Is It Time To Short Expedia?

Photo Credit: Viaggio Routard

Expedia, Inc. (EXPE) Consumer Discretionary - Internet & Catalog Retail | Reports April 28, After Market Closes

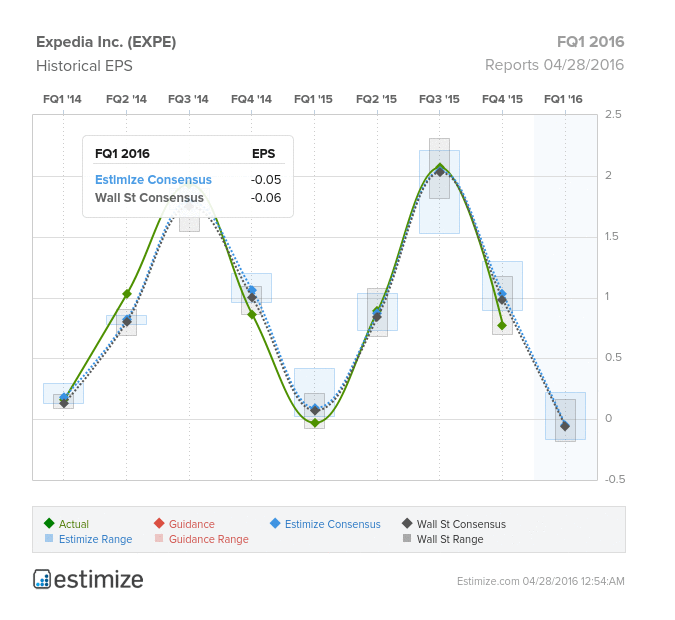

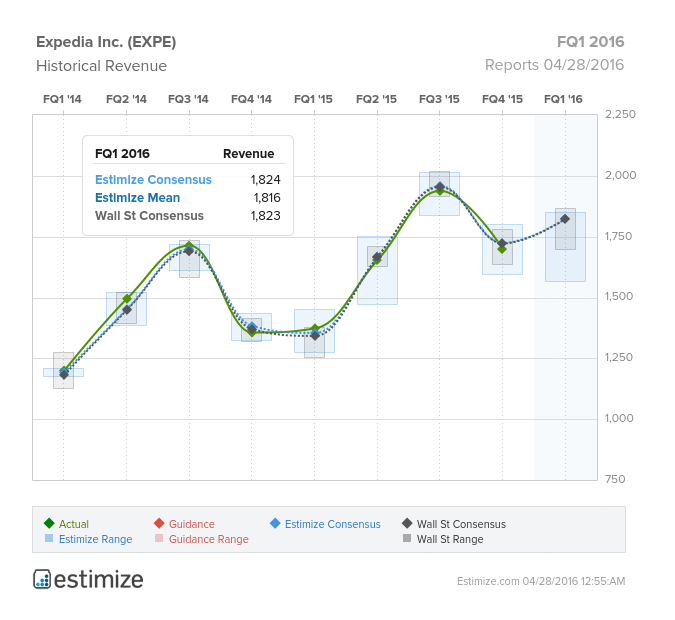

Online travel agent, Expedia, is scheduled to report first quarter earnings tomorrow, after the closing bell. The Estimize community is calling for a loss of 4 cents on $1.824 billion in revenue, slightly higher than Wall Street’s estimates -$0.06 and $1.823 billion. Expedia has missed revenue expectations in each of the previous 3 quarters. The stock has been just as poor and is down 13.3% since the start of the year.

Expedia has always had a presence internationally, but today those markets have never been more important. With expanding international trade and a rise in global travelers, Expedia has focused its efforts on increasing foreign revenues. By adding new inventories and working with local businesses, the company has a chance to benefit from travel trends abroad. Furthermore, Expedia has strategically acquired several big name European travel companies like Trivago and Venere. Both names will add to Expedia’s ever growing catalog of inventories and consolidate the online travel industry.

Customers have been raving over the Expedia Traveler Preference Program (ETP). ETP is an extension of the traditional agency business model, and allows guests to pay when checking out rather than beforehand. This avoids costly credit card processing fees and provides Expedia with a hefty commission. So far, the program has been successful in domestic markets with limited feedback from international markets.

While Expedia is focused on expanding revenue and inventories, decelerating travel trends in Europe and the U.S. has been a cause for concern. In the United States, hotel occupancy rates declined 0.6% YoY in the first two months of Q1. ADR, the metric illustrating the average realized room rental per day, was also down 3.2% over the same period. European occupancy growth was down 1.5% while ADR fell 2.6% compared to a year earlier. These dips indicate that the hotel markets in the US and Europe may be slowing down. Meanwhile, currency headwinds and stiff competition particularly from Priceline continue to be a problem for Expedia.

Disclosure: There can be no assurance that the information we considered is accurate or complete, nor can there be any assurance that our assumptions are correct.