5 Stocks To Watch This Week November 9, 2015

(Photo Credit: Wendy)

Monday, November 9

![]()

![]()

Tuesday, November 10

![]()

Thursday, November 12

![]()

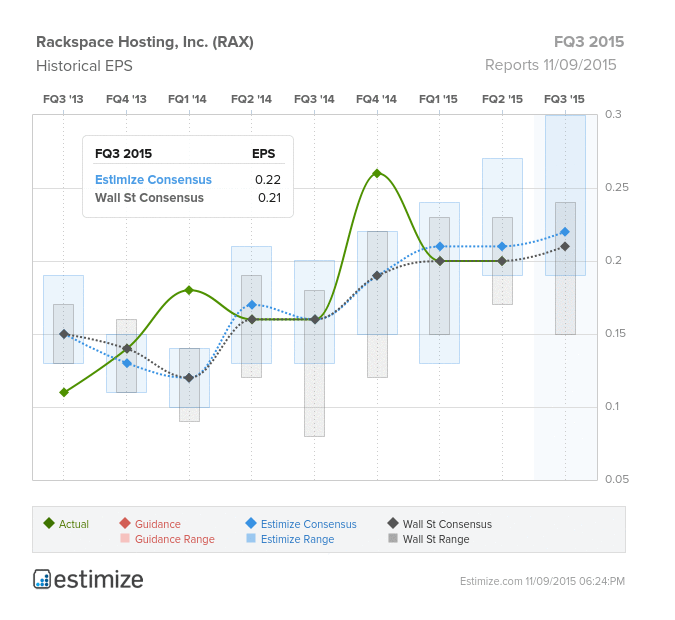

Rackspace Hosting (RAX)

Information Technology - Internet Software & Services | Reports November 9, after the close.

The Estimize community is looking for EPS of $0.22, only a penny better than Wall Street. Estimize is also looking for higher revenues of $504.44M vs. the Street’s $503.60M.

What to watch: Even though Rackspace is considered one of the first to get into the cloud industry, first movers advantage hasn’t helped this stock which has fallen nearly 42% since the beginning of the year. In order to differentiate itself in a very crowded market, RAX recently reorganized its business model to include computing and support. Behemoths such as Microsoft, IBM and Alphabet (Google) are all making a play for cloud computing, with Amazon really owning the space at this point, their Amazon Web Services makes up 25% of the market. Price competition has gotten incredibly stiff, with Rackspace still charging higher prices than its peers. To remain afloat Rackspace recently announced a partnership with Amazon, which still wasn’t enough to buoy the stock. At nearly 30 times forward earnings, a rich valuation doesn’t seem justified at this point given current fundamentals. Any improvement in share price this year relies on Q3 numbers coming in ahead of expectations.

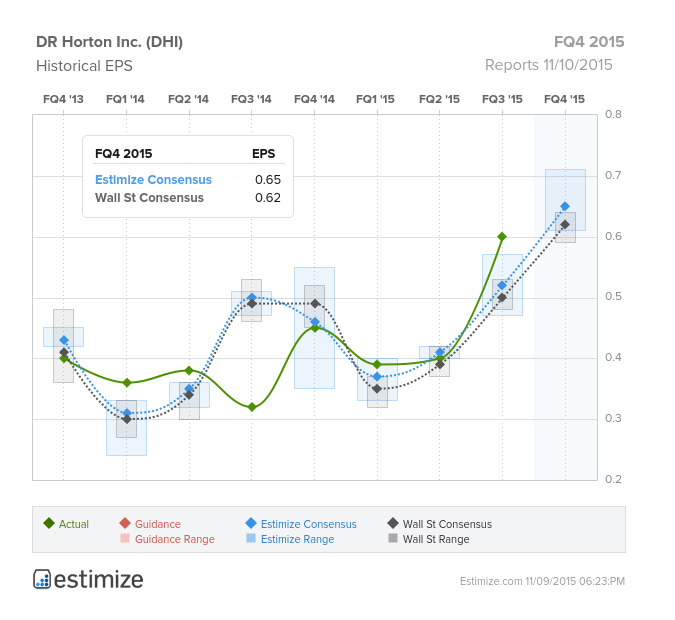

DR Horton (DHI)

Consumer Discretionary - Household Durables | Reports November 10, before the open.

