Discount Carriers Hurting United Airlines Profitability

United Continental Holdings (UAL) Industrials - Airlines | Reports January 17, After Market Close

Key Takeaways

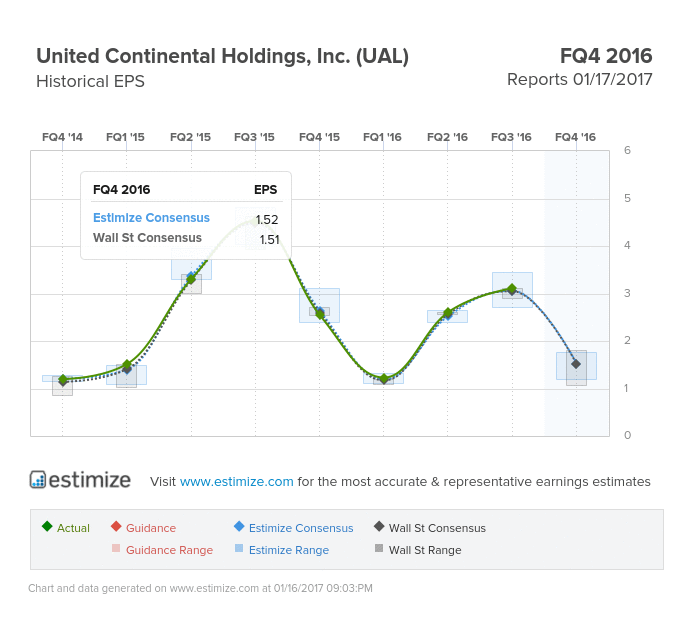

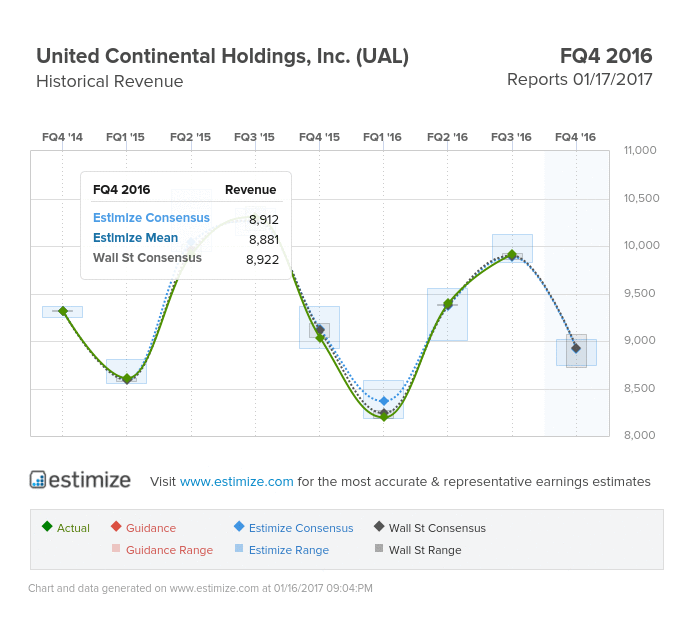

- The Estimize consensus is calling for earnings per share of $1.52 on $8.91 billion in revenue, 1 cent below Wall Street on the bottom line but right in line on the top

- United Continental recently raised its target PRASM range to down 1.25-1.75% from a decline of 3 to 4%

- Steadily rising fuel costs plus macroeconomic uncertainty poses a threat to high margin international flights

- What are you expecting for UAL?

Airline earnings season is officially underway and going by Delta’s results, other major airlines can expect to hit some turbulence. Delta announced better than expected revenue for the fourth quarter but fell short of analyst’s estimates on the bottom line. Sales figures benefited from lower fuel costs, improving travel trends and greater promotional and discounting campaigns. But discounting also put a damper on margins especially for large airlines which traditionally rely on overpriced flights. Don’t be surprised if United falls into a similar trap when it announces fourth quarter results tomorrow morning.

Analysts at Estimize expect United to post $1.52 per share on the bottom line, reflecting a 43% decline from a year. That estimate increased by 14% since the company’s most recent report in October. Revenue for the period is expected to decline by 2% to $8.91 billion, marking a significant improvement from previous reports in fiscal 2016. The stock typically does its best in the month following an earnings report, increasing by an average of 4%.

Like the other airlines, United reports operational performance on a monthly basis. Its most recent reports declared December 2016 traffic increased by 2.6% on a 2.6% increase in average seat miles, compared to a year earlier. The company also took the time to raise guidance on key PRASM metrics from a decline of 3-4% to 1.25-1.75%. The bullish revisions reflect a stronger close in bookings, low fuel costs, and improving traffic trends.

United’s promotion activity, especially its member loyalty, continues to play a large role in its recent success. In fact, United was recently deemed to operate the best overall frequent flyer program in the world for a thirteenth straight year.

Some near term risks to another bullish report include currency headwinds, slowly rising fuel costs, macroeconomic uncertainty and increased competition. JetBlue, Spirit and Southwest pose a legitimate threat to major airlines market share by offering tickets at more attractive price points. Meanwhile, the strength of the U.S. dollar and increasing turmoil overseas could hamper performance in international operations.

![]()

Disclosure: None.