Can Workday Keep Its Unblemished Earnings Streak Alive?

(Photo Credit: Ken Teegardin)

Tech investors have something to be excited about when Workday (WDAY) reports 4th quarter earnings after the closing bell.

The cloud based financial management and HR app builder has been growing like crazy since its late 2012 IPO. Workday’s quarterly revenue has consistently increased between 61% and 110% on a year over year basis. To make the company’s fundamental growth even more impressive, Workday hasn’t missed top or bottom line analyst forecasts a single time.

This afternoon expectations are near the lower end of Workday’s monumental revenue growth range. Contributors on Estimize are predicting $230 million in sales, that would be a 62.3% year over year gain.

Workday’s track record is extraordinary, yet Wall Street is setting its sights lower again. The Street is forecasting revenue of $223 million. Investors will want to see more than that.

As promising as Workday’s revenue growth is, the company still isn’t profitable, and it trades at a rich valuation. Workday’s stock is priced at 24x sales. Mature companies within the industry like Salesforce (CRM) and Oracle (ORCL) trade at 8x and 5x sales by comparison.

WDAY PS Ratio (TTM) data by YCharts

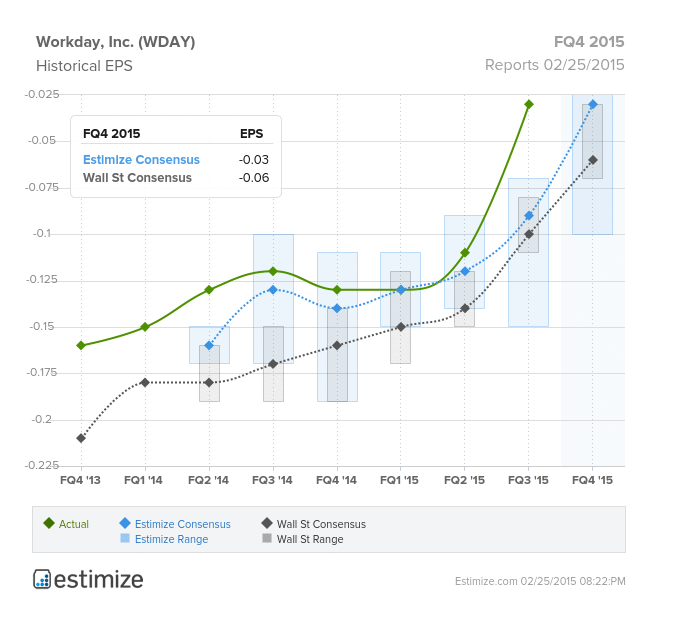

On the bright side, management has always kept loses thinner than Wall Street analysts predict. Estimize contributors believe Workday will report a 4th quarter loss of 3 cents per share. That’s significantly better than the Street’s forecast for a 6 cent loss.

After the closing bell we’ll see if Workday can keep its untarnished win streak alive.

Disclosure: There can be no assurance that the information we considered is accurate or complete, nor can there be any assurance that our assumptions are correct.