Don’t Fear The Yield Curve?

In July of this year, James McCusker penned an article entitled “Don’t Fear The Yield Curve” in which he stated:

“There are always a lot of things to worry about in our economy — short range and long range. The yield curve, however. isn’t one of them. It just shows that some other people are worried, too. It doesn’t mean that they are right.”

I didn’t think much of the article at the time as it was an outlier. However, now, given the yield curve continues to trail lower, despite the many calls of “bond bears” swearing rates are going to rise, the number of voices in the “this time is different” camp has grown.

“Contrary to what many people think, inverted yield curves don’t always sound the alarm to sell. In fact, looking at the past five recessions, the S&P 500 didn’t peak for more than 19 months on average after the yield curve inverted, along the way adding more than 22% on average at the peak,” – Ryan Detrick, LPL

“In fact, an inversion is often a buying opportunity. During each of the past seven economic cycles, the S&P 500 has gained in the six-months before a yield-curve inversion.” Tony Dwyer, analyst at Canaccord Genuity.

First, the yield curve is simply the difference in the yields of different maturities of bonds. However, in this particular case, we are discussing the difference between the 2-year and the 10-year rate on U.S. Treasury bonds.

Historically speaking, the yield curve has been a consistent predictor of weaker economic times in the U.S. As James noted:

“The yield curve itself does not present a threat to the U.S. economy, but it does reflect a change in bond investor expectations about Federal Reserve actions and about the durability of our current economic expansion.”

Importantly, yield curves, like valuations, are “terrible” with respect to the “timing” of the economic slowdown and/or the impact to the financial markets. So, the longer the economy and markets continue to grow without an event, or sign of weakness, investors begin to dismiss the indicator under the premise “this time is different.”

James did hit on an important point but misses the mark.

“Much of our economy relies on debt, and the so-called ‘entitlement’ sector of government spending is dependent on investors parting with cash to purchase trillions of dollars of the federal government’s debt. That means that the investor expectations reflected in the yield curve have some weight. However, it is good to remember that the negative yield curve may simply be the result of a delayed reaction of long-term interest rates to the economy’s expansion. If long-term rates were to rise, the inversion of the yield curve would disappear.”

He is right that we are in a debt-driven economy. Corporate, household, margin, student, and government debt are at all- time highs. That debt has a cost. It must be serviced. Therefore, as rates rise, the cost of servicing rises commensurately. This is particularly the case with variable rate, credit card, and other debt which are tied directly to short-term rates which is impacted by changes in the overnight lending rates (aka Fed monetary policy).

As rates rise on the short-end, and as expected rates of future returns fall, money is shifted toward the “safety” of longer-dated U.S. Treasuries not only by domestic investors, but also foreign investors which are seeking safety from a stronger dollar, weaker economic growth, or reduced financial market expectations.

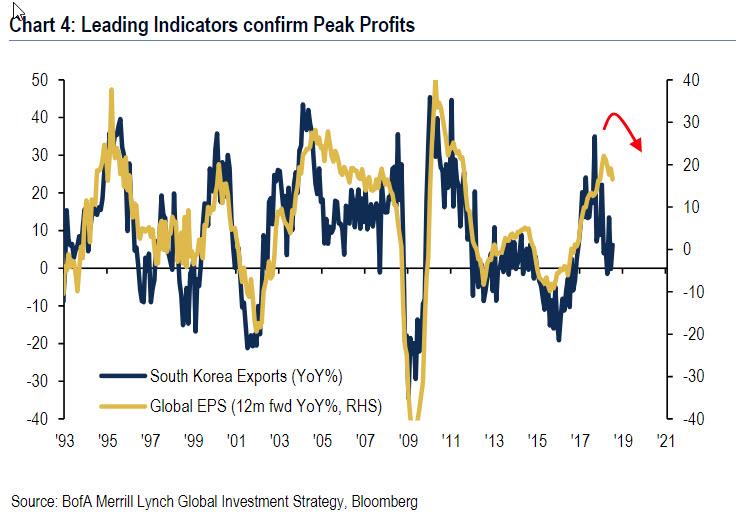

While there are many calls to ignore the yield curve, some of the most economically sensitive commodities. like Copper, are providing a cause for concern. Per Jesse Colombo:

“Copper, which is known as “the metal with a PhD in economics” due to its historic tendency to lead the global economy, is down nearly 4 percent today alone and 22 percent since early-June. Copper’s bear market of the past couple of months is worrisome because it signals that a global economic slowdown is likely ahead.”

