United Continental Holdings Looks Like A Buy This Earnings Season

Photo Credit: Christian Barmala

United Continental Holdings (UAL) Industrials - Airlines | Reports October 17, After Market Close

United Continental is the second of the major airlines to report earnings, following Delta’s mixed third quarter results earlier this week. United, like Delta, is headed into its third quarter report with with tepid expectations. Factors such as the strong U.S. dollar, low fuel surcharges, declining business demand and increased competition should contribute to a decline in revenue and margins. The company has already indicated that its key PRASM metric is expected to fall between 5.5% and 7.5% compared to the same period last year

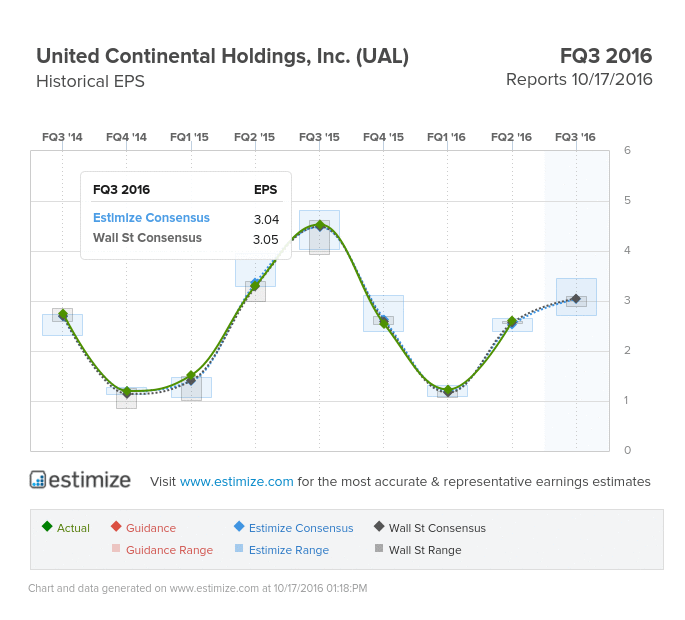

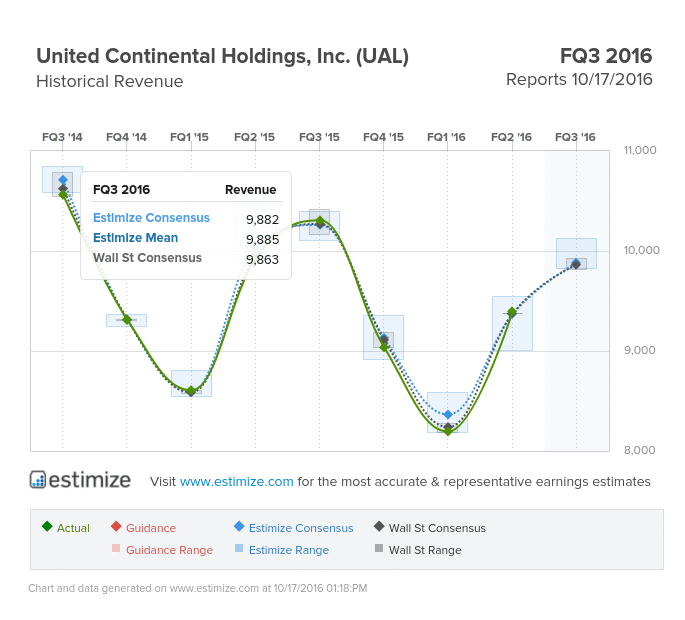

Analysts surveyed at Estimize are calling for earnings per share of $3.04, reflecting a 34% decline from a year earlier. That estimate has climbed 3% since the company last reported in July. Revenue for the period is estimated to drop 4% to $9.88 billion, marking a slight improving from the previous two quarters. Given the tough times the airlines is experiencing its surprising that shares are only down 6% year to date. Historically the stock remains flat following an earnings report and 30 days afterwards.

Major airlines have faced significant headwinds lately from foreign currency pressures, mounting terrorist threats, weaker last minute business flights, and a simple reluctance to fly. United, in particular, has witnessed sharp declines across earnings and revenue with negative growth in the past two quarters. The second quarter posted a 5% decline in revenue and 6.6% drop in its crucial PRASM measure.

Management has already indicated that investors should expect similar declines throughout the third quarter. In its August Traffic reports the company posted marginal increases in consolidated traffic and capacity but also stated that PRASM is expected to decline 5.5-7.5% for the third quarter. September’s report instilled confidence in investors with surprisingly strong traffic trends, but that won’t be reflected in Q3 earnings.

Meanwhile, United is expected to see pricing pressure from increasing competition. Low budget airlines such as Southwest and Spirit have captured greater market share through a more consumer friendly pricing model.

Disclosure: Each week, Forcerank runs a variety of games covering different industries. What we have found, is that the highest ranked companies in their ...

more