WageWorks Exceeding Expectations

HR and Employee Benefits provider WageWorks (NYSE:WAGE) recently reported a sales revenue of $334.3 million for 2015, a 25% increase Y/Y - beating Wall Street's expectation. The company's revenue grew at a 22% clip annually over the last three years since its IPO and has become a fast grower in HR service industry. The Affordable Care Act (ACA) offers the company great opportunity to unlock its full earnings power and continue its fast growth in the near future.

WageWorks is an HR service company with a market cap of $1.6 billion. The company solely dedicates itself to administer Consumer-Directed-Benefits accounts (CDBs), such as Health and Dependent Flexible Spending Accounts (FSAs), Healthcare Saving Accounts (HSAs), Health Reimbursement Arrangement Accounts (HRAs) as well as Commuter Benefit Accounts, OBRA and Other Employee Benefit Accounts.

WageWorks went public in 2012. It grew quickly through aggressive acquisitions of smaller competitors. Over the last three years, the company has successfully managed to increase its revenue 22% annually. In 2014, WageWorks acquired CONEIX for $118 million with the expectation to generate an additional $23 million to $25 million in annual revenue moving forward.

WageWorks operates under four sectors: Healthcare, Commuter, COBRA and Others, and each account for 53%, 19%, 15% and 13% of its total revenue respectively. Healthcare accounts service is the core business, and generated 53% of the company's total revenue in 2015. This was a 13% increase Y/Y. Others revenue increased 135% and COBRA grew at 60% in 2015.

Market Trends of Healthcare Spending and Savings

According to the FSA, HAS and HRA Trends and Projections Report from FlexibleBenefit.com, the Affordable Care Act will continue to impact health care market conditions for the next three to five years. A majority of employers will continue to offer Flexible Spending Accounts (FSAs), until FSAs market share reaches a mature level. The Health Savings Accounts (HSAs) will increase significantly as they offer employers cost reduction and employees more freedom to choose the appropriate healthcare plan to save on premiums for health insurance. Health Reimbursement Arrangements (HRAs) may become more prevalent due to its lesser impact on Cadillac Tax thresholds. The purpose of the Cadillac Tax was to limit the impact of rising healthcare costs by discouraging costly benefit packages. The Cadillac Tax requires companies to pay a 40% tax on the dollar value of coverage for these high-cost healthcare benefit packages, plans that exceed $10,200 for individuals and $27,500 for other coverage, starting in 2020.

The strong growth projection in HAS and HRA would offer WageWorks a great opportunity to continue its fast growth and unlock its full potential earning power.

Strong Management Incentive Plans

According to the company's 10-Q filing in Sept. 2015, WageWorks created strong benefit incentive plans for its management team to drive revenue and increase earnings significantly moving forward. In 2014, the company granted 199,000 market-based-performance restricted stock units (RSU) to certain executive officers. For any twenty consecutive trading day's period, if the stock price hit $75, $90, $100 per share, restricted stock units will be eligible to vest at 50%, 100%, and 200%. In 2015, WageWorks granted 140,000 performance-based restricted stock units to certain executive officers. Once the company achieves revenue growth above 20%, the restricted stock units will be eligible to vest at 150%, meaning there are strong incentives in place to reach the company's ambitious growth targets.

Lack of Significant Competitor

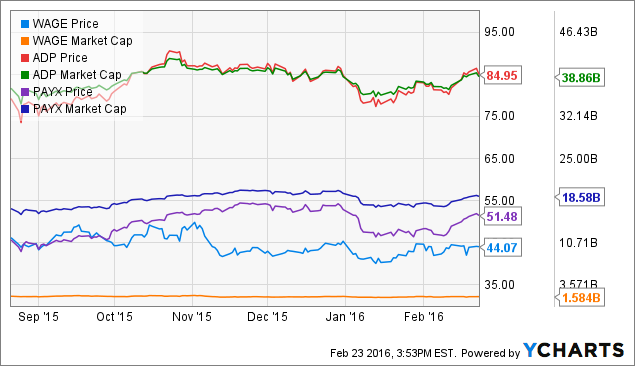

WageWorks has no significant competitors of a similar size. Payroll Giant ADP (NASDAQ:ADP) has a market cap of $38.8B. Ceridian is private holding company with revenues at $944 million. Both companies have a much broader HR, Payroll, Tax and recruitment service business than WageWorks, who solely focuses on Consumer-Directed-Benefit accounts. This niche allows WageWorks room to continue growing a good pace. WageWorks could be a takeover target by the payroll giants once its growth levels out.

In Aug. 2015, the company's board authorized a $100 million stock repurchase program without an expiration date. So far, no shares have been repurchased.

According to the latest SEC filing, WageWorks' top three shareholders Fidelity (14.99%), Black Rock (9.4%) and Vanguard (7.84%) have all added positions since late 2015.

Conclusion

From a value consideration, WageWorks is not undervalued at this point. With P/E at 81.3, P/B 4.9, P/S 4.9, P/Cash Flow 13.3, and a Debt/Equity ratio that stands at 0.23. However, the Affordable Care Act may offer the company a great opportunity to keep growing at a fast pace in the near future. Value investors should be patient for the next downturn to consider a long position for this fast growing company.

Follow our Blog at: www.LeverageEquityResearch.com.