(Click on image to enlarge)

Even exports from South Korea, which acts as a leading indicator of economic activity has turned sharply lower as well.

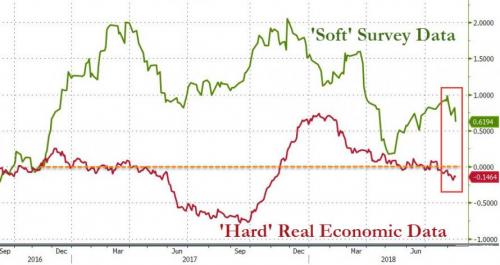

While “sentiment” data was previously extremely elevated over “hopes” that “Trumponics” would create an broad-based economic surge, as noted recently, such has not been the case and “sentiment” is now catching “down” with reality.

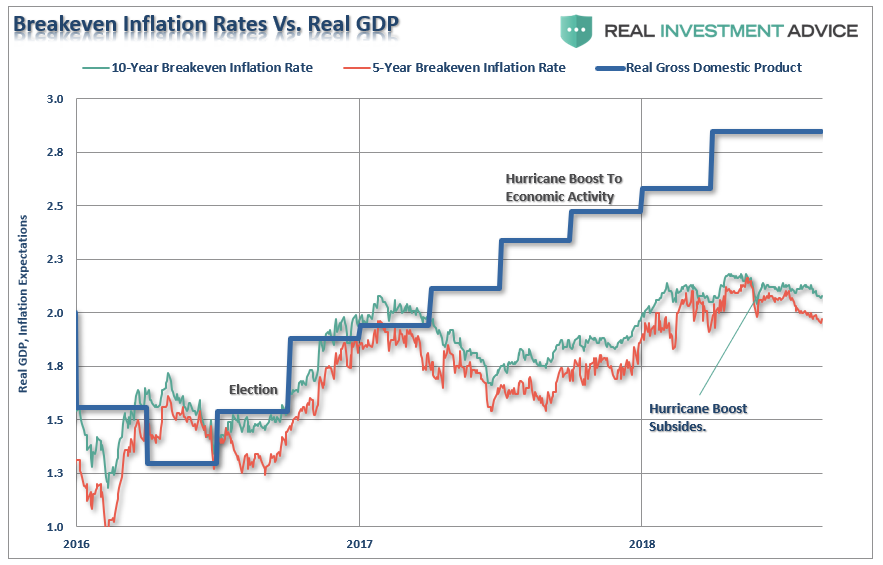

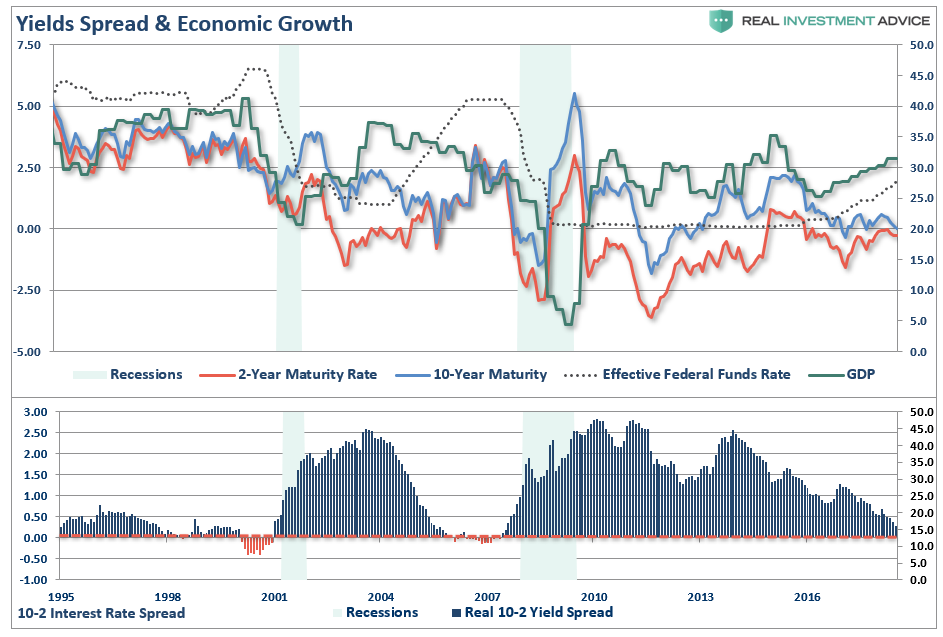

Of course, one really needs to look no further than the bond market which is also screaming the Fed is once again, as they always have, making a monetary policy mistake. The chart below shows, GDP as compared to both the 5- and 10-year inflation “breakeven” rates. As noted, there was a significant boost to economic activity following three massive hurricanes and two major wildfires in 2017. That bump to activity only served to “pull forward” future economic activity, increasing short-term inflationary pressures, which are now beginning to subside.

