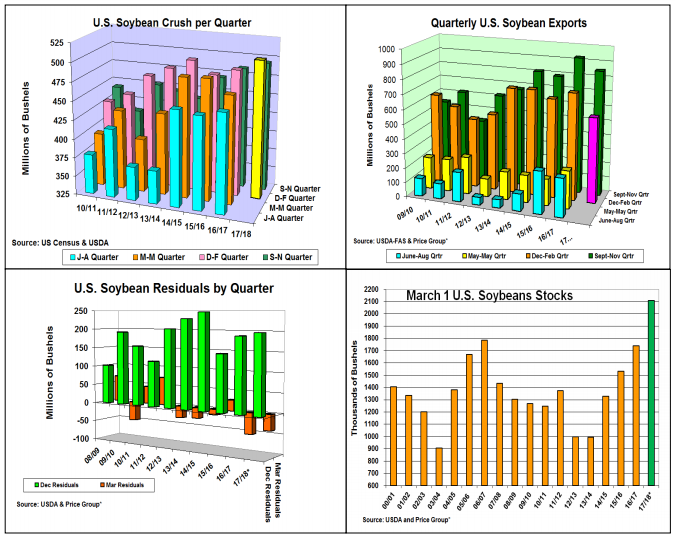

This year's strong US processing pace has been a talk of the domestic markets. Last week’s February US National Processor (NOPA) report revealed a 153.7 million bu. record which was 5.3 million above its previous monthly high in 2010. For the winter quarter, this year’s total crush is likely to be 514 million which pushed this year’s first half processing level 33 million above last year and to a new record for this domestic demand. This hasn’t been the case for soybean’s overseas demand. Until the past few weeks, US sales were struggling behind the seasonal pace to reach the USDA’s forecast. A dramatic 136 million jump in foreign purchases in past 2 weeks with Argentine crop ideas still being 2-4 mmt lower than USDA is a positive, but the US winter quarter shipments appear to be only 580 million bu. This leaves this year’s exports 225 behind last year’s first half shipments.

Despite this year's strong US crush demand, soybeans March 1 stocks will likely be about 2.11 billion bu., a record 2nd quarter stock level because of 2017’s record output. Last fall’s middle of the pack residual of 197 million bu. suggests this disappearance, which is a combination of export supplies in transit and soybeans moving to seed firms for processing, could shrink by 40 million bu. This stock report along with June’s quarterly supplies will help determine if the USDA will have to adjust last fall’s crop size to better reflect soybean’s ending stocks.

What’s Ahead

The USDA’s March 1 soybean stocks will be checked to see if the current crop size is on target or if it might be changing. This quarter’s residual vs. last fall’s 198 million bu. level will be the 1st look. 2018’s planting intentions maybe a bigger market mover that day if a higher than a 1 million acre jump in beans is reported. Hold old-crop sales at 90%, but move up Nov bean sales to 30-40% sold in $10.30-$10.40 range.

Disclaimer: The information contained in this report reflects the opinion of the author and should not be interpreted in any way to represent the thoughts of The PRICE Futures Group, any of its ...

more