Are Strong Earnings Behind Discover?

Photo Credit: 401(K) 2012

Discover Financial Services (DFS) FInancials - Consumer Finance | Reports April 19, After Market Closes

Key Takeaways

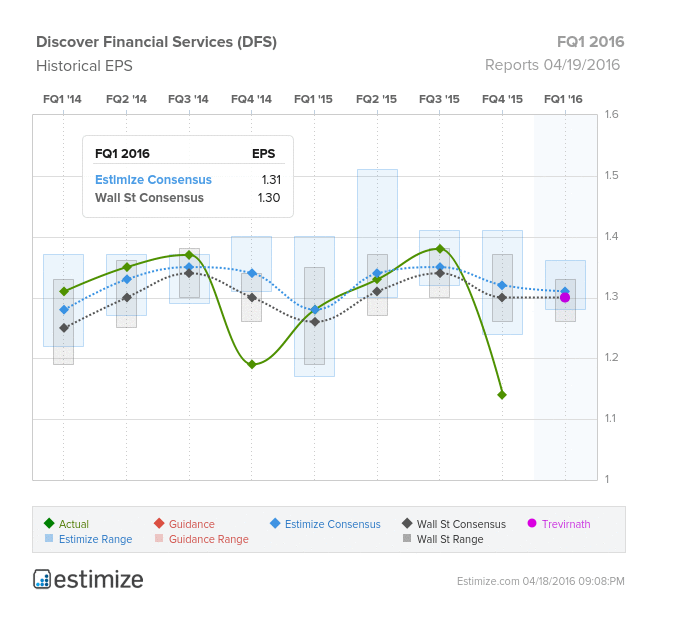

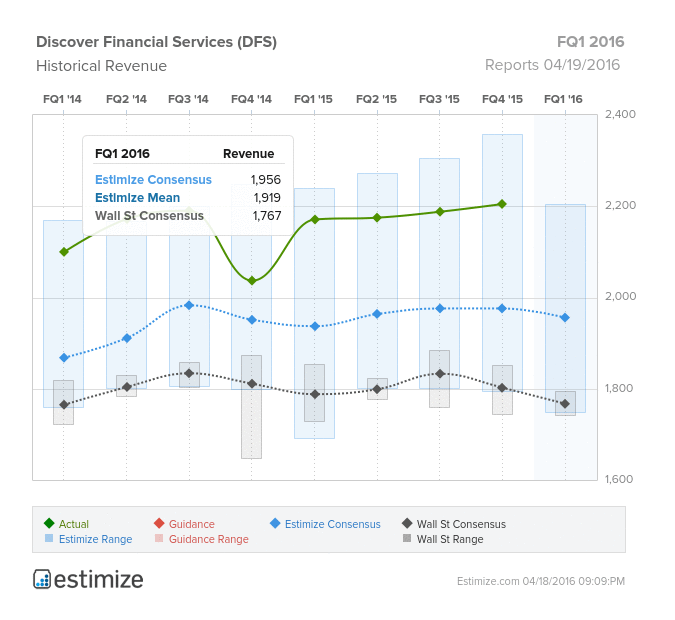

- The Estimize consensus is calling for EPS of $1.31 on $1.92 billion in revenue, 1 cent higher than Wall Street on the bottom line and $150 million on the top

- In the near term, Discover faces threats from stiff competition, litigation expense, regulatory challenge and an overall weakness in its payment services segment

- Last quarter, provisions increased $27 million or 6%, reflecting a high probability of customer defaults

- What are you expecting for DFS? Get your estimate in here!

In the next two weeks we get credit card reports with Discover prepared to kick things off this Tuesday. In the past 2 fiscal years, earnings have been difficult to pin down for the credit card company. Last quarter, Discover missed on the bottom line by 20 cents but crushed revenue expectations by $225 million. The company has taken a beating for this volatility with the stock now down 10% in the past 12 months.

Unfortunately, expectations have been tepid in regards to first quarter earnings. The Estimize consensus is calling for EPS of $1.31 on $1.92 billion in revenue, 1 cent higher than Wall Street on the bottom line and $150 million on the top. However our Select Consensus , a weighted average of our most accurate analysts and recent estimates, is expecting a greater beat of $190 million. Per share estimates have been cut by 2% in the past three month while revenue fell 1%. As a result, earnings are predict to grow by only 2% compared to a year earlier and sales is expected to shrink by 12%.

In the near term, Discover faces threats from stiff competition, litigation expense, regulatory challenge and an overall weakness in its payment services segment. The company’s payment services division has weighed down performance over the past few quarters. In the fourth quarter last year, revenue from the segment decreased to $14 million. Meanwhile, provisions for loan losses increased $27 million or 6% on a larger reserve build versus the prior year. This indicates the company believes there is a high probability customers will default in the near future.

On the bright side, Discover has a slew of initiatives that are expected to pan out in the long run. They include an extensive student loan portfolio, prudent capital management and increased card sales. Additionally, financials appear to be in good shape with total assets and book value rising from the year prior.

Disclosure: There can be no assurance that the information we considered is accurate or complete, nor can there be any assurance that our assumptions are correct.