(Click on image to enlarge)

The message is quite simple.

The spread between the 10-year and 2-year Treasury rates, historically a good predictor of economic recessions, is also suggesting the Fed may be missing the bigger picture in their quest to normalize monetary policy. While not inverted as of yet, the trend of the spread is clearly warning the economy is much weaker than the Fed is suggesting.(The boosts to economic growth are now all beginning to fade and the 2nd-derivative of growth will begin to become more problematic starting in Q3)

(Click on image to enlarge)

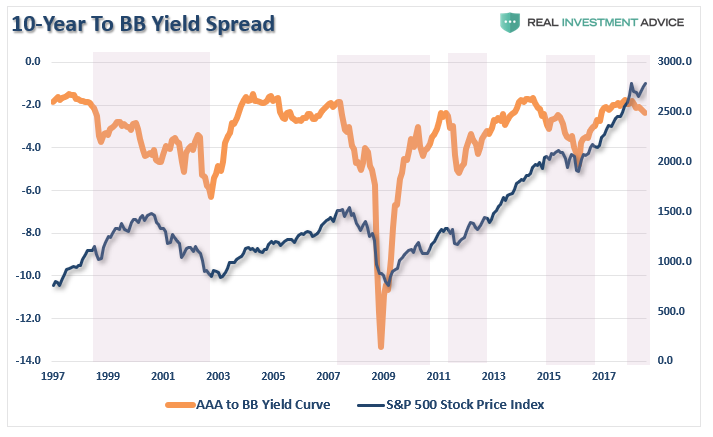

Furthermore, the AAA-Junk yield curve is also beginning to suggest problems for companies which have binged on debt issuance to support share buybacks over the last decade.

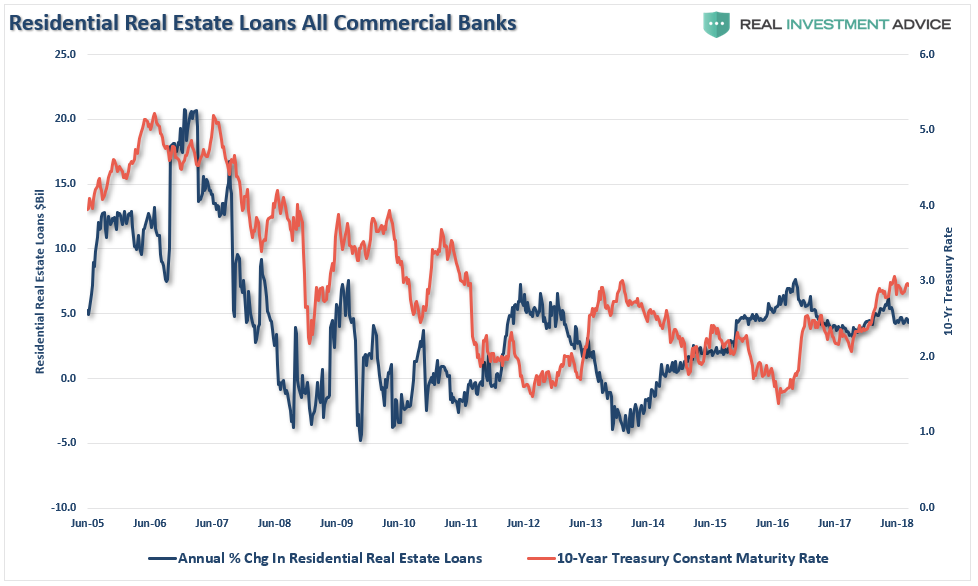

The annual rate of change for bank loans and leases as well has residential homes loans have all started declined as higher rates are crimping demand.

