“Bre-lief” – Central Banks To The Rescue

Happy “Independence Day”

Ronald Reagan once wrote:

“There is a legend about the day of our nation’s birth in the little hall in Philadelphia, a day on which debate had raged for hours. The men gathered there were honorable men hard-pressed by a king who had flouted the very laws they were willing to obey. Even so, to sign the Declaration of Independence was such an irretrievable act that the walls resounded with the words ‘treason, the gallows, the headsman’s axe,’ and the issue remained in doubt.

The legend says that at that point a man rose and spoke.

‘They may turn every tree into a gallows, every hole into a grave, and yet the words of that parchment can never die. To the mechanic in the workshop, they will speak hope; to the slave in the mines, freedom. Sign that parchment. Sign if the next moment the noose is around your neck, for that parchment will be the textbook of freedom, the Bible of the rights of man forever.’

The 56 delegates, swept up by his eloquence, rushed forward and signed that document destined to be as immortal as a work of man can be. When they turned to thank him for his timely oratory, he was not to be found, nor could any be found who knew who he was or how he had come in or gone out through the locked and guarded doors.

Well, that is the legend. But we do know for certain that 56 men, a little band so unique we have never seen their like since, had pledged their lives, their fortunes and their sacred honor. Some gave their lives in the war that followed, most gave their fortunes, and all preserved their sacred honor.”

All people want is to be in a place where they can improve their lives. Where their children can have a brighter future than they did. The system in England did not provide that. The revolution was born from economic frustration, oppression, and depression.

240 years later America has descended into much of the same extractive system as Europe. There’s a tiny elite showering itself with free money and political favors at the expense of everyone else. Meanwhile, America continues down its path of more debt, more money printing, more regulations, and less freedom. How long can this go on without consequence?

As you celebrate your “4th of July” holiday, it is worth remembering the sacrifices made by those 56 men who signed the declaration of America’s birth.

“We hold these truths to be self-evident, that all men are created equal, that they are endowed by their Creator with certain unalienable Rights, that among these are Life, Liberty, and the pursuit of Happiness.”

Giving up freedoms in the name of national security, political correctness, and social equality were not the intentions of our founding fathers. Nor should they be yours.

Happy “Independence Day!”

Market Outlook Presentation

A copy of last week’s Webinar: Summer Market & Investing Outlook

Round Trip Ticket

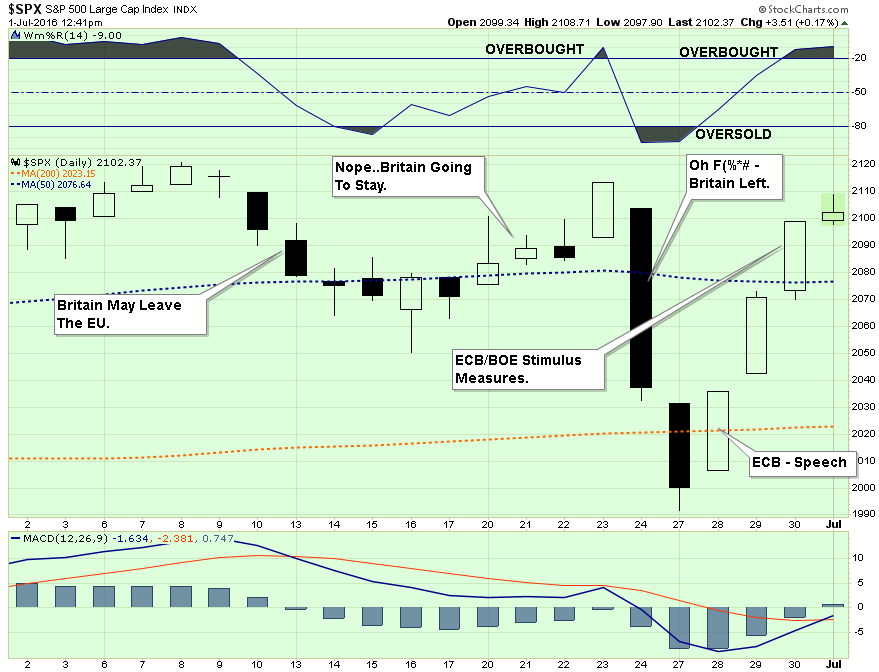

In this past weekend’s commentary, I discussed the likelihood of Central Bankers leaping into action to stabilize the financial markets following the British referendum to leave the E.U. To wit:

“Of course, the reality is that we will likely see a globally coordinated Central Bank response to the financial markets over the next few days if the selling pressure picks up steam. This will come in the form of:

- Further interest rate reductions

- Deeper moves into negative rate territories

- Increased/accelerate bond purchases by the ECB

- A potential short-term QE program by the Federal Reserve

- A pick up of direct equity/bond buying by the BOJ.

- Liquidity supports through FX swaps or direct intervention

- Lot’s and Lot’s of “Verbal Easing”

Not to be disappointed, Mario Draghi sprung into action on Tuesday suggesting a greater alignment of policies globally to mitigate the spillover risks from ultra-loose monetary measures.

“We can benefit from the alignment of policies. What I mean by alignment is a shared diagnosis of the root causes of the challenges that affect us all; and a shared commitment to found our domestic policies on that diagnosis.” – Mario Draghi at the ECB Forum in Sintra, Portugal.

Furthermore, as noted by John Plassard, a senior equity-sales trader in Geneva at Mirabaud Securities via Bloomberg:

“Stocks are rebounding on the expectation that there will be a coordinated intervention by central banks. What central banks can do is put confidence back in the market by telling everyone that they are here and ready to act. If we don’t get that sort of support, we’ll see further declines.”

