General Dynamics: Profit From Boosts To Defense Spending

When thinking about significant changes to the U.S. economy that happened in 2016, the first thing many people will think of the is Presidential Election that occurred on November 8th, 2016. Among other things, one of the significant changes after this election cycle will be the boost in military and defense spending.

What if there was a way to profit in these changes to government spending?

This post will describe how to profit from the boost in defense spending with General Dynamics (GD) – one of the nation’s largest military, defense, and aerospace companies.

Business Overview

General Dynamics was incorporated in Delaware in 1952 and grew steadily until the 1990's, when the company sold nearly all of their businesses to focus on core strategies. Since then, the company has grown organically and via the acquisition of various combat- and IT-related companies along with Gulfstream Aerospace Corporation.

Today, General Dynamics is one of the largest aerospace and military defense contractors in the world. Based on market capitalization, there are only a few companies larger than GD in the Aerospace & Defense industry:

- Boeing (BA) ($95 billion market cap)

- United Technologies (UTX) ($91 billion market cap)

- Lockheed Martin (LMT) ($73 billion market cap)

- General Dynamics (GD) ($52 billion market cap)

General Dynamics divides their operations into four main segments for reporting purposes:

- Aerospace (28% of 2015 sales)

- Combat Systems (29%)

- Marine Systems (25%)

- Information Systems & Technology (18%)

Source: General Dynamics 2015 Annual Report

Growth Prospects

Over the long-run, General Dynamics has done a fantastic job of compounding their earnings on a per-share basis.

Source: Value Line

EPS growth from $2.24 in 2000 to $9.65 in 2016 (expected) represents a CAGR of 9.6%.

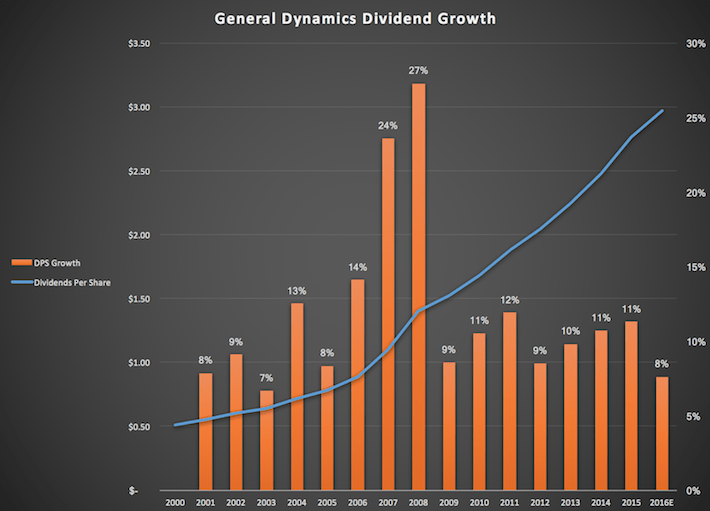

General Dynamics has also rewarded shareholders by delivering heaps of cash in the form of dividends.

Source: Value Line

The company has grown their dividend even faster than their earnings. The cumulative increase from $0.51 per share in 2000 to $2.97 per share in 2016 represents a CAGR of 11.6%. Impressive growth indeed.

Better yet, 2016 marks GD’s 25th consecutive year of dividend increases – qualifying them to become a Dividend Aristocrat in 2017. Dividend Aristocrats are elite companies that satisfy the following:

- Be in the S&P 500

- Have 25+ consecutive years of dividend increases

- Meet certain minimum size & liquidity requirements

You can view the full list of Dividend Aristocrats here. With that said, GD hasn’t ‘officially’ been added to the Dividend Aristocrats List yet. For now, the company is a Dividend Achiever – one of 273 stocks with 10+ years of rising dividends.

Going forward, there are numerous drivers of growth for General Dynamics. This will ensure that adequate returns will continue for investors in the future.

First of all, the defense industry is expected to be one of the largest beneficiaries of the new Trump administration. The President-Elect's policies are expected to include significant budget boosts to national defense, surveillance and intelligence products, which are all positive for General Dynamics.

This has been reflected in GD’s stock price since the election results were announced.

General Dynamics stock has surged since the November 8 Presidential Election.

Beyond that, General Dynamics’ growth will occur through a mix of new government contracts and business with private sector counterparties.

In quarterly press releases, General Dynamics always lists new significant orders. Taking a look at their significant orders (in millions) for their Combat Systems segment for third quarter:

- $170 from the U.S. Army for the production of Hydra-70 rockets.

