On The Freight Train - How Do You Value Adidas?

I own a position in Adidas - the German athletic shoe and fashion company.

Given how well it has performed the position is nowhere near big enough.

I wish all my longs had performed this well.

But it poses a fairly typical investment problem for which I have no real answers.

--

Background

I will give you a very stylised history of how we got here.

Herzogenaurach in Germany is a funny (and small) town quite close to Nuremberg - and a couple of hours drive north of Munich.

Once upon a time two brothers started a sports shoe company (and it was successful). The brothers split up and one brother started another sports shoe company.

Those companies are Adidas (ADDYY) and Puma (PMMAF). And for a long time they considered each other the enemy.

Then along came Nike (NKE) and especially the Michael Jordan partnership and basketball shoes - and exposed Herzo for what it was - an out-of-touch German backwater.

Bluntly the fashion path in shoes was from (mostly African American) street wear, to middle-class white street wear to China (where the affluent to a surprising extent mimicked American fashion). And basketball shoes were the path to cool.

Sure there were some people I knew who went to Wharton who thought Puma was some kind of Euro-elite cool - but frankly the Germans just missed out.

I went to Herzo to visit these companies because they were super-cheap (and for no other reason).

How did I measure cheap?

These stocks were just cheap against revenue really. Nike - by far the leader - has a market cap of $85 billion down from well over $100 billion.

It has a bit of net cash (reflecting how insanely profitable it is) and about 33 billion of revenue. The price is about 2.5 times sales - but when I went to visit Herzo Nike was trading over three times sales.

By contrast Puma (which is essentially in the same business) has a market cap of €3.5 billion and sales of about the same. It is roughly 1 times sales. When I went to visit Puma was trading at about 0.6 times sales.

Relative to sales Nike had something more than five times the valuation of Puma. This gap has now closed a lot.

But then again Nike was (and remains) insanely profitable and Puma just wasn't.

Adidas was somewhere in the middle of these valuations.

If Adidas or Puma could sell shoes at something like Nike's effective margin then the German companies would go up. A lot. An insane lot. Like 5 baggers were on offer.

But then Adidas and Puma had just missed the boat. And whilst they had decent positions in European fashion (driven by strong positions in what Australians and Americans call "soccer") they had meaningless positions in America and weak positions in China.

Now fashion is not an area I have any expertise. This is obvious if you see how I dress.

So I was not likely a buyer. Just kicking the tyres.

The Puma shop in Beijing

But I still wanted to kick the tyres. After all cheap is fun - and I am a value investor. So I did make a point of walking around Puma and Adidas shops in various locations, and even counting customers vs. say local Nike shops.

Most the shops however are like shops on "Fifth Avenue". They are meant as much as anything to be brand advertising rather than to make a profit in their own right. So this is still only marginally useful research.

That said I went to the Puma flagship shop in Beijing - and - with a translator - interviewed the staff. I wrote out the impressions in an email to Michael Lämmermann, Puma's CFO - but mostly because I had his email somewhere in the system. Here is that email:

I have just come back from a work trip to China.

I wanted to leave you impressions of the Puma Shops in Beijing and Shenzhen which I spent some time looking at.

Beijing is a disaster area - very badly run by surly staff.

This is a fitness company and the staff were fat. Not obese - just pudgy - but they did not look like they used the products and they did not present an image that would sell the product.

We asked them (in Chinese) how they were employed - and it was from a local staff pool. They were Beijing locals (more expensive) but that was the end of it.

This is a country where it is legal to ask women to send in photos with their job applications and to just choose the prettiest one. Whatever - fat staff in a sporting good shop is a really bad image - and you need to fix it.

Fat and rude staff is just unforgiveable.

-

Shenzhen (Dongman district) was better. The kid behind the counter (only one of them - shop was small) looked the part - and was wearing your shoes and looked young and fit.

He was also helpful to our (very fluent) Chinese speakers in the group. However he was wearing non-Puma track clothes. Just saying.