Then on Thursday more announcements came from both the Bank of England and ECB:

- BOE: SOME MONETARY POLICY EASING LIKELY OVER SUMMER

- BOE: MPC WILL DISCUSS FURTHER POLICY INSTRUMENTS IN AUG

- ECB: TO WEIGH LOOSER QE RULES AS BREXIT DEPLETES ASSET POOL

- ECB: OPTIONS TO INCLUDE MOVING AWAY FROM QE CAPITAL KEY

- ECB: CONCERNED ABOUT SHRINKING POOL OF ELIGIBLE DEBT

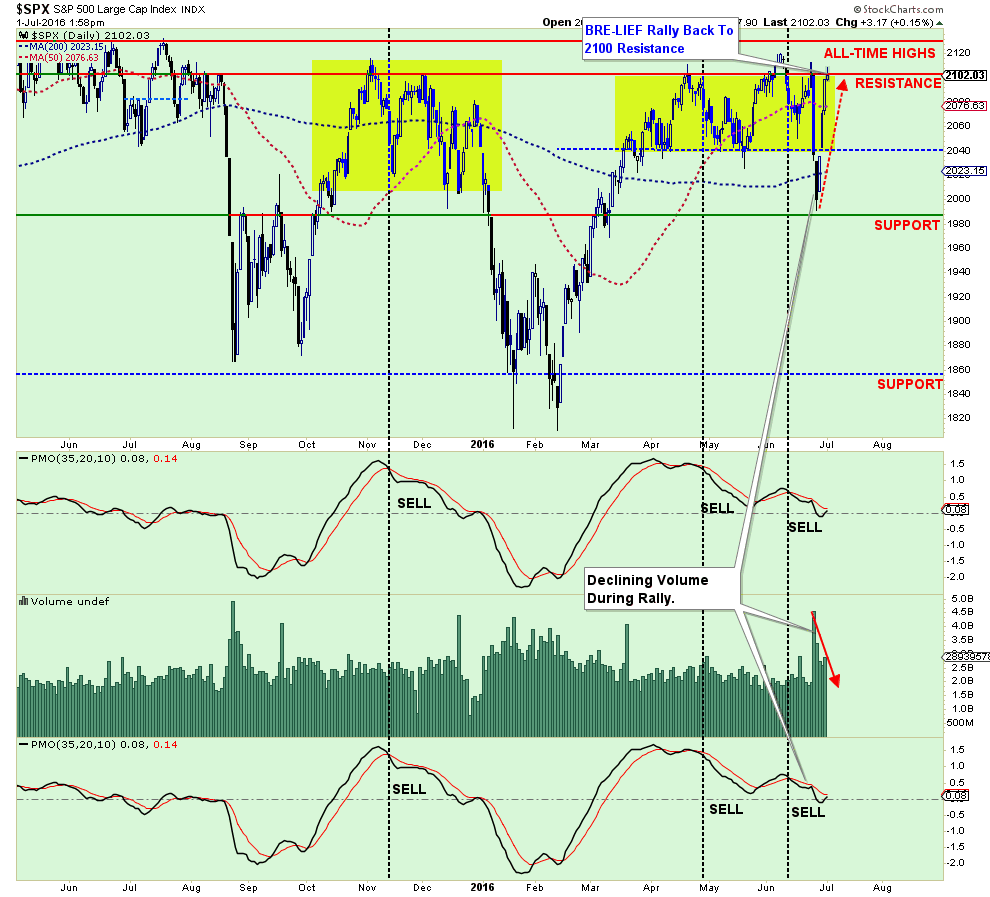

While many had predicted a market crisis of magnitude stemming from the “Brexit” vote, the reality was a 100-point swing in the markets in just one week. No matter how you bet, you were probably wrong.

So, yes, from “Brexit Fears” to “Brexit MEH” in just one week. Talk about volatility.

STILL DO NOTHING

However, this is why over the last few weeks I have continued to recommend “Doing Nothing” in portfolios.

“There are times in portfolio management where ‘doing nothing’ is better than ‘doing something.’This is one of those times.

With portfolios already running at just 50% of total recommended equity exposure, portfolio risk is already substantially mitigated. This leaves us is the best place to be for the moment as we await the outcome of the ‘Brexit’ vote on Thursday and the culmination of Yellen’s testimony on the ‘Hill.’

From that vantage point, we can then assess the markets and make a reasonable assumption about what to do next. Could we miss a bit of upside? Absolutely. But such a small lag is a much better outcome than trying to recoup a substantial loss if things go wrong.”

However, the problem is we remain trapped in limbo. With the markets holding above supports, but still within an overall corrective topping process, there is no reason to become extremely negative on the markets at the moment OR be extremely bullish.

In other words, the only option is to continue to “do nothing” until the market resolves its current state in one direction or another.

The bad news is the longer the market remains in this current state, the risk are rising of a more substantial downside break.