- $165 from the Army to produce various calibers of ammunition and ordnance.

- $145 from the Swiss government to produce Piranha armored vehicles equipped with mortar systems.

- $100 from the Army for Abrams M1A2 System Enhancement Program (SEP) components and associated program management.

- $75 to provide munitions to the government of Israel.

- $55 from the Army for Abrams technical support and engineering services.

- $40 for technical assistance with Abrams tank kits for Egypt.

- $35 from the U.S. Marine Corps for the reset of Cougar vehicles.

Noting that this is only for one quarter and business segment, it appears that business continues to boom for this soon-to-be Dividend Aristocrat.

Competitive Advantage & Recession Performance

As a defense contractor, General Dynamics deals with counterparties such as the U.S. Navy, the U.S. military, and the U.S. Marine Corps. Earnings are based on long-term contracts which reduces their earnings volatility.

In fiscal 2015, U.S. Government contracts represented 57% of their total revenues.

Source: General Dynamics 2015 Annual Report

General Dynamics also has a long backlog of business which has been contracted but not yet completed or paid for. Their ~$52 billion backlog at the end of fiscal 2015 is much higher than fiscal 2015’s $31 billion of revenues.

Source: General Dynamics 2015 Annual Report

This means that in theory, General Dynamics could continue to operate even if they fail to write new business (which is unlikely).

This backlog is also quite stable over time.

Source: General Dynamics 2015 Annual Report

All factors considered, the business model of General Dynamics lends itself well to investment from the risk-conscious investor. This was reflected in the company’s performance during the 2008-2009 financial crisis. Here is a snapshot of their EPS:

- 2007: $5.10

- 2008: $6.13 (20.2% increase)

- 2009: $6.20 (1.1% increase)

- 2010: $6.82 (10.0% increase)

- 2011: $6.94 (1.8% increase)

General Dynamics did not experience a single year of negative earnings growth during the financial crisis. This is a testament to the ability of this stock to weather recessions.

Valuation & Expected Returns

General Dynamics’ consensus earnings per share estimate for fiscal year 2016 is $9.65. Based on the December 30th closing price of $172.66, this means that GD is currently trading at 17.9 times 2016’s earnings.

The following diagram displays how this is above GD’s historical valuation levels.

Source: Value Line

The stock should eventually fall to a more normalized level, and this will be a detractor from future shareholder returns. Value-conscious investors might be better off waiting for a better entry point.

Other than changes in valuation, General Dynamics shareholder returns will be composed of share buybacks, dividend yield, and earnings growth.

General Dynamics has been a steady repurchaser of stock over recent years. In fiscal 2015 alone, the company repurchased $3.2 billion of stock, representing approximately 6% of today’s market cap. Since 2012, the company has reduced their number of shares outstanding by 12%, an impressive feat.

Buybacks are currently slowing down for General Dynamics. The company repurchased only 3.2 million shares for $348 million in Q3 and year-to-date, the share repurchase program has been roughly cut in half from the year before.

Never the less, share repurchases will still be a contributor to future shareholder returns.

The company has a current dividend yield of ~1.7%, which although not particularly high, has plenty of room to grow. Based on 2016’s expected numbers, General Dynamics is paying $2.97 in dividends from $9.65 of earnings for a payout ratio of 30.8%. This leaves plenty of upside for income-oriented investors.

The company has a long-term goal of double-digit earnings growth, which combined with their historic 9.6% EPS CAGR makes me comfortable expecting EPS growth in the range of 7%-9%. This will be boosted by share buybacks.

Overall, total shareholders returns for General Dynamics are expected to be in the range of 8.7%-10.7%, consisting of the following:

- 1.7% dividend yield

- 7-9% earnings growth (boosted by share buybacks)

These are maximum estimates, though, and will almost certainly be reduced by future contraction of the stock’s valuation.

Final Thoughts

General Dynamics operates in an industry with a wide economic moat and a distinct competitive advantage. These are Buffett-esque qualities that should be appreciated by investors.

“The key to investing is not assessing how much an industry is going to affect society, or how much it will grow, but rather determining the competitive advantage of any given company and, above all, the durability of that advantage.”

– Warren Buffett

They also pay a rising dividend with a low payout ratio and steady earnings growth.

The company has an above average rank using The 8 Rules of Dividend Investing. Despite this, General Dynamics is trading above historical valuations. Investors might be better off to wait for an attractive entry point to invest in this great business.

Disclosure:

Sure Dividend is published as an information service.It includes opinions as to buying, selling and holding various stocks and other securities.

However, the publishers of ...

more