(Click on image to enlarge)

While none of this suggests a problem is imminent, nor does it RULE OUT higher highs in the markets first, there is mounting evidence the Fed is headed towards making another mistake in their long line of creating “boom/bust” cycles.

(Click on image to enlarge)

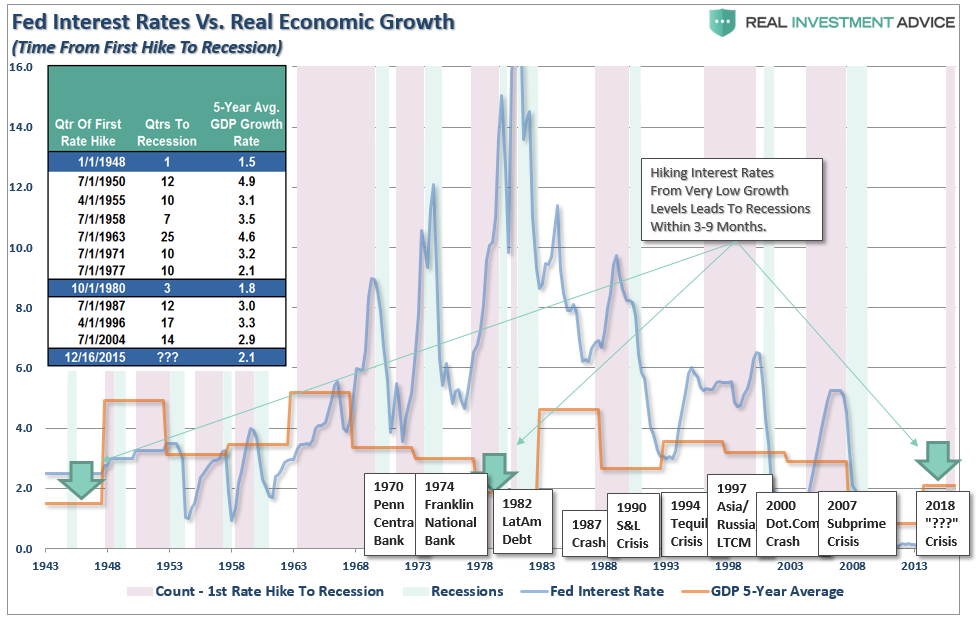

Looking back through history, the evidence is quite compelling that from the time the first rate hike is induced into the system, it has started the countdown to the next recession.

The Federal Reserve is quickly becoming trapped by its own “data-dependent” analysis. Despite ongoing commentary of improving labor markets and economic growth, their own indicators have been suggesting something very different. This is why the scrapped their Labor Market Conditions Index and are now trying to come up with a “new and improved” yield curve to support their narrative.

Tightening monetary policy further will simply accelerate the time frame to the onset of the next recession. In fact, there have been absolutely ZERO times in history that the Federal Reserve has begun an interest-rate hiking campaign that has not eventually led to a negative outcome.

The only question is the timing.

It is unlikely this time is different. There are too many indicators already suggesting higher rates are impacting interest rate sensitive, and economically important, areas of the economy. The only issue is when investors recognize the obvious and sell in the anticipation of a market decline.

Believing that investors will simply ignore the weight of evidence to contrary in the “hopes” this “might” be different this time is not a good bet. The yield curve is clearly sending a message that shouldn’t be ignored and it is a good bet that “risk-based” investors will likely act sooner rather than later. Of course, it is simply the contraction in liquidity that causes the decline which will eventually exacerbate the economic contraction. Importantly, since recessions are only identified in hindsight when current data is negatively revised in the future, it won’t become “obvious” the yield curve was sending the correct message until far too late to be useful.

While it is unwise to use the “yield curve” as a “market timing” tool, it is just as unwise to completely dismiss the message it is currently sending.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Real Investment Advice is expressly disclaims all liability in ...

more