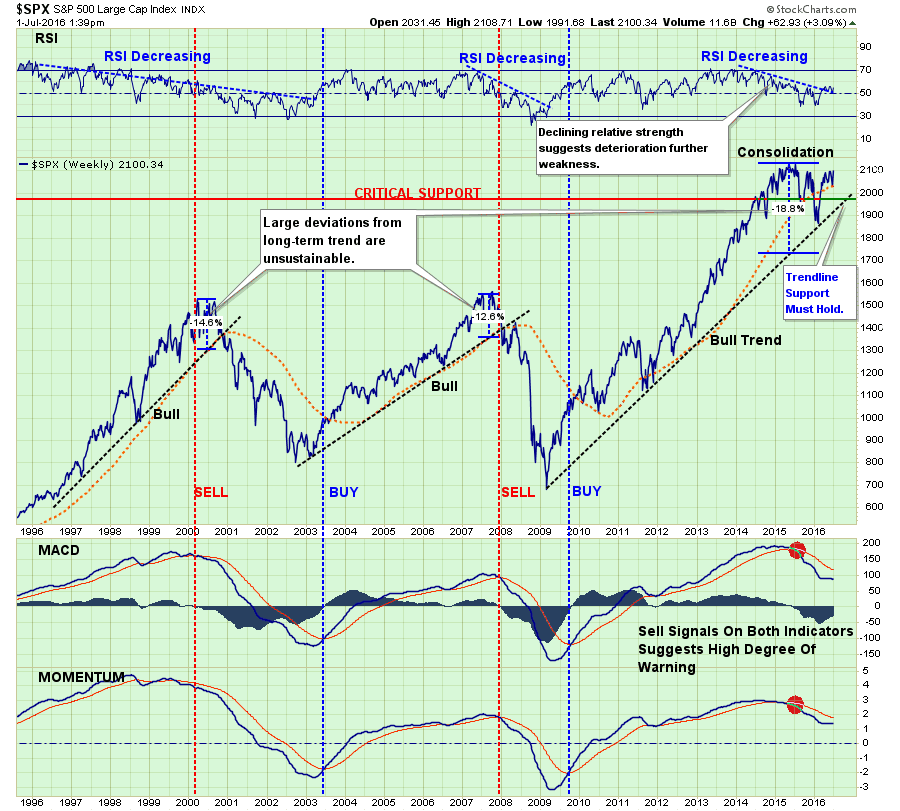

As I have discussed many times previously, the current topping process, stuck below “all-time” highs, is not too dissimilar to what has been seen at previous major bull market peaks.

However, importantly, the long-term bullish trend remains intact. This is why the focus on 1990 as support is so critical. A break of that level would signify the completion of the market topping process and an entry into a full-fledged bear market correction.

Conversely, a breakout above all-time highs would signify a continuation of the current bull-market. While such a breakout is feasible given the reassurance of further Central Bank interventions, it will be increasingly harder to justify higher valuations given the ongoing deterioration in the earnings and economic backdrops.

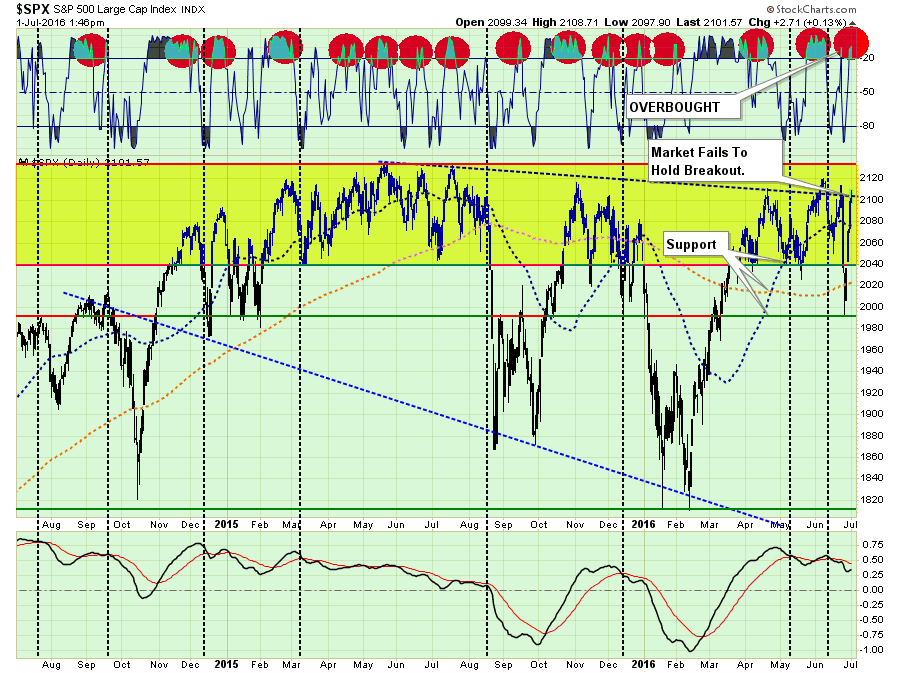

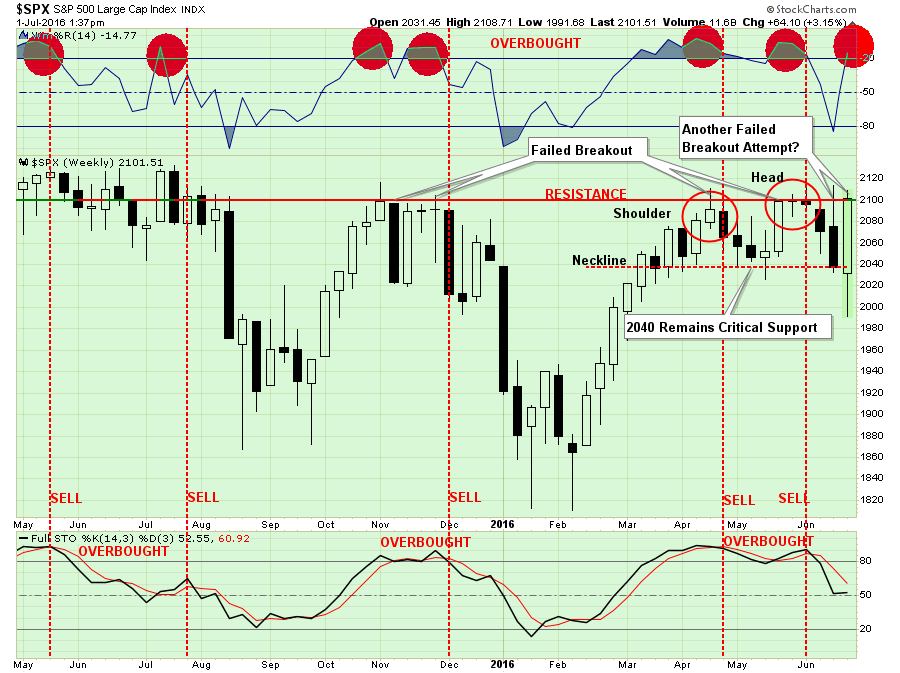

For now, as has been repeatedly discussed over the past few weeks, the markets remain trapped within the ongoing range of 2040 to 2135.

The vertical dashed lines are “momentum sell signals.” Even with the massive surge this past week, there was not enough pickup in price momentum to reverse the current “sell signal.” Such suggests, with the markets now back to overbought on a short and intermediate-term basis, there is little buying power available to push stocks substantially higher. The chart below shows the same issue on a weekly basis.

