Why I Told Rhonda “I’m Not Interested”

My phone rang. It was a local number I didn’t recognize.

I usually don’t answer unless I know who is calling. But I was supposed to meet a friend for lunch in a few minutes, so I thought maybe he’d changed his number (we’d communicated by email).

“Hi, Marc. This is Rhonda from…” the voice on the line said eagerly. It was a financial planner from one of the discount brokers that I use. She wanted to see if my portfolio was meeting my goals and if she could sit down with me to figure out ways to help me reach those goals.

The charge for this help was 0.75% to 1% of the assets being managed depending on the size of the account. That’s the industry standard.

I turned Rhonda down. It wasn’t the first time. She’s persistent. Considering what I do for a living, I don’t need Rhonda’s help, and I certainly don’t want to pay thousands of dollars per year for it.

And nothing against Rhonda, but I suspect most investors don’t need her help either.

Here’s why…

If you own a diversified portfolio of Perpetual Dividend Raisers (companies that raise their dividends every year) or The Oxford Club’s Gone Fishin’ Portfolio, you’re invested in a wide range of stocks that should outperform the market over the long term. Historically, they always have.

And you’ll save thousands of dollars by doing so.

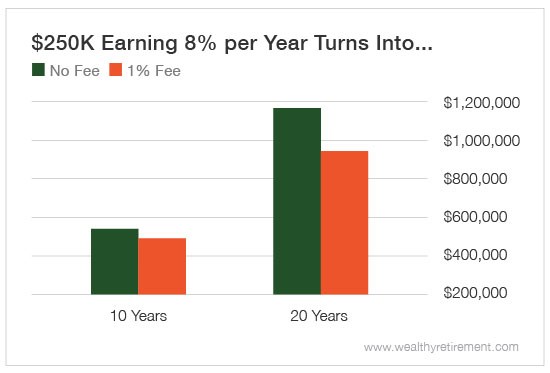

If you have a portfolio worth $250,000 and you earn an average of 8% per year, after 10 years, you’ll have $539,731. In 20 years, it will be worth $1.16 million. That’s the power of compounding for you.

However, if you pay an advisor 1% per year, the totals end up being a much smaller $488,123 after 10 years and $953,057 after 20.

By paying an advisor 1% per year, you lose out on more than $212,000 – nearly the size of your account to start with. Again, that’s the power of compounding. By missing out on just 1% per year, the results change significantly.

Some brokers have options where you can work with a planner to set up your portfolio, but it won’t be a full-service program. In other words, they’ll create a plan for you (but won’t monitor it), work with you throughout the year and stay on top of your goals.

That’s a much cheaper 0.3% per year.

Even that small amount changes your numbers more than you think it would.

Instead of $539,731, you end up with $523,758. Rather than owning a nest egg worth $1.16 million you have $1.09 million.

Just paying 0.3% per year, you wind up with $68,000 less.

If you don’t need constant monitoring, you could use a planner that charges a one-time fee. That usually costs less than $1,000.

There’s nothing wrong with working with a financial advisor if you need help – especially if it’s with more complicated issues like insurance, trusts, etc. Or if you’d just feel less stressed and would sleep better at night knowing there is someone watching your accounts for you, then by all means, spend the money on a good financial professional. It will be well worth it.

But the majority of investors are fully capable of investing in quality companies and index funds on their own. By skipping the financial advisor, you’ll keep more money in your account, which thanks to compounding, will turn into a meaningful amount over the years.

No one cares more about your money than you do – not even a professional. Take control of your finances and invest in Perpetual Dividend Raisers or the Gone Fishin’ Portfolio.

And the next time Rhonda calls, tell her “I’m not interested.”

Good investing,

Marc

Disclaimer: Nothing published by Wealthy Retirement should be considered personalized investment advice. Although our employees may answer your general customer service questions, they are not ...

more