The 5 Stocks To Watch This Week - October 3, 2016

(Photo Credit: Mike Mozart)

Tuesday, October 4

Wednesday, October 5

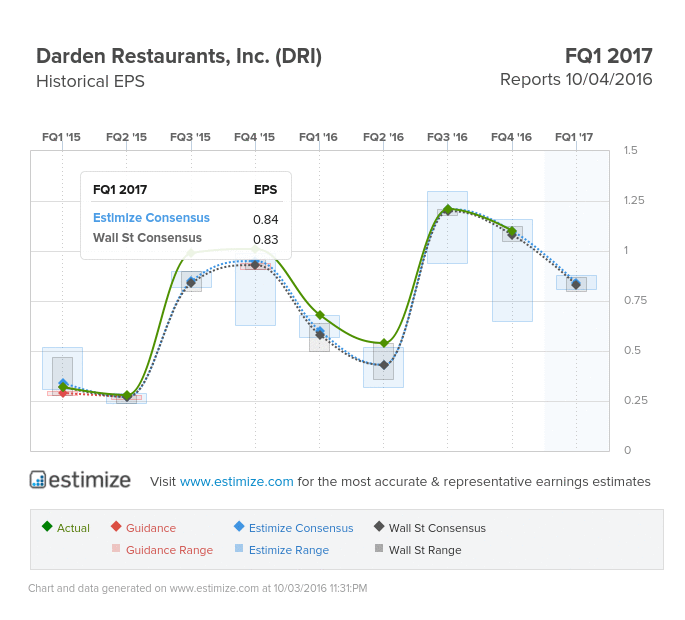

Darden Restaurants (DRI)

Consumer Discretionary - Hotels, Restaurants & Leisure | Reports October 4, before the open.

The Estimize consensus is looking for earnings per share of 84 cents, one cent higher than Wall Street and up 24% from the same period last year. That estimate has increased 2% since Darden’s most recent report. Revenue is anticipated to grow by 2% to $1.72 billion, a bit of a slowdown from last quarter. Despite meeting or beating on earnings in every quarter of their fiscal 2016, revenues missed in Q2 and Q4, the stock is down 4% YTD.

What to Watch: Darden’s recent recovery may have hit its first roadblock. The restaurant group capped off its fiscal 2016 on quite a sour note. Earnings were reported right in line with expectations but were significantly lower than prior quarters. Revenue, on the other hand, delivered negative growth and missed analyst’s targets by about $30 million. Early indications look as though Darden is back on track and prepared to deliver a strong FQ1 report. Initiatives to incorporate technology to improve kitchen efficiency combined with new menu items should help drive top line growth. Meanwhile, new store openings will help boost sales volume but also pressure margin growth.

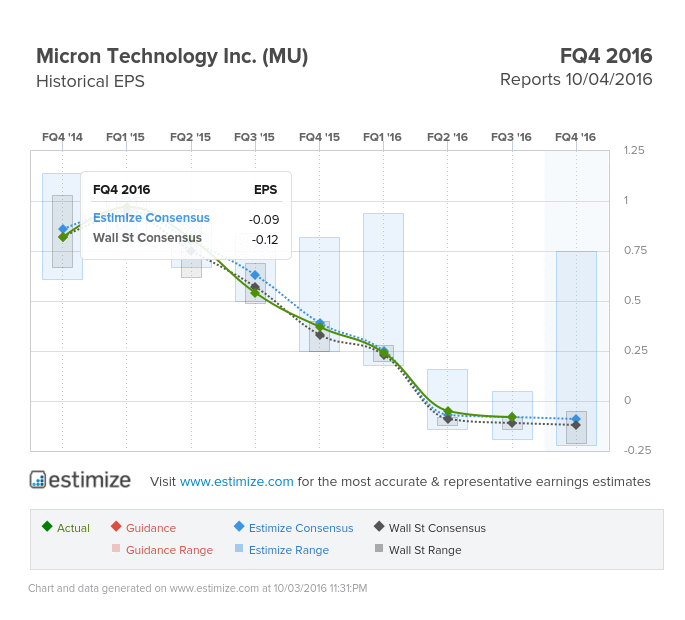

Micron Technology (MU)

Information Technology - Semiconductors | Reports October 4, after the close.