As shown below, while price action has certainly been “exciting” of the last week, which is only getting investors “back to even,” volume has been lacking.

All evidence continues to suggest the current rally will likely fail in the short-term. But given the resilience of the markets in the short-term, and the credence given to ongoing Central Bank support, it remains important to not become overly bearish in the short term.

However, given the extremely low risk/reward environment for investors at the moment, it is also not advisable to become overly bullish until the fundamental and economic backdrop improves markedly.

PORTFOLIO ACTIONS (Reprisal)

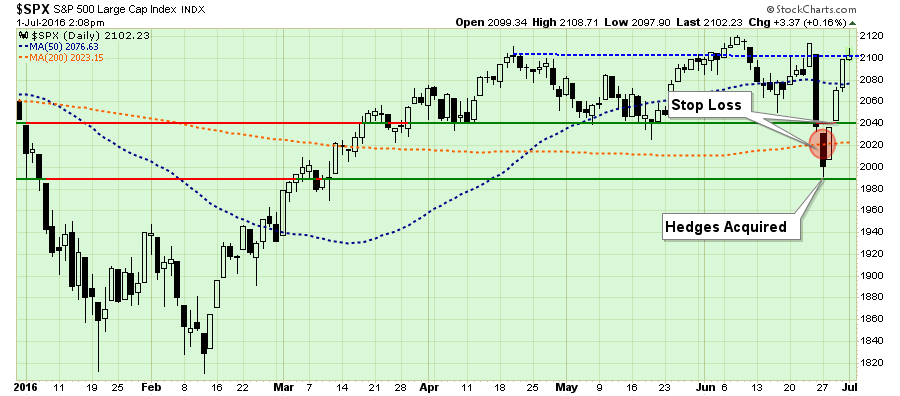

Given the technical backdrop of the market this week, the rally over the last several days has returned the markets back to upper resistance levels and pushing into overbought territory.

If you have not taken any actions over the last few weeks, this is a good opportunity to clean up and reduce excess risk in portfolios.

Continue with the steps laid out in the “Monday Morning Call” Section a few weeks ago:

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against major market declines.

- Take profits in positions that have been big winners

- Sell laggards and losers

- Raise cash and rebalance portfolios to target weightings.

Next, as shown in the chart below, tighten up “stop loss” levels and have a strategy to hedge equity risk in portfolios in the event the market breaks down.

Last week, I stated:

“While the 2040 level was “technically” broken on Friday, I recommend waiting until next week before liquidating positions. With the markets now very oversold on a short-term basis, a bounce early next week would not be surprising. Use any bounce to rebalance portfolios.”

Waiting for a confirmation of the break of 2040 proved prescient given the conditions present at that time.

Given the depth of the recent decline, the trading range has been expanded from 2100 to 1990. Therefore, I am adjusting the hedging level to the bottom of the trading range to reduce the potential for a “whipsaw” effect of another short-term “sell-off.” Therefore, I am moving the level where a “negative market (short) hedge” is added to portfolio down to 1990 from 2020 last week.

T.I.N.A. IS B.S.

I liked this note from Doug Kass this week:

“I also reject the idea that stocks are ‘attractive’ because they’re cheap relative to bonds right now.

This is known as ‘T.I.N.A.’ — ‘There Is No Alternative’ to stocks — but I don’t buy it. If bonds are overvalued, where does that leave stocks?

Or how about another ‘relative’ notion — that U.S. stocks are the ‘best house in a bad neighborhood’ when compared to foreign equities? If non-U.S. economies are problematic and their share prices vulnerable, I think that argument holds little water in our flat and interconnected global economy.”

His point is well made. Stocks DO NOT preserve capital, bonds do. Even if interest rates do reverse for some reason, while bond prices may fall, the corpus is still returned to the investor at maturity along with all interest payments along the way. Such is not the case for equities.

Eventually, even the best house in a bad neighborhood is eventually devalued. Global low to negative interest rates are not a function of financial market strength but rather global economic weakness. There is only one way this ends which is badly.

But for now, the party rages on with little regard for the consequences of partying too long or too loudly. There are always a few who leave the party too early, but the consequences are substantially worse for those who stay too long.

“There is nothing riskier than the widespread perception that there is no risk.”– Howard Marks

