IPO Preview: Golf Manufacturer Acushnet

Summary

Acushnet (Nasdaq:GOLF), manufactures and sells golf equipment under various brands, with the most notable being Titleist. The company is expected to IPO on Friday, 10.28.16. GOLF plans to offer 19.33 million shares at an expected price range of $21 to $24. Shares will be offered by company insiders; therefore, the company will not receive any net proceeds from the offering. Upon completion of the offering, Magnus, which is wholly-owned by Fila Korea will control 53.1% of the common stock. Fila Korea Ltd., purchased Acushnet for $1.23 billion in 2011.

Assuming GOLF prices at $22.50, the mid-point of the range, it will have a market cap value of $1.667 billion. Underwriters for the deal include: J.P. Morgan, Morgan Stanley, Nomura Securities, UBS Investment Bank, Credit Suisse, Daiwa Securities, Deutsche Bank, Jefferies, Wells Fargo Securities, D.A. Davidson, KeyBanc Capital Markets, Raymond James, and SunTrust Robinson Humphrey

Business Summary: Manufacturer and Marketer of Golf Products

Acushnet describes itself as the global leader in the design, development, manufacture and distribution of performance-driven golf products with Titleist and FootJoy brands being its most notable brands. The company operates through four divisions (2015 revenue breakdowns in brackets): Titleist Golf Balls (36%), Titleist Golf Clubs (26%), Titleist Golf Gear (9%), and FootJoy Golf Wear (28%). By geographical region, the United States accounted for 54 percent of sales, Europe accounted for 13 percent, Middle East and Africa accounted for 12 percent, and Japan accounted for 10 percent of sales for fiscal year 2015. Acushnet owns or controls the design, sourcing, manufacturing, packaging and distribution of all their products.

Executive Management Highlights

President and CEO Walter Uihlein joined Acushnet in 1976, and he was appointed to his current positions in 1995. He has served on the board since 1984. In 2005, Mr. Uihlein received the PGA of America's Distinguished Service Award.

CFO, EVP and Treasurer William Burke joined the company in 1997. His previous experience includes senior financial positions at Fortune Brands and American Brands.

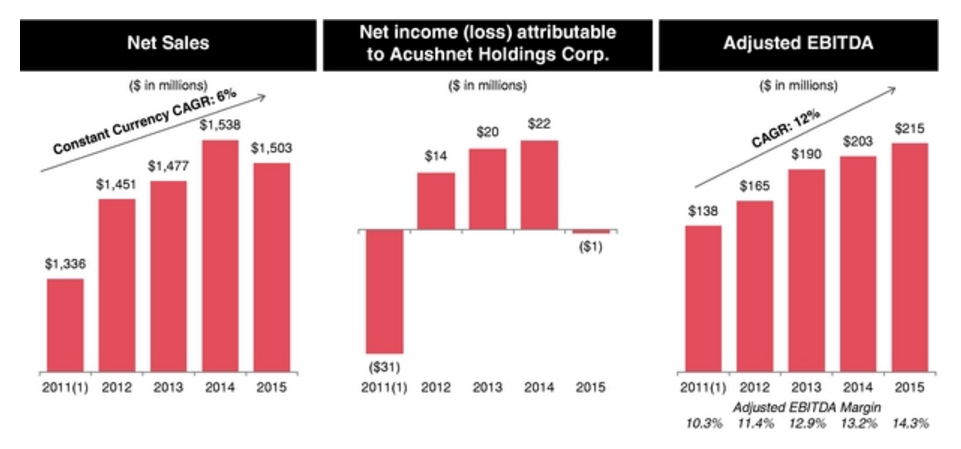

Financial Highlights - Declining Revenue in a Tough Market

Revenue dropped from $1.53B in 2014 to $1.5B in 2015, a 2.3 percent decline. The company reported a net loss of $966M for the year ended 2015.

Gross margin for the years ended December 31, 2013, 2014 and 2015 and the six months ended June 30, 2015 and 2016 was 49.6%, 49.3%, 51.6%, 52.5% and 50.9%, respectively. Operating margin for the years ended December 31, 2013, 2014 and 2015 and the six months ended June 30, 2015 and 2016 was 7.8%, 6.8%, 7.8%, 13.2% and 13.9%, respectively.

(Potential Competition: Callaway, Dunlop, TaylorMade, Ping

Using sales from the last twelve months ended June 30, 2016, GOLF would command a price/sales multiple of 1.08. This is almost in-line with Callaway (NYSE:ELY), which trades at a price/sales multiple of 1.23x with 43.28% gross margin. Callaway has a market cap of 1.00B and also designs, manufactures and sells golf clubs, golf balls, golf bags and other golf-related accessories. By comparison, GOLF trades at a lower price/sales multiple while generating a higher gross margin of 52.5%. A comparison of the two gold manufacturers is below.

|

Price/Sales |

Gross Margin |

Market Cap |

|

|

GOLF |

1.08x |

52.5% |

1.67B |

|

ELY |

1.23x |

43.3% |

1.00B |

GOLF faces competition from other companies, however tough market conditions for the golf industry has encouraged some companies in the sporting good industry to drop out of the golf equipment business. For example, Nike (NYSE:NKE) recently stopped selling golf equipment and Adidas is in the process of looking for a buyer for its TaylorMade, Adams, and Ashworth brands, all of this are focused on golf equipment.

While less competition may sound like good news for Acushnet, golf-equipment sales generally have trended down in 2016. According to a recent Golf Digest article, the sales of both woods and irons were down by 15-20 percent over the last couple of months, while ball sales have been flat.

Conclusion: Consider A Modest Allocation At Most

Declining revenue and tough market for golf manufactures make us pass on investing in this upcoming IPO.

The fact that company insiders are selling 100% of the shares and that Fila Korea will have majoring voting power are additional detractors.

Its current valuation also looks like quite a significant mark-up from Fila Korea's 2011 purchase price.

While we do hear the deal is oversubscribed, we suggest investors play golf but avoid the GOLF IPO.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

more