The Estimize consensus is looking for earnings of -$0.09 per share on $3.14 billion in revenue, 3 cents higher than Wall Street on the bottom line and inline on the top. Compared to a year earlier, earnings are expected to decrease by 125% with revenue decreasing 13%. EPS estimates have fallen by 235% since the last quarterly report, and revenue estimates have stayed flat. The stock is just about flat YoY.

What to Watch: Micron is coming off a mixed FQ3 which delivered in line earnings but fell short on the top line. Year over year comparisons were unfavorable on both counts thanks to weakness in its PC business. Earnings dropped over 100% for a second consecutive quarter while revenue fell 25%. Micron’s primary DRAM market appears to be rebounding with indications of a broader bounceback in PC demand. Additional initiatives to expand NAND and NOR flash memory solutions are being widely used in the latest mobile computing devices and should provide a boost to the top line. Micron still faces some near term headwinds. Pricing pressure in SSD and heavy competition from key players like Western Digital and Seagate Technology could squeeze results. Shares have soared over 60% in the past 6 months but it still would be wise to expect volatility coming out of this report.

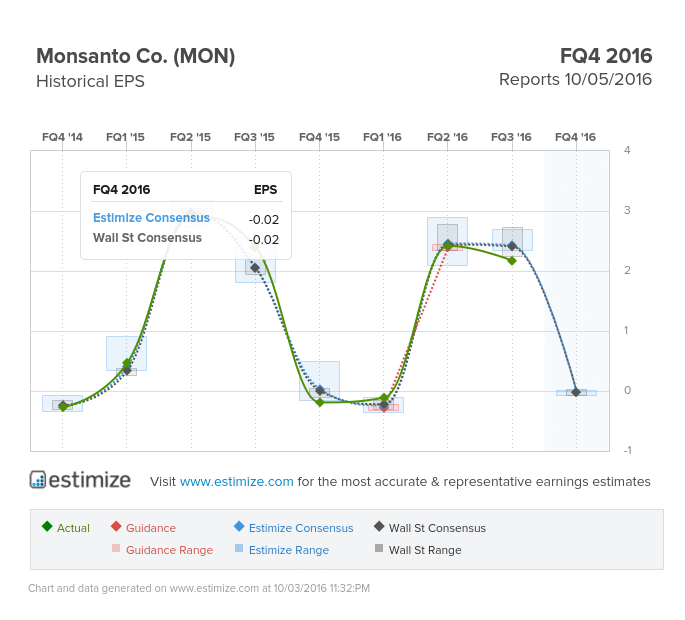

Monsanto (MON)

Materials - Chemicals | Reports October 5, before the open.

The Estimize consensus is looking for earnings per share of -$0.02 on $2.3 billion in revenue, in-line with Wall Street on the bottom line and in-line on the top. Compared to a year earlier, this reflects a 90% increase in earnings and flat sales. Earnings and revenue estimates have increased 46% and 2%, respectively, since the last quarterly report. The stock is up 4% since the beginning of the year.

What to watch: The biggest news out of Monsanto this year came just last month when it officially accepted Bayer AG’s all-cash buyout offer of $66 billion. The deal is still being sorted, but will surely be a large topic during Wednesday’s earnings call. Despite higher demand for areas in which MON operates, such as crop protection, the development of new agricultural solutions and the rise of digital agriculture, the company remains exposed to various macroeconomic risks. The global economic slowdown (specifically in China), decreased investments in the agricultural industry, lower agricultural prices and the continued strength of the U.S. dollar will likely drag down earnings again this quarter. Based on some of these continued concerns, Monsanto lowered FY 2016 guidance during its last quarterly report in June.

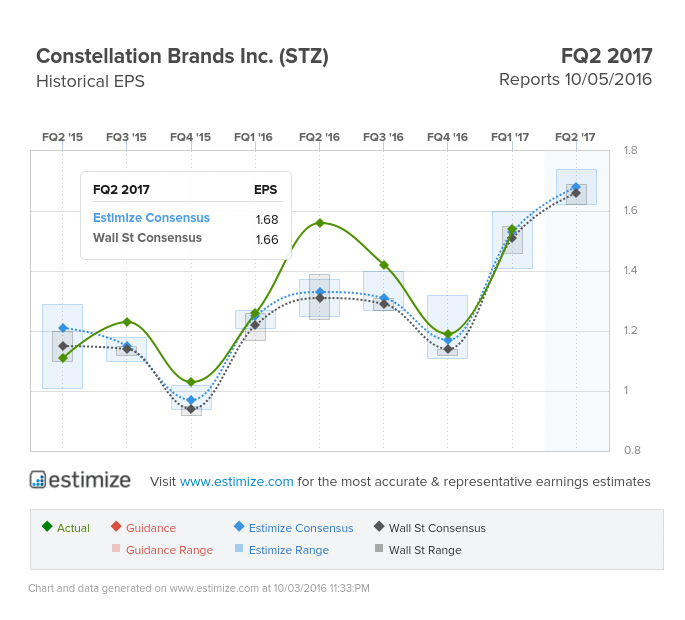

Constellation Brands (STZ)

Consumer Staples - Beverages | Reports October 5, before the open.