THE MONDAY MORNING CALL

The Monday Morning Call – Analysis For Active Traders

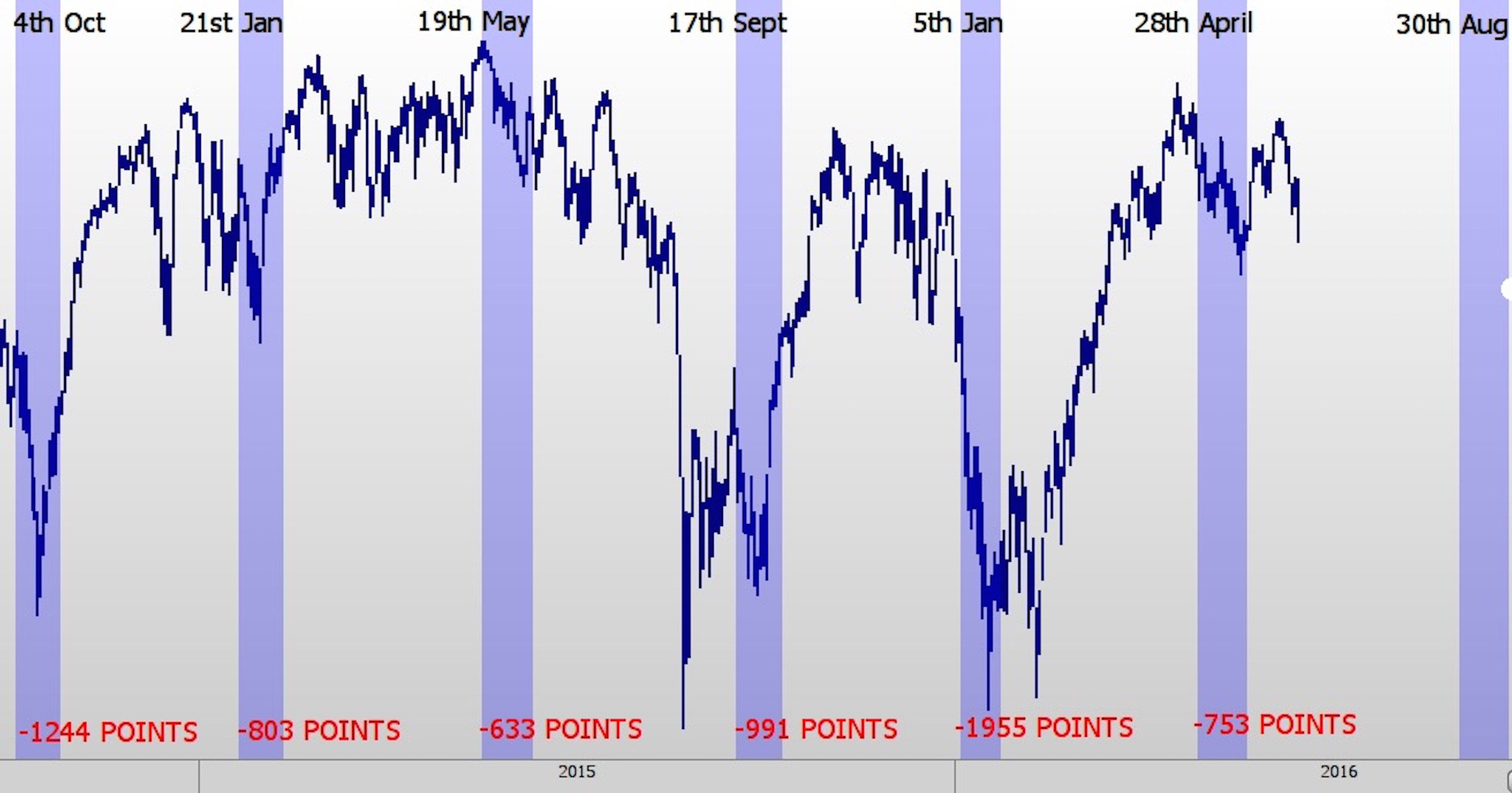

BEWARE AUGUST

Art Cashin delivered some great comments on CNBC stating:

“Not at all, I think the only thing I heard from him was a mild frustration that they couldn’t get things going. The market is more powerful than the Fed, that’s the problem.“

Of course, it was Sandy Jadeja, a technical analyst and chief market strategist at Core Spreads, that caught my attention just recently. He predicted that we are in for some big bumps on the road to 2018.

“We are currently in a very dangerous time zone between 2011 until 2018. This is an 84-year cycle [called the ‘Time Cycle’] and the previous cycle appeared during 1928 until 1934 where the Great Depression took place.”

Take a look at this chart:

“This exact same cycle is what we are in right now. And so I am worried that we could see a potential threat to our economy in the current ‘Time Cycle’ we are witnessing right now.

We have a situation. This lasts until 2018 for this particular cycle. And my worry is that we could see sudden sharp declines take place and tripping investors if they are not prepared.”

Jadeja is convinced that the sudden declines will take place on three dates:

- between August 26 and August 30,

- September 26, and;

- October 20, 2016

He has been deadly accurate previously, so I wouldn’t entirely dismiss his views. I have bookmarked these dates and will follow up when we get closer to these periods.

No Change To Allocations (Again)

The inability for the markets to advance, but having not yet violated important support levels, keeps portfolio allocation models once again unchanged.

Please review the portfolio management rules discussed a few weeks ago which guide the investment process in my shop. It is through following these basic rules that, with the markets overbought, underlying fundamentals and economics deteriorating, and profits still weak, that I continue to suggest some portfolio actions be taken to reduce, not eliminate, overall risk as noted above.

