Wells Fargo: Big Dividend, Attractive Valuation

Wells Fargo (WFC) is down over 13% this year, while the Financials sector ETF to which it belongs (XLF) is down only 7%, and the overall market (S&P 500) is essentially flat. We believe Wells Fargo has sold off more than it should have for a variety of reasons. For starters, WFC is less sensitive to interest rates than many other banks, and it should not have sold off as much when the Fed recently tamed its expectations for future interest rate hikes. Additionally, WFC inappropriately sold off as many investors reacted fearfully to recent news stories about energy sector exposure, analyst ratings, and new retirement account regulations. We believe these events, combined with WFC’s strong financial position and big 3.2% dividend yield, make now an excellent buying opportunity for long-term investors.

Why is Wells Fargo Unique?

Wells Fargo is unique among large banks because almost half of its revenues come from fee-based business, and because it is perceived to be much less risky.

For starters, the following table shows WFC’s large, diversified, fee based revenues.

These diversified fee revenues make WFC less susceptible to low interest rates because it has steady revenues coming in regardless of its net interest margin. (For reference, net interest margin measures the spread between the rate a bank receives on loans and the rate it pays on deposits; and the Fed’s extended period of low interest rates has compressed net interest margins, and made it more difficult for banks to be profitable). WFC’s significant fee business is different than many other large banks that rely more heavily on interest rates to be profitable. Also worth noting, WFC’s beta (a measure of market risk exposure) is below one whereas its peer, Citigroup, is around 2, suggesting WFC is much less risky in this regard.

Wells Fargo is able to grow in ways other banks cannot because it is perceived to be much less risky. For example, WFC has less extensive capital market operations (these are often perceived to be higher risk), and a much more transparent balance sheet (basic consumer and commercial loans make up a large portion of WFC’s holdings). These lower risk operations allow WFC to grow at a time when other banks cannot. For example, WFC has been able (and allowed by regulators) to increase its healthy dividend payments to a much higher level than many of its peers. Additionally, WFC has been able to take on new business opportunities that other banks cannot. Specific examples include WFC January 2016 purchase of GE Railcar Services, and its expected ~$31 billion acquisition of assets from GE Capital in the first half of 2016. Because of its financial strength, WFC is able to take on new business and grow its net interest income at a time when growth is particularly challenging to achieve.

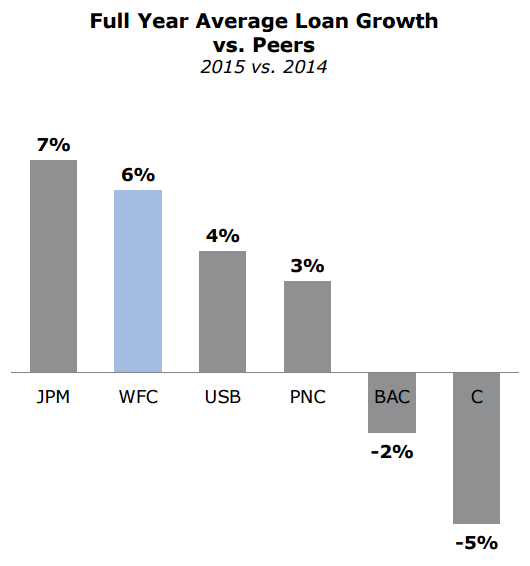

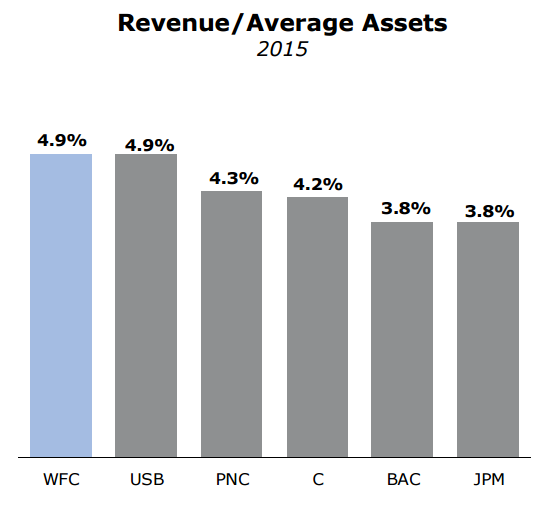

WFC’s financial strength has also enabled it to grow its loan portfolio at a faster pace than peers, and generate higher revenues per assets, as the following charts show:

(source: Investor Presentation,p.8)

(source: Investor Presentation,p.11)

Why Has Wells Fargo Sold Off?