The Estimize consensus calls for EPS of $1.68, 2 cents higher than Wall Street’s consensus. Revenue expectations are also slightly higher than the sell-side, with the Estimize community expecting $1.97 billion, as compared to $1.96 billion. Earnings expectations have stayed relatively flat since last quarter. This puts YoY growth expectations at 8% for EPS and 13% for sales.

What to Watch: The summer quarter tends to be the strongest of the year for the alcoholic beverage distributors. Constellation Brands is expected to further benefit from its beer portfolio as demand continues to grow, specifically for imported beer. Net sales for beer increased 19% last quarter, primarily due to volume growth and favorable pricing. As for imported beer value, about 60% came from Mexico. The beverage company’s Mexican beer profile continues to perform best, with total revenues receiving a nice boost due to the popularity of Corona and Modelo. The wine business has also been growing rapidly (STZ is the largest premium wine company in the world), with brands like Robert Mondavi, Black Box and Dreaming Tree, and the recent acquisition of Meiomi. Wine and spirit sales increase 8% in the latest quarter. Despite ongoing strength, competition in this area is really starting to heat up.

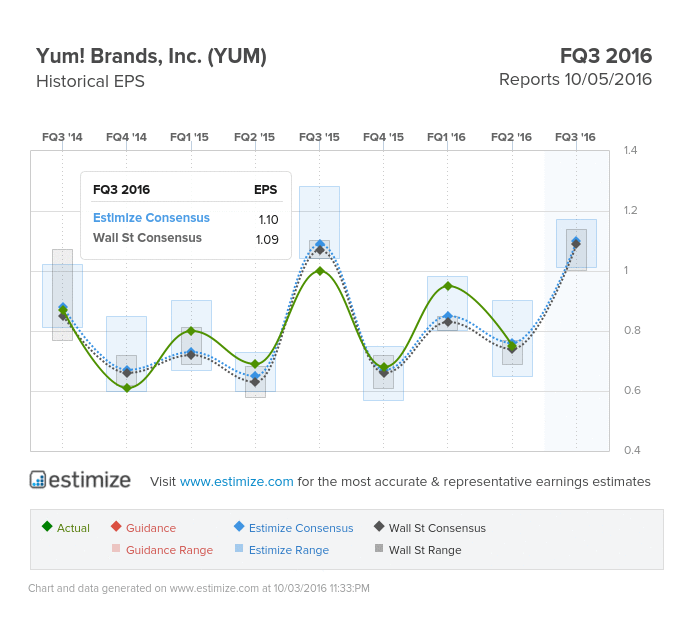

Yum! Brands (YUM)

Consumer Discretionary - Hotels, Restaurants & Leisure | Reports October 5, after the close

The Estimize consensus is looking for earnings per share of $1.10, one cent above the sell-side consensus and 10% higher than the same period a year earlier. That estimate has increased 2% since YUM’s last quarterly report. Revenue is anticipated to rise 2% to $3.5 billion. The stock is down 20% since the beginning of the year.

What to Watch: Popular fast food chain, Yum Brands, is scheduled to report Q2 earnings Wednesday, after the market closes. While the quick serve industry has rebounded in recent years, Yum’s results have been mixed. Strength in the third quarter is expected to come from strong comps from all major outlets: Taco Bell, Pizza Hut and KFC. Taco Bell has been hugely successful with its breakfast offerings while menu innovation, increased efficiency and digital initiatives have boosted Pizza Hut. KFC is steadily improving as well, on the back of renovated restaurants and healthier menu items. Yum China has been on the rebound, recording a 3% increase in system sales (excluding currency impact) and flat SSS in the second quarter.

Disclosure: Each week, Forcerank runs a variety of games covering different industries. What we have found, is that the highest ranked companies in their ...

more