-

For the record - I have not been convinced enough to buy your shares - but they look cheap.

This was just observation.

I did not get a reply.

And I have never touched Puma stock.

--

Enter Kasper Rorsted at Adidas

Adidas got an activist shareholder - one with a longer-than-average time horizon. This was Groupe Bruxelles Lambert - the holding company of Albert Frere and the late Paul Desmarais. I have watched GBL for some time.

GBL are soft-cooperative activists in the Northern European sense. They tend to get what they want cooperatively and slowly - often very slowly.

GBL agitated for and got a new CEO at Adidas - a Dane named Kasper Rorsted.

We knew him. And I have thought him pretty darn good for a long time. He was the longtime CEO of Henkel (a Munich based industrial glue and consumer goods conglomerate). Henkel was the second biggest stock at the foundation of Bronte Capital - and we have held it continuously. [Regrettably I sold too much on the way up.]

Kasper might not walk on water. But he is still in the top league of CEOs.

So we bought Adidas stock purely on the speculation. After all Kasper had experience in American consumer goods, was a generally good guy and the stock was cheap enough on a price to sales basis that the upside was large.

And the stock has gone up.

In all honesty I do not begin to understand what Kasper has done that has made this company better - but it sure shows in the numbers.

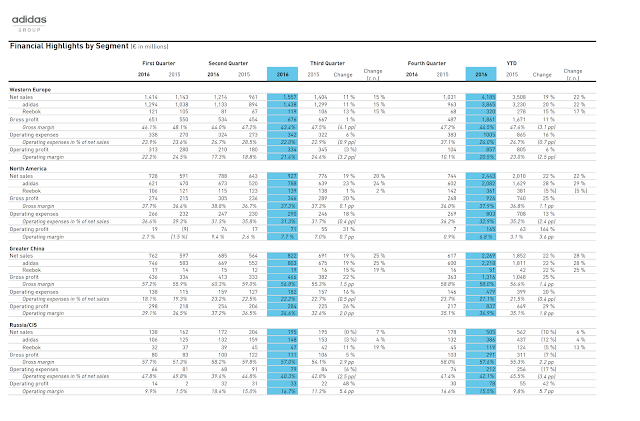

Here is an extract from the last quarterly presentation - you can find the link here:

This is a little hard to see - so I encourage you to download the original. But note really nice sales growth in all jurisdictions and sales growth above 20 percent in both the USA and China.

There is clearly a fashion element here. Adidas has a deal with Kanye re shoes. I am so out of popular culture I needed to educate myself as to who Kanye was. (No I am not joking.)

But it can't just be Kanye (as the new Michael Jordan no less) because Reebok shoes (also owned by Adidas) are having similar sales volume growth.

Whatever - Adidas is now growing explosively.

Take your 20 percent volume growth and stick into a valuation spreadsheet and see what you come up with. This sort of net present value worksheet is like Hubble telescope. Tweak the directions of various variables even a tiny bit and you wind up in a different galaxy.

So we can't value it. We have no idea.

But we own the stock. The position is still not enormous (the original holding was a suck-it-and-see speculation on the new CEO) but the position is getting bigger and bigger because the stock is doing well.

I don't want to get off the train. At least until I see something negative. So I am looking for negative. Comments wanted.

Sports rights - the new and increased negative

A re-energized Adidas is the best thing ever if you are high profile sports player looking for a shoe-deal.

There are now two rich companies wanting to put shoes on your feet and logos on your body. And that means bidding wars.

The insane war for the four big brands of Spanish football (Barcelona, Real Madrid, Ronaldo, Messi) is getting just bizarrely expensive.

This is great for people with innate ball skills (which is most certainly not me). It is bad for both Adidas and Nike shareholders. I watch in horror.

But apart from that I can't (yet) see the negatives. But then I have no fashion sense (at all) so I might be the last person to see.

Disclosure: The content contained in this blog represents the opinions of Mr. Hempton. Mr. Hempton may hold either long or short positions in securities of various companies discussed in the blog ...

more