Talking to friends and family at Thanksgiving dinner made me realize how unprepared for volatility investors are. The gathering I attended was filled with a wide mix of investors, from the young and novice interested in technology stocks and (somehow still) in Bitcoin to older, seasoned veterans. The veterans, however, didn’t exhibit much more savvy than the novices; everyone was spooked by the recent volatility.

Based on my Thanksgiving Dinner experience, here’s what I think investors need to learn now.

Re-Set Your Expectations

First, I think investors are spooked because they are being unduly influenced by the market action of 2017. But that was an unusually calm year that saw a 22% gain in the S&P 500 without a down month. That’s a Bernie Madoff-like performance — straight up every month like clockwork with no hiccup to the downside. That kind of performance usually only occurs when someone makes it up. Investors should realize that 2017 is an anomaly and that volatility is part of investing. Financial markets are rarely that smooth and stable. Do your best to expunge 2017 from your memory.

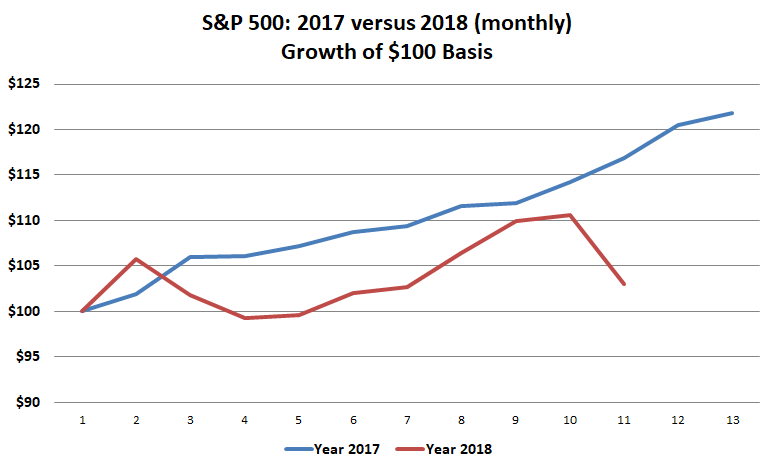

Below is a monthly chart of how the S&P 500 Index performed in 2017 and for the first 10 months of 2018. It may surprise you to see that the index was still in positive territory at the end of October. A $100 investment in the index at the start of the year was still worth more than $102 on Halloween. As of this writing (Nov. 23), the index was still in positive territory, albeit barely ((0.19% for the year, including dividends).

I don’t point out that the market is still positive to give investors encouragement to take more risk though, or to argue that markets have delivered solid returns this year. I do so in order to impress on you that large-cap U.S. stocks are still positive and that your sense of markets might be warped. This year feels awful to investors, but the returns really haven’t been bad. There’s a disconnect between the year’s returns and what the year has felt like. That’s because 2017 was so strange in the index posting positive gains for every month.

Reconsider Your Allocation

I also don’t mean to encourage investors to think they can time markets perfectly. The point is not to dance in and out of stocks adroitly, missing losses and capturing gains; it’s having an allocation that gives you enough of the upside and allows you to live with the downside without shaking you out of your investments. If the recent volatility makes you want to sell, chances are you have too much stock exposure, or you have to re-calibrate your expectations from financial markets.

I think most investors I meet with have more stock exposure than they can handle. Or at least they strike me as being badly prepared for declines either because they don’t have advisors or because they have incompetent advisors who don’t disclose risks and historical volatility. When declines come, many of them will bail out at or near the bottom despite the fact that Morningstar‘s most recent “investor return” numbers suggest investors are getting better at mistiming markets. Instead of falling into that trap you should reassess your allocation now before any damage has occurred. That’s not a prediction that a crushing decline is around the corner; I wish I could be that clairvoyant. But you should always be prepared for one. And you should have an allocation that encourages you to buy after a big market decline, not sell.

Hold Extra Cash, But Avoid Bunker Mode

Having just given all those warnings about market timing, I still think it’s fine to hold some extra cash. Every reasonable market valuation metric, including the Shiller PE and Tobin’s Q, is flashing expensive. None of these indicators are good at forecasting short-term market moves; markets can get (and have been) more expensive. But they are good are forecasting the next decade’s worth of returns. Returns will likely be low from current valuations. That means holding some extra cash is warranted. But, for goodness sake, don’t go to 100% cash with long-term assets, thinking you’ll time your reentry perfectly. The paradox of sidestepping a decline is that if the market crashes, there’s a good chance that you’ll feel so good for having missed the decline that you’ll have a lot of trouble getting back in. But 10% or even 20% more cash or shorter-term U.S. Treasuries than usual for long-term assets isn’t unreasonable either.

Comments

Log in or sign up to join the conversation.