IPO Everspin Technologies Is A No Go

Everspin Technologies (Nasdaq:MRAM) offered 5.0 million shares (with an over-allotment option of an additional 750,000 shares) at an expected price range of $8 to $10 on Friday, Oct. 7, 2016. There is also a private placement occurring concurrently with the IPO. The company recently agreed to a private placement with GigaDevice, selling $5 million of its common stock.

The stock was repriced at a reduced price range of $8 to $10. This range is a decrease from the range of $11 to $13.

Everspin plans to use the net proceeds to make an estimated payment of $8.5 million in loans as well as other general corporate purposes. Underwriters include: Stifel, Needham & Co., Canaccord Genuity, and Craig-Hallum Capital Group.

Business Summary: Manufacturer of Magnetic-Based Random Access Memory Products

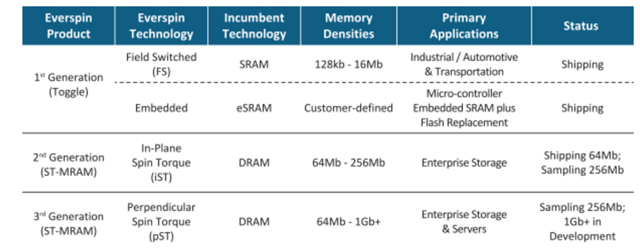

Everspin Technologies, Inc. manufactures and sells magnetic-based random access memory chips. The company was founded in 2008, is based in Chandler, Arizona and booked 26.8 million in sales for the 12 months ended June 30, 2016. The company provides its products for applications, including industrial, automotive, transportation, and enterprise storage applications.

Its products enable enterprises with the capability to design high performance systems without the need for bulky batteries. Everspin Technologies is currently the only maker of commercial MRAM products, and has sold over 60 million units over the last eight years.

The MRAM technology stores data as a magnetic state instead of an electrical charge, which is used in conventional semiconductor technology. The company's products can read and write data at fast speeds and with high endurance. Notable clients include: Honeywell (NYSE:HON), Siemens (OTCPK:SIEGY), Nikkiso, Airbus (OTCPK:EADSY), Broadcom (NASDAQ:AVGO), Dell, Lenovo (OTCPK:LNVGY), and IBM (NYSE:IBM).

(Everspin Technologies S-1/A Filing)

Executive Management Highlights

Phillip LoPresti has served as President, CEO, and board member, since June 2010. Mr. LoPresti has a long history in this industry. He previously served as Director of High Speed Data Converters for Intersil Corporation (08-10), President and Chief Executive Officer of Kenet, Inc. (06-08), and numerous roles at NEC Electronics. He received both his bachelor's and master's of science degrees in electrical engineering from Boston University.

Jeffrey Winzeler has served as CFO since April 2015. He previously served as Chief Financial Officer at Avnera Corporation, a semiconductor company specializing in analog and digital SoCs and Chief Financial Officer at Rackwise Inc., a provider of data center management software. He also held positions at: Solar Power Incorporated, International Display Works Inc. and Intel.

Use of Proceeds and Highlights From Management's Analysis

Everspin Technologies derives its revenue through the sale of its products in discrete unit form, as embedded technology, and through the licensing and royalties of its technology. The company maintains direct relationships with some clients in order to manufacture specific products according to design specifications, and it maintains a direct sales and support workforce as well.

Revenue is growing slowly, and the rate of growth is decreasing. For the six months ended June 30, 2016, Everspin Technologies generated $12.9 million in revenue, a 1.57% increase from $12.7 million generated in the last six months the previous year. Revenue generated in 2015 was $26.5 million, a 6.4% increase from 2014. Everspin has not been profitable and has generated a net loss in every year since its founding. Net loss generated in 2015 was $10.7 million, up from $7.9 million.

Potential Competition: Samsung, Toshiba, and Fujitsu

Everspin Technologies faces competition from other manufacturers of RAM products as well as other companies which are building MRAM technologies. Competitors include: Cypress (NASDAQ:CY), Advanced Micro Devices (NYSE:AMD), Avalanche Technology, Micron (NASDAQ:MU), Intel, and others.

Using price/sales multiple for the last twelve months ended June 30, 2106 ($26.8M in total revenues, market cap of $100M as noted in paragraph two), MRAM will trade at a price/sales multiple of 4.19x. The average price/sales multiple for the semiconductor business is 3.56x. Given Everspin's slow growth, significant cash burn, and lack of profitability, it is unclear why it is trading at a higher price/sales than peers.

Conclusion: Hold Off

Although the market for MRAM technology is expanding, we are skeptical on Everspin's future performance. Its slowing revenue growth, high cash burn, and slightly high price/sales multiple all give us pause.

We are also not comfortable that the price range was significantly reduced. We suggest investors avoid investing in this IPO.

Disclosure:

more