The Safety Net: A 7% Yield On Shaky Ground

A year and a half ago, I analyzed the dividend health of British Petroleum (NYSE: BP). The stock received a “C” rating.

At the time, BP had just reported 2014 results. It had plenty of cash flow to pay the dividend.

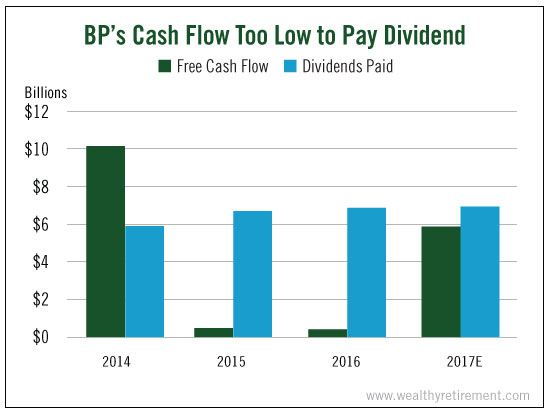

In fact, BP’s payout ratio was just 58% (far below my 75% threshold) in 2014. The company was able to pay shareholders $5.9 billion in dividends from $10.2 billion in free cash flow.

But still I was concerned about BP’s dividend. Analysts expected free cash flow to fall below $5.9 billion through 2017.

BP’s track record for dividend payments isn’t exactly stellar. While it raised its dividend each year from 2011 to 2014, the company eliminated its dividend in 2010 after the giant spill in the Gulf of Mexico. In 2011, it reinstated the dividend at just half the previous rate.

BP’s current $2.40-per-share annual dividend translates to an attractive 7% yield. But it’s still below the $3.36 it paid before the spill.

Let’s see if the situation has improved at all for the oil giant.

Disappearing Free Cash Flow

In 2015, BP’s gushing free cash flow slowed to a drip. After bringing in $10.2 billion in 2014, free cash flow totaled just $485 million last year. Hardly enough to pay the $6.7 billion it shelled out to shareholders in dividends.

This year, it will get even worse. Free cash flow is expected to come in at just $388 million. Meanwhile, the company is expected to pay $6.9 billion in dividends. It adds up to a ridiculous payout ratio of 1,765%.

In other words, for every dollar of cash flow, the company will pay out $17.65 in dividends. That’s not sustainable.

The good news is that in 2017, free cash flow is expected to jump to $5.9 billion. It’s a heck of a lot more than $388 million, but still below what BP pays in dividends.

Additionally, the company is still paying for the Deepwater Horizon oil spill. Last quarter, it racked up another $5 billion in charges, making the total more than $61 billion in costs and penalties.

While BP’s dividend track record has been impressive over the past few years, it did eliminate its dividend in 2010. The accident, an unusual event, caused the cut… but it still counts.

A recent dividend elimination plus several years of inadequate cash flow means that BP’s dividend is in worse shape than it was when I analyzed it a year and a half ago. Unless oil prices spike and drive cash flows higher, I’d be worried.

Dividend Safety Rating: F

If you have a stock whose dividend safety you’d like me to analyze, leave the ticker symbol in the comments section below.

Good investing,

Marc

Disclaimer: Nothing published by Wealthy Retirement should be considered ...

more