Three Reasons Why Micron Technology, Inc. Can Go Even Higher

Micron Technology, Inc. (Nasdaq:MU) stock has already exploded after two years of poor performance. On a one-year basis, the stock has moved from just $12 to the current price of just over $30. Not surprisingly, given the rapid gain, some investors are nervous that the stock is moving into overvalued territory and that there is limited upside potential left. These bears (see, for example KeyBanc’s Weston Twigg) warn that the stock will crash if demand for Micron’s DRAM and NAND memory chips cool off. However here are three reasons why bulls believe the stock still has further room to grow:

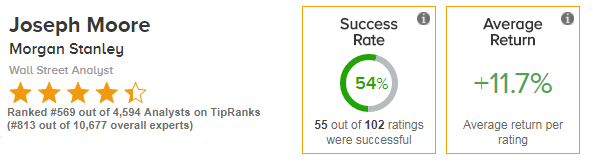

1. Ongoing Fundamental Momentum – Micron’s stock has been propelled by tight supply/ demand dynamics due to increased demand from cloud providers, smartphone manufacturers, vehicles and networks. In the first nine months of fiscal 2017 DRAM sales rose 70% and NAND sales 40% when compared with the same period in 2016. And this increased demand has boosted prices- for example in the fiscal third quarter just reported by Micron DRAM prices were up 14% and NAND 17%. Over half of Micron’s revenue comes from DRAM hence the big knock on effect on Micron’s overall strength. For example, Micron has also finally announced that in fiscal Q3 it has again achieved free cash flow- money which can be used for share repurchasing or indeed further company expansion. The good news is that this situation is set to continue according to Morgan Stanley analyst Joseph Moore.

He carried out his own investigation into the market and concluded that demand will remain strong while supply will remain inadequate. In fact, Morgan Stanley has a $40 price target on MU stock. Macquarie Research also came to the same conclusion, and so did IC Insights- a semiconductor market research company. IC Insights claims that DRAM sales will rise by 39% in 2017 due to a 37% average selling price increase. For example, the research points out that smartphone shipments will remain strong due to the steady increase of smartphone demand from developing countries. IC Insights is also expecting NAND to rise by 25% in 2017. This outlook is reflected by management’s very bullish revenue guidance for Micron’s fiscal fourth quarter of $5.7-$6.1 billion which it announced on the company’s June 29 earnings call, and comes in well above the pre-earnings consensus of $5.62 billion.

2. Cost Cutting – Partly as a result of its impressive cost cutting initiatives, Micron has also ended up making another important step in the right direction by diversifying its revenue base. As well as cost cutting via traditional methods like reducing staff numbers, it has also increased operational efficiency and diversification with a number of smart acquisition moves. Names that spring to mind include Inotera Memories, Tidal Systems and Elpida Memory. These acquisitions have freed from Micron from its dependence on the weaker PC sector. For example, we can see that in the most recent quarter the DRAM sales from PCs alone only amounted to 16% of the company’s total revenue.

3. Not Overvalued – Micron may look expensive, but it certainly looks a lot cheaper when you compare it to larger rival companies. For example, the stock is only trading at 5x its anticipated 2018 EPS of $5.61 which comes in notably below the average forward PE of 6 for the memory semiconductor industry. Stocks with much higher PE ratios include Intel (INTC) and Western Digital (WDC) which have both have a forward PE ratio of 11- more than double Micron’s.

And the stock certainly has the support of the Street. In the last three months, financial accountability engine TipRanks reveals that Micron has received 17 buy ratings, 2 hold ratings and just 1 sell rating. The average analyst price target of $39.94 also suggests considerable upside potential of 32.25% from the $30.20 current share price. Interestingly even the lowest analyst price target of $30 is basically on line with the current share price.

(Click on image to enlarge)

Disclaimer: TipRanks is an independent cloud based service that measures and ranks digitally published financial advice. TipRanks' natural language processing (NLP) algorithms aggregate and ...

more