Appian: An Overhyped But Still Good Enterprise Software IPO

Enterprise software maker Appian (APPN) priced their IPO at $12 yesterday and it traded to $15. It's a solid deal and still has more upside based on our IV model below. However, we take issue with many of their rather bold claims about their technology and where it fits. Our original notes are below along with some added segments of the APPN annotated IPO roadshow transcript to illustrate more of our differences.

Appian is a “low code” application development platform that exploits modern architectures that include the cloud and mobile computing.

Low code or rapid development platforms are a tried-and-true form of enterprise computing that has been around since the early days of client-server computing in the 1990’s. Back then they were called “fourth generation languages” or 4GLs for short. One of the most famous tools of the day was PowerBuilder which was acquired by Sybase in 1994 for $940M. In 2010 Sybase was acquired by SAP for $5.8B.

As architectures change new tools are sought for new projects so they can better leverage the new capabilities. Client-server gave way to “n-tier” computing which has been atomized into the modern cloud computing model. This is where we are today and will be for some time. It includes all the “as a service” technology providers with an emphasis on the use of programmatic interfaces (APIs) to build complex systems.

Rapid and “low-code” platforms offer clients high speed but typically with important trade-offs in terms of fine-grained control and performance. For many applications, the speed of development and ability to make changes rapidly are more important. Unfortunately, there is a lot of hype and overstatement in the Appian IPO roadshow. The company and the software have plenty of value but not to the degree they are touting.

Appian is really a rapid development tool for internal, database oriented applications. As illustrated in some of the examples from the roadshow lots of companies struggle to automate internal workflows and deal with an aging and disconnected set of existing applications. Appian is a great solution for these types of use cases.

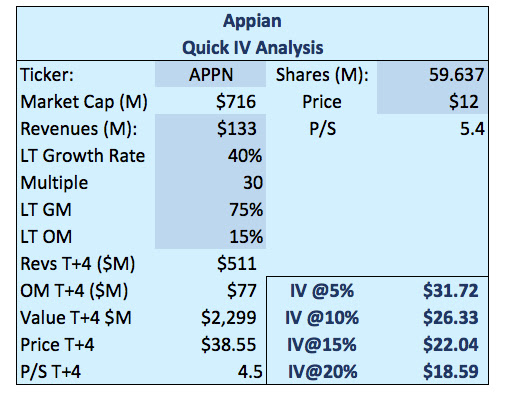

(Click on image to enlarge)

Revenues of $133M are growing at 45% and ultimately they company should be able to deliver typical mature SaaS margins over time. Theirs is a conventional enterprise “land and expand” strategy. We’re putting together a larger list of comparable companies but the ones that jump to mind are Workiva (WK), ServiceNow (NOW) and Varonis (VRNS).

Looking at valuation the IPO price is more than fair and we expect the deal to get done at the high end or above the $11-13 range and trade up from there. Our QuickIV is below and suggests a $22 price target.

Here are some segments of the transcript with our annotations:

Hi, I'm Matt Calkins, CEO of Appian. Appian makes it easy for every company to be a software company. We provide a Platform as a Service on which our clients create, deploy, and use software that automates the unique parts of their operations. Organizations of all kinds are turning to software to differentiate, adapt to unique circumstances, and create distinctive relationships with their customers. It's called digital transformation.

The upside is extraordinary, but the technologies and approaches used today make it a challenging, lengthy, and expensive process. Appian provides a breakthrough product: a platform on which to build sophisticated mission-critical applications with unusual speed. Our product has led to strong customer ROI and fueled Appian's growth. Before I get into detail, let's start with a few investment highlights.

Our platform is addressing a top strategic priority at the C-suite. Our TAM is nearly $30 billion. Our revenue per customer is excellent due to the high value we create and our focus on high-end applications. Our customers are loyal and enthusiastic, with frequent expansions and high lifetime value to Appian.

[Ed. The reality is that Appian is a good solution for internal rather than external applications.]

We are also addressing one of the most pressing problems in IT today — the growing gap between worldwide demand for software, which is rising sharply, and the supply of those who can write it, which is not. We solved the problem by making developers much more productive than they would be otherwise, and by allowing non-developers to build simple software on their own. Just because we make it easy to create software doesn't mean that the software we create is trivial. It's just the opposite.

On our platform, clients build sophisticated, mission-critical applications focused on the core of their value propositions. Our customers include 37 of the Fortune 500, six of the largest financial services firms, and eight of the largest healthcare firms. Twenty organizations, who are nearly 10% of our subscription customer base, pay more than $1 million every year for Appian software. This shows the strategic nature of the problems our customers are addressing with Appian and further validates the strength of our platform.

[Ed. Considering a full-time cost for a single good developer is in the mid-six-figures, using a platform to quickly build internal applications is a no-brainer.]

But most low-code platforms cannot build mission-critical applications. We believe Appian is the first company to combine speed and power in one platform. Appian provides the power of custom development combined with the speed of a low-code platform. We are obsessed with simplicity, and you can see it in everything we do. Making software is naturally difficult. We are determined to keep making it easier. [Ed. Not true. There is a certain “physics” of software the results in a tradeoff between speed and implementing detailed specifications.]

Appian has the greatest advantage when addressing the most powerful applications. On our platform, customers build software with high levels of process sophistication, a wide range of integrations, high concurrency and uptime, and the strongest security requirements. That confluence of speed and power gives Appian a unique market position and an advantage over every vendor we compete against. It also creates a meaningful barrier to entry in the segment of the market that we are leading. [Ed. This paragraph is very overstated – however they are good with BPM applications and enterprise workflow.]

This convergent market is very large by several measures. Simply adding the markets in which Appian competes totals $24 billion. The total size of the custom software market is $148 billion according to Forrester. But the bottom-up analysis is the most revealing. If we extrapolate the software revenue Appian gains from each current client onto the companies with which we do not yet do business, sorted by size and industry, the result is impressive — $29 billion. In 2016, our 280 customers generated $133 million in revenue.

We have a long way to go, continuing to expand with these customers and our high wallet share shows the type of opportunity we have as we expand from hundreds to thousands of clients over time. For a closer look at the Appian product, let me introduce my co-founder and CTO, Mike Beckley.

[Ed. There’s no question that the company has plenty of room to grow from $133M in revenues, however their TAM estimates are far too large because rapid application development is a smallish (but still meaningful) segment of the market.]

Disclosure: We do not have any vested interest in the shares of this stock at the time of writing and publication. We may however take a position post publication and are not under any obligation to ...

more