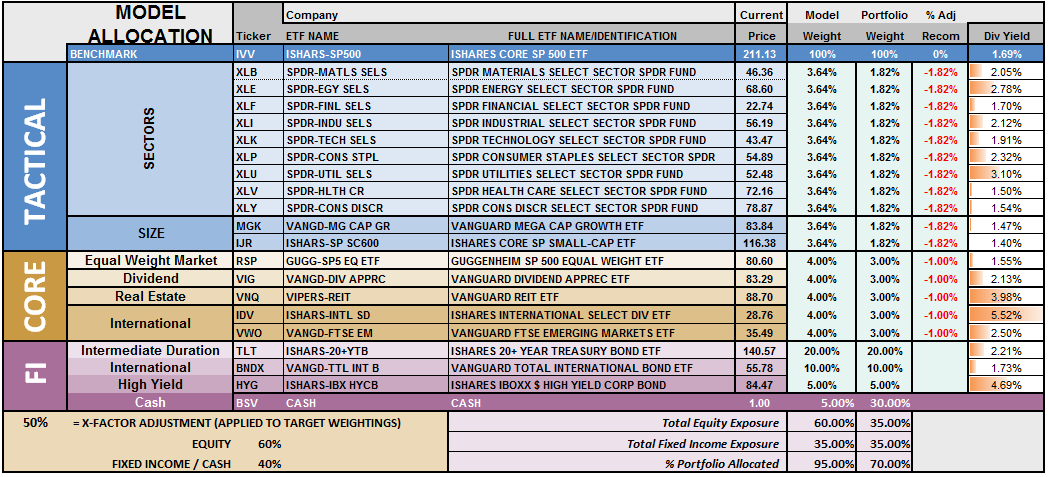

S.A.R.M. Model Allocation

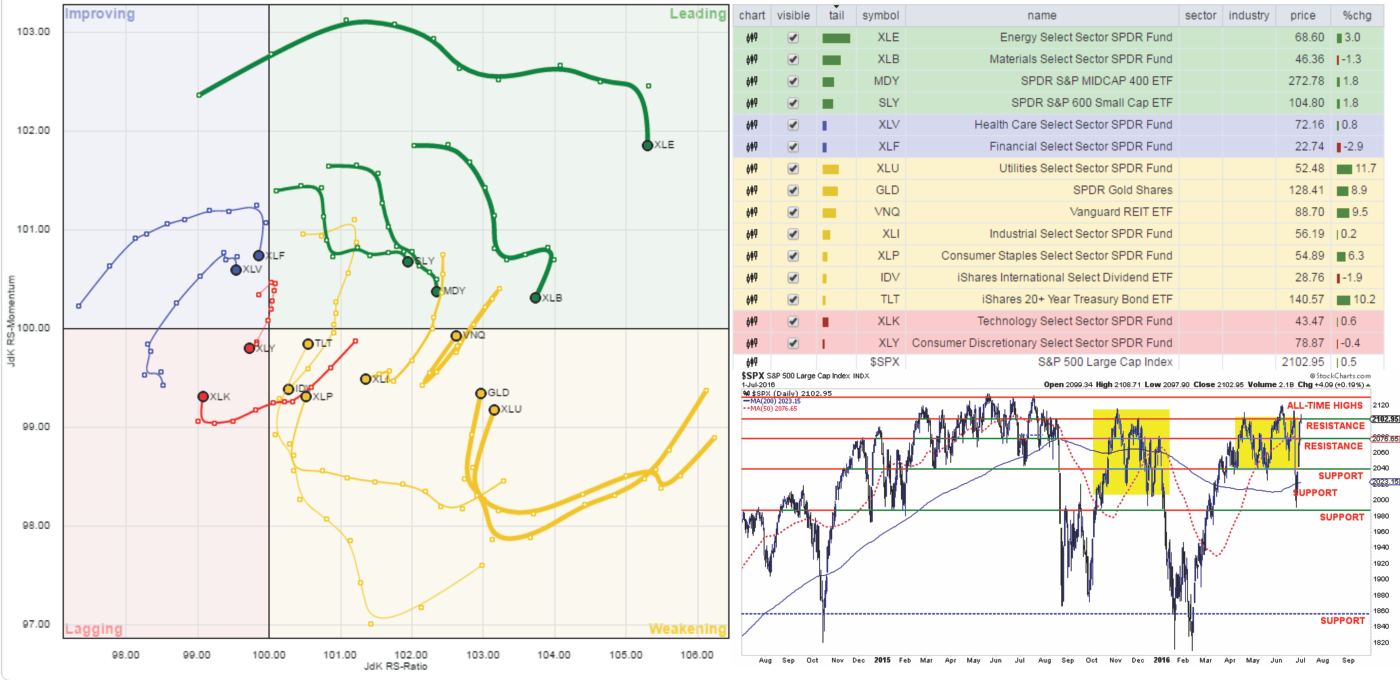

The Sector Allocation Rotation Model (SARM) is an example of a basic well-diversified portfolio. The purpose of the model is to look “under the hood” of a portfolio to see what parts of the engine are driving returns versus detracting from it. From this analysis, we can then determine where to overweight sectors which are leading performance, reduce in areas lagging, and eliminate those areas that are dragging.

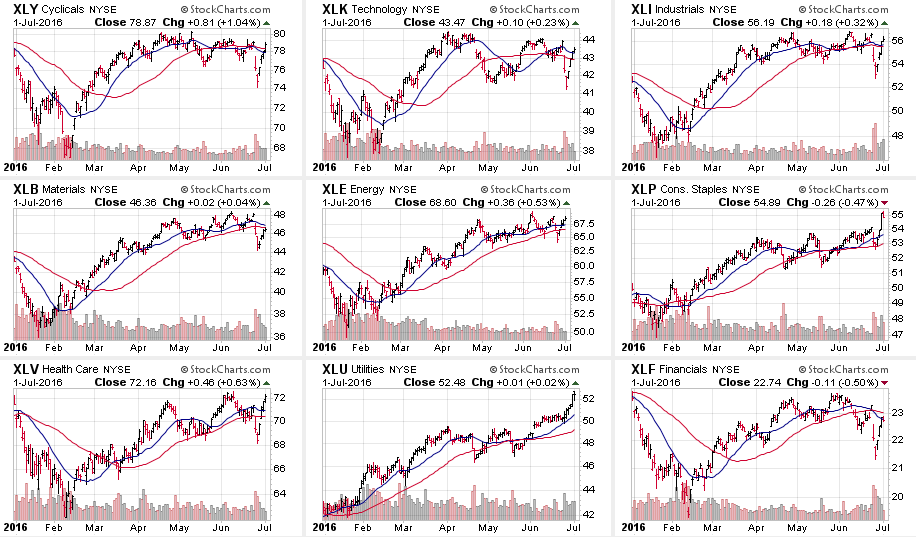

This past week’s volatility didn’t change the backdrop of the market much. However, it is worth noting that the leadership of energy, basic materials, small and mid-cap is fading along with the relative performance of healthcare and financials.

The sector recommendations over the last two weeks, shown below, paid off handsomely during this past week’s wild ride. With some extra cash in hand, laggards reduced, portfolio volatility was well reduced relative to the markets.

LEADING BUT WEAKENING: Energy, Materials, Mid-cap and Small-cap

IMPROVING BUT WEAKENING: Financials and Health Care

LAGGING BUT IMPROVING: Utilities, Gold, Bonds, REIT’s and Staples

LAGGING & WEAKENING: Discretionary, Technology, International & Industrials

The sector comparison chart below shows the 9-major sectors of the S&P 500.

The “Brexit” sell-off was seen across all sectors of the market with the exception of Utilities and Staples. Both of these sectors are EXTREMELY OVERBOUGHT and profit taking is strongly advised.

The hardest hit sector was Financials as potential debt default concerns rose, however, Matericals, Healthcare, Technology, Discretionary and Industrials were all punished. But, by Friday, the damage has been mostly reversed.

