FX Markets Turn To UK & US Inflation Data As Bond Bears Awaken

02/13 Tuesday | 09:30 GMT | GBP Consumer Price Index (JAN)

Inflation data is starting to come back into the spotlight as a significant influence for central banks in developed economies, and the Bank of England is no different in this regard. As such, unlike inflation reports in previous months, the upcoming data release should hold greater importance for the Sterling in the near-term. Consensus forecasts are calling to see price pressures to dip to -0.6% from +0.4% (m/m) and +2.9% from +3.0% (y/y). Conversely, Core CPI is expected to edge higher to +2.6% from +2.5% (y/y).

Just last week BOE policymakers warned that headline CPI could stay elevated prompting a faster pace of rates hikes. While the November rate hike was not the beginning of a rate hike cycle, inflation holding near +3% through early-2018 could very-well pull forward rate hike expectations from August 2018 to May 2018.

Pairs to Watch: EUR/GBP, GBP/JPY, GBP/USD

02/14 Wednesday | 13:30 GMT | USD Consumer Price Index (JAN)

According to a Bloomberg News survey, US consumer prices maintained their steady climb in January, due in at +0.3% from +0.1% (m/m) and +1.9% from +2.2% (y/y). The core readings should be similar, at +0.2% from +0.3% (m/m), and at +1.7% from +1.8% (y/y). These figures aggregately have started to steady near the Fed’s medium-term target, adding evidence to an already-convinced market that the Fed will hike rates in March. Given signs that wage growth is starting to perk back up and bond markets are responding in kind, the US CPI report on Wednesday could be the most important data release of the week. Expect the US Dollar to follow US Treasury yields around the data.

Pairs to Watch: DXY Index, EUR/USD, USD/JPY, Gold

02/14 Wednesday | 13:30 GMT | USD Advance Retail Sales (JAN)

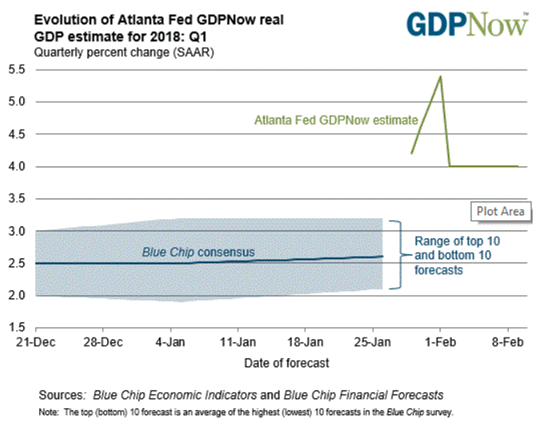

Consumption is the most important part of the US economy, generating nearly 70% of the headline GDP figure. The best monthly insight we have into consumption trends in the US might arguably be the Advance Retail Sales report. In January, according to a Bloomberg News survey, consumption was flat the headline Advance Retail Sales due in at +0.2% from +0.4% (m/m). The Retail Sales Control Group, the input used to calculate GDP, is due in at +0.4% from +0.3% (m/m). Based on the data received thus far about Q1’18, the Atlanta Fed GDPNow forecast is looking for growth near +4%.

Pairs to Watch: DXY Index, EUR/USD, USD/JPY, Gold

02/15 Thursday | 00:30 GMT | AUD Employment Change and Unemployment Rate (JAN)

Australian employment increased by +34.7K in December, and labor market data in general can be attributed as one of the main drivers of Australian Dollar strength over the past two months. With the unemployment rate steady around 5.5%, the Reserve Bank of Australia is probably looking for nothing more than signs of stable growth rather than another blowout print to keep their optimism about the labor market intact. Current forecasts call for +15.0K jobs to have been added last month and for the unemployment rate to have held at 5.5%, in what should amount to another strong labor report overall.

But despite the steadily improving state of the labor market, uneven economic data appears to be a wrinkle in the outlook for the RBA, which continues to note that real wage growth trends aren’t strong enough to provoke a rate hike any time soon. Interest rate expectations (per overnight index swaps) show July 2018 as the most likely period for the next rate hike; this is only one month sooner than what was being priced in back in October 2017.