Despite Lower World Output, Stagnant Demand Keeps Wheat Stocks High

Market Analysis

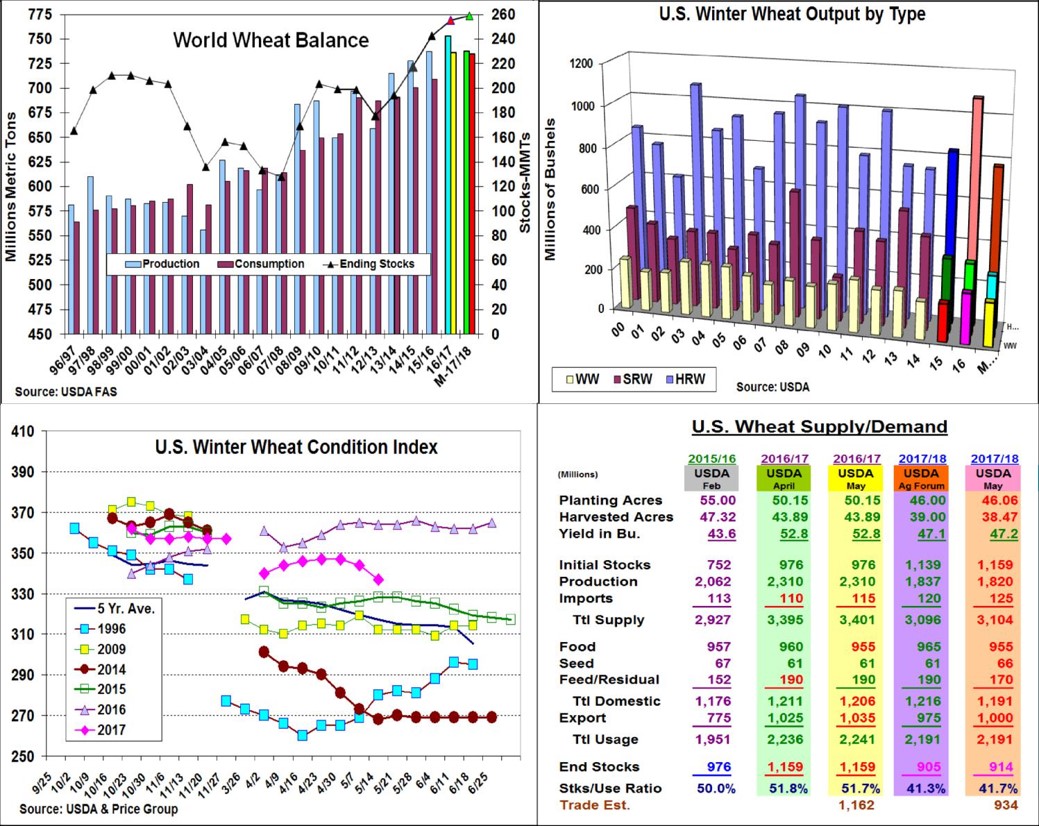

This month’s World numbers provided the wheat surprise from the USDA last week. As suspected, the Ag Department reduced its world production outlook by 15 mmt to 738 mmt with 5 out of top 7 world wheat export competitors likely decreasing their output while the EU and Argentina are projected to have modest increases in 2017. This year’s US crop is also forecast to decline by 13 mmt, but China, India and others are projected to in-crease. The USDA’s surprise came when they didn’t in-crease their total 2017/18 world demand leaving it un-changed at 735 vs. expectations of a modest 1% in-crease from much of the trade. Overall, the USDA’s world carryover forecast rose by 3 mmt to 258 mmt vs. ideas of a 6-10 mmt drop in the world wheat stocks for upcoming year leaving a negative cloud over the market.

Given the extremely unusual freeze across NC Kansas and hefty snows across the W. Plains that reduced the field samples from the second day of the Kansas by one third, the USDA’s first winter wheat crop level was lower than the trade’s average estimate, but left much unknown about the final US crop size. This year’s hard red output has taken the blunt of 2017’s reduced output from 1.081 billion bu to 737 million because of reduced Plains seedings. Hefty rains across the Delta and the Southern Mid-west this spring prompted May’s Soft red output to be trimmed from 345 million to 297 million this year. Cold, wet weather also shaved the USDA’s PNW white wheat outlook by 33 million to 212 million this month. Given the recent downtrend of US wheat condition index from 347 to 337 (very poor and poor picking up 2% while good and excellent losing 2 and 1% over the past two weeks), the US winter wheat crop remains vulnerable given the cur-rent 90 degree Plains heat. This month’s 2017/18 balance sheet already has tightened US stocks by 245 mil-lion bu. despite using an unchanged US demand outlook.

(Click on image to enlarge)

What’s Ahead

Given this year’s unknowns concerning tiller counts and grain test weights, this year’s winter wheat crop could still be 25-45 million bu smaller. The US spring wheat plantings will be finishing up in next 10 -14 days so 2017/18’s overall US wheat crop really remains a mystery. Downside seems limited, but another world competitor needs to have a crop problem for wheat to have a big post-harvest price rally.

Disclaimer – The information contained in this report reflects the opinion of the author and should not be interpreted in any way to represent the thoughts of The PRICE Futures Group, any of ...

more