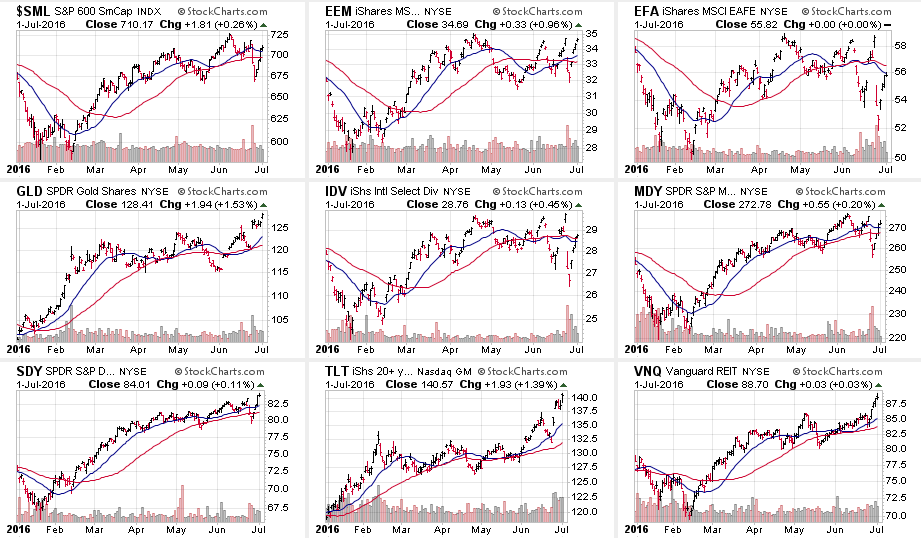

In other major markets and asset classes, International and International Dividend Yielding markets were the hardest hit last week along with Small-Cap, Mid-Cap, Emerging Markets. Like the S&P above, the majority of the damage has been reversed.

On a short-term basis, bonds, REIT’s and gold are pushing extreme levels of deviation, profit taking at these levels would be strongly recommended.

As I stated two weeks ago:

“We saw the early stages of deterioration in leadership in Small and Mid-Cap stocks last week, so profit taking would be suggested.“

That proved very prescient. I suspect we are about to see the same rotation in bonds, REIT’s, Gold, Utilities & Staples so, again, profit taking and rebalancing is advised.

S.A.R.M. Sector Analysis & Weighting

The current risk weighting remains at 50% this week. The failure to maintain the breakout above 2100 holds allocation changes for now. With technical underpinnings still “bullishly biased,” we want to give the markets the benefit of the doubt for now. However, with those technical underpinnings deteriorating, risk has risen markedly.

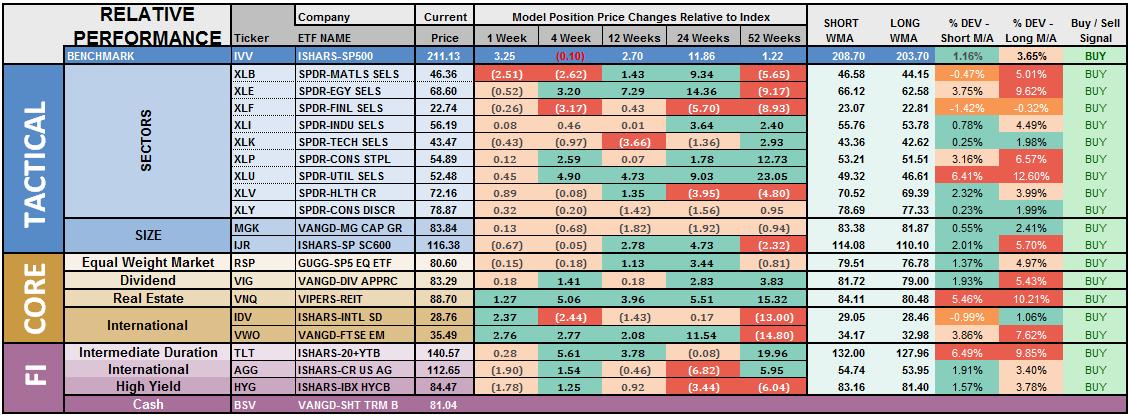

Relative performance of each sector of the model as compared to the S&P 500 is shown below. The table compares each position in the model relative to the benchmark over a 1, 4, 12, 24 and 52-week basis.

Historically speaking, sectors that are leading the markets higher continue to do so in the short-term and vice-versa. The relative improvement or weakness of each sector relative to index over time can show where money is flowing into and out of. Normally, these performance changes signal a change that last several weeks.

The last column is a sector specific “buy/sell” signal which is simply when the short-term weekly moving average has crossed above or below the long-term weekly average. The number of sectors on “buy signals” has improved from just 2 a few weeks ago to 19 this past week.

The risk-adjusted equally weighted model remains from last week. No changes this week.

The portfolio model remains at 35% Cash, 35% Bonds, and 30% in Equities.

As always, this is just a guide, not a recommendation. It is completely OKAY if your current allocation to cash is different based on your personal risk tolerance, time frames, and goals.

For longer-term investors, we need to see an improvement in the fundamental and economic backdrop to support a resumption of the bullish trend. Currently, there is no evidence of that occurring.