As mentioned previously, WFC has sold off for a variety of reasons, and we believe this has helped create an attractive entry point for long-term investors. For example, financial stocks in general have sold off as the US Fed lowered its expectation for the pace of interest rate hikes. However, we believe WFC sold off more than it should have for a variety of reasons (and not only because of its near 50% fee-based revenue which is largely unaffected by interest rates).

Recent fears over WFC’s exposure to energy sector loans may have contributed to its stock being oversold. For example, this March 24th Wall Street Journal article may have stoked fears among investors by suggesting “[t]he number of energy loans labeled as "classified," or in danger of default, is on course to extend above 50% this year at several major banks, including Wells Fargo & Co…” The selloff of Wells Fargo stock accelerated when this article was published as shown in our graph at the beginning of this article. The following table shows Wells Fargo’s exposure to “Oil and Gas,” and the company has already set aside a $1.2 billion of allowance for credit losses allocated for its oil and gas portfolio which accounts for 6.7% of its total oil and gas loans outstanding. (Investor Presentation, p.16).

Similarly, analysts at UBS came out with a bearish sell report on WFC on the same date. The report suggested WFC revenues may be under pressure from continued low interest rates and weak risk appetites among the bank’s clientele.

Further, as this recent Wall Street Journal article suggests, may investors fear negative impacts on banks like Wells Fargo from new and more stringent Labor Department rules on retirement account advice. The article suggests that banks like Wells Fargo will be negatively impacted by higher expenses associated with implementing new requirements.

What is Wells Fargo Worth?

Despite the current low interest rate and high regulation banking environment, Wells Fargo generates a lot of cash flow. In 2015 the company returned $12.6 billion to shareholders in the form of dividends and share buybacks, and that represented only 58% of the company’s net income applicable to common stock (investor presentation, p.17). That means total net income applicable to common stock was $21.724 billion, and if we discount that by Wells Fargo’s cost of equity(9.125%) minus a 2.5% growth rate (assuming it keeps pace with GDP), then Wells Fargo shares are worth $304.9 billion. That give the stock more than 37% upside potential considering its current market cap is only $238.8 billion.

Also worth noting, WFC management plans to eventually return a higher portion of earnings to shareholders in the future (perhaps as much at two-thirds, instead of the 58% mentioned above). With regulatory approval, WFC may achieve this goal within the next few years, and this will result in even more cash being returned to shareholders.

Another way to gauge WFC’s value is its current price to book ratio (a common metric for valuing banks). WFC’s current price to book ratio suggest the stock may be undervalued. The ratio is currently around 1.4x. It was 1.6x at the end of 2015 and 1.7x at the end of 2014. This suggests WFC’s common stock may be undervalued, especially considering the company’s reputation for a strong, healthy, and transparent balance sheet.

Further, famous value investor Warren Buffet added to his already significant stake in Wells Fargo earlier this year as the stock continued to decline. Buffett is famous for his contrarian, “be greedy when others are fearful” investment approach. Wells Fargo has fallen further since Buffett’s recent purchases, and we believe this makes for an even more attractive entry point for long-term investors.

What are the Risks?

Wells Fargo faces a variety of significant risks. We’ve described several of them above (e.g. low interest rates, energy sector exposure, bearish analyst reports, and new regulations). Obviously, interest rates pose a big risk. It’s harder for banks to be profitable in a low interest rate environment, and if the US fed keeps rates lower for longer, that makes profitability more challenging for all banks, Wells Fargo included. Additionally, regulations are an expensive challenge for the banking industry, and they go much further than simply the new Labor Department rules for retirement accounts. For example, regulators heaped new expensive regulations on banks following the financial crisis, and any new rules could make profitability more challenging for Wells Fargo in the future. Further, the US Justice Department has extracted many tens of billions of dollars from the banking industry via lawsuits since the financial crisis, and new lawsuits pose another potential risk for Wells Fargo. Another risk is if any particular economic industry becomes stressed (such as energy as mentioned above) then that too could put significant pressure on the profitability of Wells Fargo (although its business is relatively well-diversified as mentioned previously).

Conclusion:

We like Wells Fargo. It has a big 3.2% dividend yield, a diversified business model, and the potential for significant price appreciation. In fact, we like Wells Fargo so much that we’ve ranked it number nine on our list of Ten Blue Chip Stocks Worth Considering. We believe recent market events have caused the stock to sell off more than it should have and created an attractive buying opportunity. If you are a long-term investor, now may be an excellent time to add Wells Fargo to your portfolio.

Disclosure: None.