Why Muted Earnings Expectations Could Be Good For Facebook

Investors are looking for top and bottom line growth nearing 50% when Facebook (FB) reports fourth quarter earnings after the close.

50% year over year growth is stellar for any company doing over $10 billion a year in sales. Facebook’s massive success last year has made it an exception to that rule.

(Graph Above from ChartIQ Visual Earnings)

Facebook stock exploded higher in 2014 as the social network began juicing profits through its mobile ads. Targeted mobile ads enabled Facebook to improve its operating margins from 41% in the first quarter of 2013 to between 57% and 60% in the first three quarters of last year.

Along with the rising profitability in 2014 earnings and revenue increased by an average of 125% and 64% respectively. Last quarter Facebook’s stock slipped when it missed the high expectations from investors on Estimize. In the upcoming quarter contributing analysts on Estimize have softened their view and are forecasting earnings and revenue growth to decelerate to 61% and 47%.

Facebook’s numbers will still be huge this quarter, but the company’s expansion is projected to flatten out significantly. CEO Mark Zuckerberg has been ahead of the curve searching aggressively for acquisition targets which could sustain or boost Facebook’s growth.

The best deal Facebook has made to date was its 2012 acquisition of Instagram for $1 billion. Instagram has now reached over 300 monthly active users (MAUs) and is expected to be a major source of revenue growth this year. On December 19 analyst Mark May at Citigroup said, “Using what we believe to be conservative assumptions around user growth and monetization, we believe Instagram is worth $35bn – up from the $19bn we had previously estimated due to faster growth in its audience as well as continued monetization gains by social media properties.”

Facebook’s core product growth is beginning to shift out of focus because its 1.350 billion MAU’s are feared to be approaching saturation in key markets. That’s why there’s been emphasis on acquisitions like Instagram, Oculus VR, and Facebook’s most aggressive purchase to date, WhatsApp. Facebook paid roughly $19 billion for the internet messaging app which reached 450 million MAUs faster than any other company in history.

WhatsApp provides Facebook with massive international scale, a stage it has room to improve upon. Last quarter $1.514 billion (47%) of Facebook’s $3.203 billion in total revenue came from users in the US and Canada and an additional $844 (26%) million came from Europe. Considering that the Estimize community predicts the rate of profit growth to fall further to 26% next quarter, WhatsApp and Instagram could be catalysts which propel Facebook above dampened expectations.

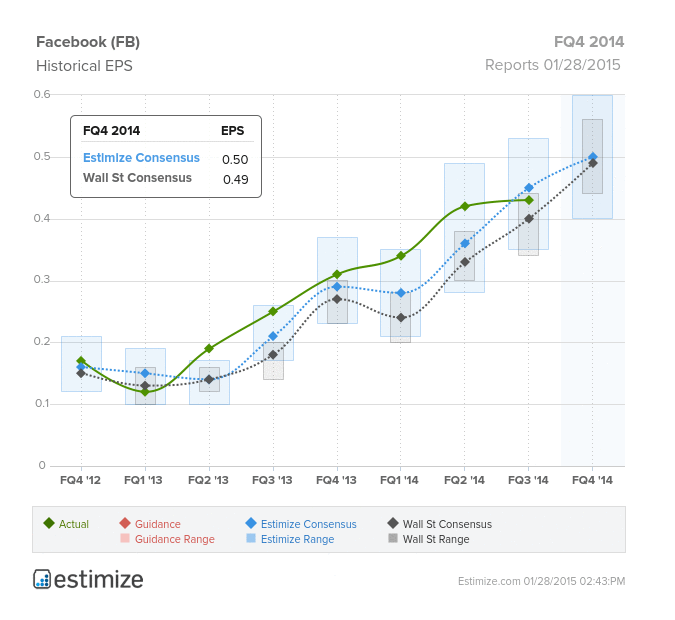

For now the earnings picture remains fixated on Facebook’s social network. 142 analysts on Estimize have come to a consensus expectation that the company will beat Wall Street earnings estimates by 1 cent share and come out a marginal $19 million (0.5%) ahead on revenue.

A year over year earnings increase of 61% is fantastic by most standards, but the expectation this quarter is that Facebook will exceed that benchmark by 1 cent per share. The upside here is that investors on Estimize are expecting the smallest earnings beat in recent history. That leaves plenty of opportunity to the upside if Facebook can top its muted expectations in the same way that Apple did yesterday.(AAPL)

(Photo Credit: Master OSM 2011)

Disclosure: There can be no assurance that the information we considered is accurate or complete, nor can there be any assurance that our assumptions are correct.