The Estimize consensus calls for EPS of $0.65, three cents better than what Wall Street is looking for. Revenues are in-line at $3.055B.

What to expect: This week we get a read on the health of the US consumer and their willingness to purchase large ticket items such as homes when DR Horton reports. Housing had a robust summer season, with signs that that could potentially be breaking down. While Housing Starts came in much stronger than expected in September driven by a spike in multi-family units, that was offset by a decline in permits. New home sales also fell in September, and supply surged to 5.8 months from 4.9 months in August and 5.5 months in September last year. As the biggest home builder in the country, DHI is expected to benefit from a housing market that stayed strong in Q3. While it is exposed to nearly every US region, it has minimal exposure to Northeast which has been performing the worst and saw New Home Sales decline 62% in September. Overall investors should look for guidance around the housing market for the last quarter of the year when DR Horton reports tomorrow. A recent reading of Home Builders Sentiment showed continue confidence surrounding the strength of housing, coming in at 64 in October, up from 61 in September.

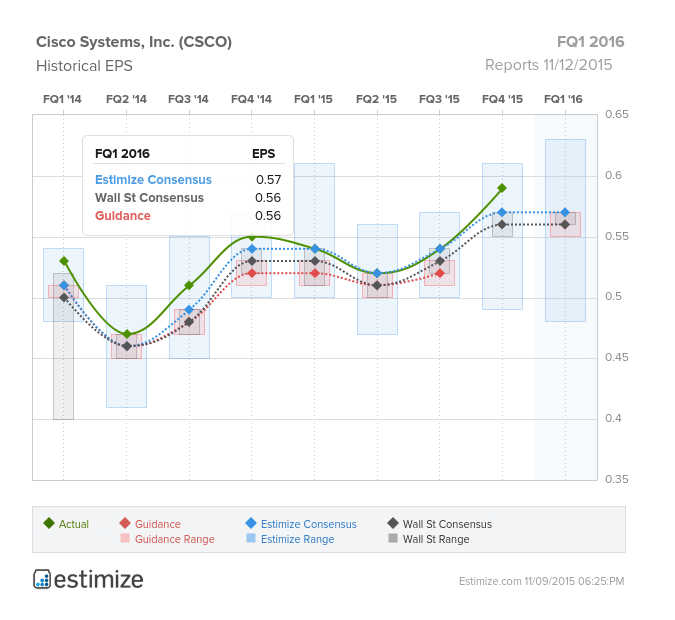

Cisco Systems (CSCO)

Information Technology - Communication Equipment | Reports November 12, after the close.

The Estimize community is looking for EPS of $0.57, only a penny better than the Wall Street consensus. Revenues are also fairly muted at $12.698B vs. the Street’s consensus of $12.636B.

What to watch: Despite meeting or beating top and bottom-line expectations for the last two quarters, low single digit growth for both of those metrics has left much to be desired from the communications equipment giant. However, Cisco is still a leader in its industry, and has been making strategic investments to remain so. Specifically, analysts are expecting impressive growth out of its next-gen firewall business. The rollout of its 100G+ data center platforms is anticipated to occur in 2016, through which the company will be focusing on its increasing cloud customer base, expecting growth in bookings for its Meraki Cloud Services. Analytics tools will also be a main focus, especially with a new partnership with Paxata and investments to drive automation for data centers. The company’s infrastructure currently routs 80% of global internet traffic.

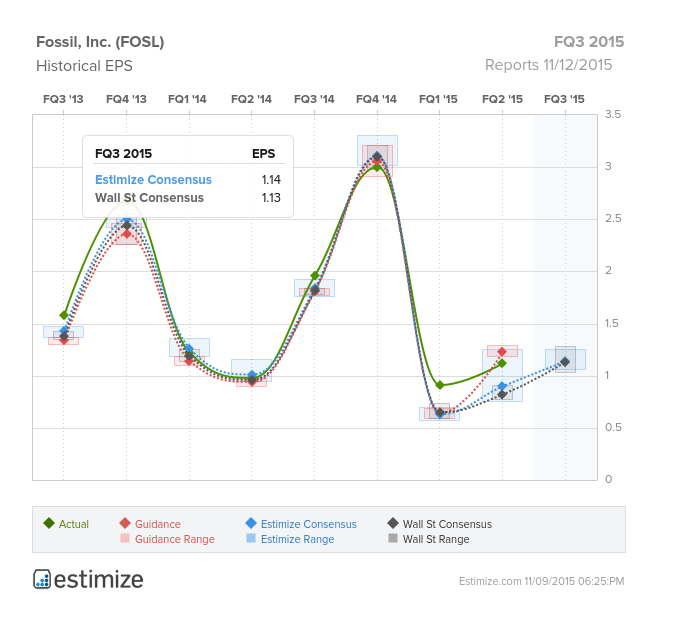

Fossil (FOSL)

Consumer Discretionary - Textiles, Apparel & Luxury Goods| Reports November 12, after the close.