THE REAL 401k PLAN MANAGER

The Real 401k Plan Manager – A Conservative Strategy For Long-Term Investors

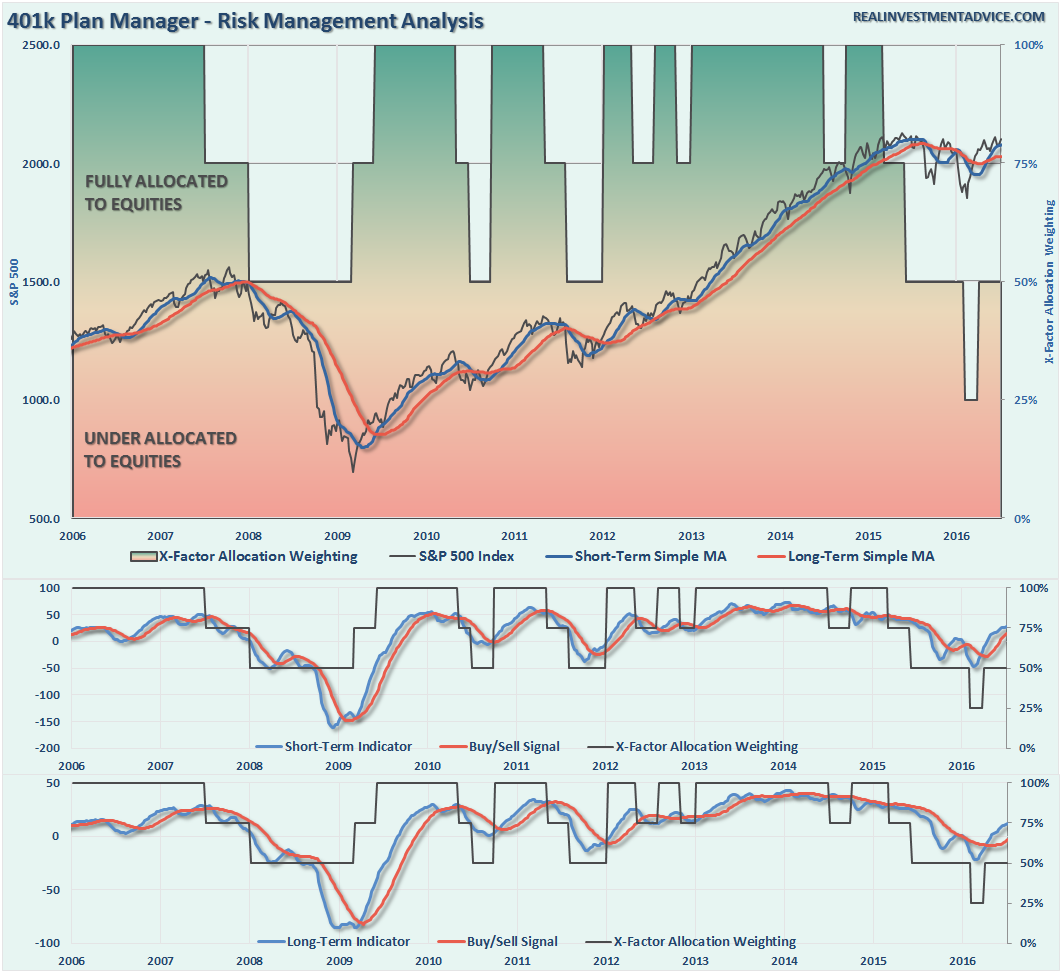

NOTE: I have redesigned the 401k plan manager to accurately reflect the changes in the allocation model over time. I have overlaid the actual model changes on top of the indicators to reflect the timing of the changes relative to the signals.

There are 4-steps to allocation changes based on 25% reduction increments. As noted in the chart above a 100% allocation level is equal to 60% stocks. I never advocate being 100% out of the market as it is far too difficult to reverse course when the market changes from a negative to a positive trend. Emotions keep us from taking the correct action.

“Bre-lief”

As discussed in the main section of the newsletter, the surprise “Brexit” last Thursday sent the markets plunging on Friday. While “bulls” were sent scrambling for cover, the overweight cash and fixed income holdings protected 401k plans reduced volatility. However, as I stated, Central Banks launched into action last week provided a short-term“relief” surge to the market effectively putting plans back where they were before all this happened in the first place.

However, the technical underpinnings, while still bullishly biased at the moment, are beginning to show more substantial deterioration. That, combined with the failure of the market to breakout about 2100, again, keeps allocation models on hold, again, this week. In other words, we remain in “limbo” and frustratingly so.

Once again, the risk/reward remains unbalanced does not justify taking on additional equity risk in the model.

For longer-term investors, the markets have made virtually no progress since January of 2015. Therefore, there is little evidence to suggest stepping away from a more cautionary allocation…for now.

If you need help after reading the alert; don’t hesitate to contact me.

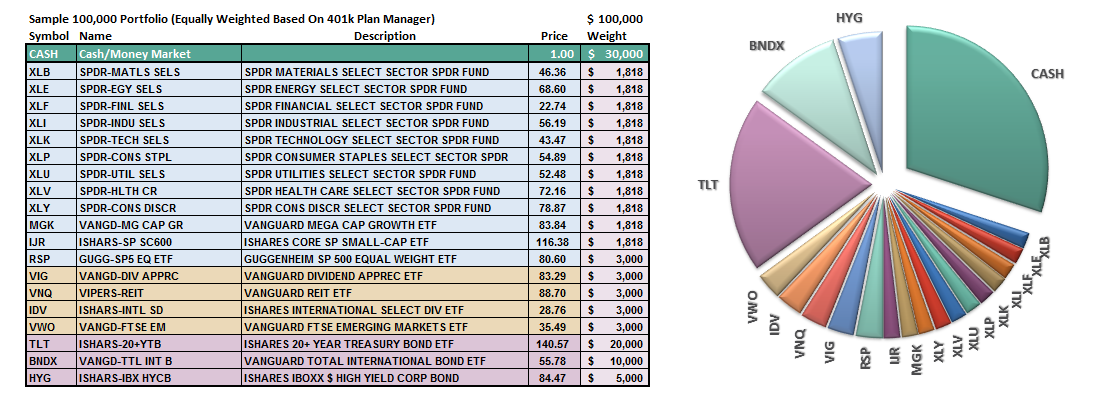

Current 401-k Allocation Model

The 401k plan allocation plan below follows the K.I.S.S. principal. By keeping the allocation extremely simplified it allows for better control of the allocation and a closer tracking to the benchmark objective over time. (If you want to make it more complicated you can, however, statistics show that simply adding more funds does not increase performance to any great degree.)

401k Choice Matching List

The list below shows sample 401k plan funds for each major category. In reality, the majority of funds all track their indices fairly closely. Therefore, if you don’t see your exact fund listed, look for a fund that is similar in nature.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Streettalk Advisors, LLC expressly disclaims all liability in ...

more