The Estimize consensus calls for EPS of $1.14, only a penny higher than what the Street is expecting. Revenues are expected to come in at $785.14M as compared to the sell-side consensus of $784.75M.

What to watch: Fossil has an impressive portfolio of brands such as Michael Kors, Tory Burch, Armani, and the newly signed license with Kate Spade, creating the watches, jewelry and small leather goods for these designer brands. However, their biggest brand, KORS has seen a decline in demand for their watches over the last year, despite beating expectations in their latest report. But as tastes change and the US consumer becomes very particular with how they allocate their discretionary income, Fossil remains very cautious. In their Q2 report the company warned that Q3 2015 would be their weakest quarter of the year due to difficult year-over-year comparisons. One concern this quarter is around sluggish international sales, specifically in China and Europe, being further exacerbated by the strong US dollar. One bright spot could be the company’s investments in wearable technology in the form of smart watches.

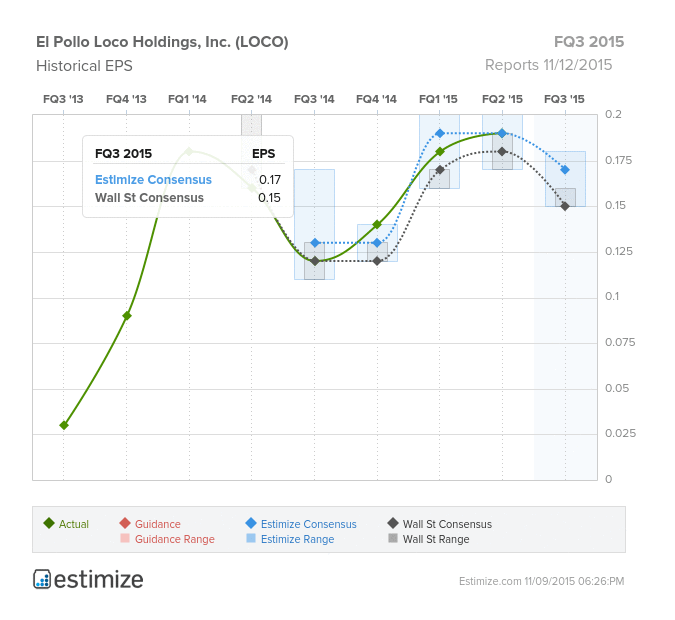

El Pollo Loco (LOCO)

Consumer Discretionary - Hotels, Restaurants & Leisure | Reports November 12, after the close.

The Estimize community is looking for EPS of $0.17, two cents higher than the Wall Street expectation. Estimize is also looking for slightly higher revenues of $90.48M vs. the Street’s $90.49M.

What to watch: Since going public in July 2014, El Pollo Loco’s main goal (along with several others in the fast casual space) has been to reach the the status of Chipotle as a stellar performer and darling of the industry. With 4 quarters as a publically traded company under its belt, this doesn’t seem as though it’s in the immediate future for LOCO. For each of the quarters the Mexican-inspired chain has just barely met or missed both top and bottom-line expectations. Despite having over 400 locations, the chain has not done well with its regional distribution, with about 86% of all restaurants located in California. Same restaurant sales, which really should be on fire at this stage, fell 0.5% last quarter, caused by a nearly 4% decrease in traffic but partially offset by a 3.4% increase in average check. Plagued by massive debt at the time of its IPO, El Pollo Loco has never quite been able to recover, and meager customer traffic and same store sales figures have not been enough to overcome the debt situation. With its stock down 42% this year alone, this restaurant is going to have to put up a positive surprise when they report on Thursday.

Disclosure: There can be no assurance that the information we considered is accurate or complete, nor can there be any assurance that our assumptions are correct.